動物用整形外科インプラントの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Veterinary Orthopedic Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766289

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

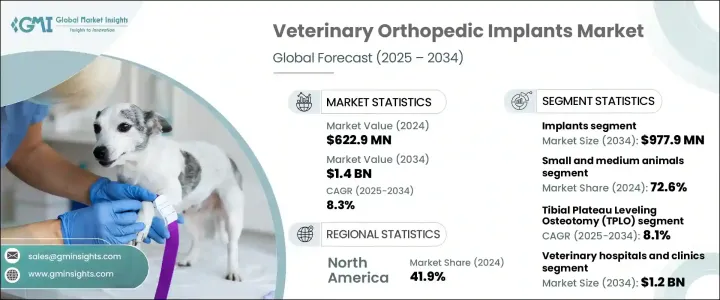

世界の動物用整形外科インプラント市場は、2024年には6億2,290万米ドルと評価され、CAGR 8.3%で成長し、2034年には14億米ドルに達すると推定されています。

この成長は、整形外科処置や骨輪郭形成などの高度な獣医学的サービスへの需要を引き続き促進する、世界のペット所有者数の増加による影響が大きいです。獣医外科手術の技術的進歩、特に関節鏡のような低侵襲技術も回復時間を早めるのに役立っており、ペットの親たちの間で受け入れが進んでいます。

さらに、動物における最新の外科用インプラントの利点に対する認識が高まり、業界参加者に新たな機会が生まれています。新興国における動物ヘルスケアインフラへの投資は、市場の拡大をさらに後押ししています。さらに、現在進行中の研究開発努力は、費用対効果が高く、使いやすいインプラント技術の開発に重点を置いており、先進国市場と新興国市場の両方で採用率が大幅に高まると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 6億2,290万米ドル |

| 予測金額 | 14億米ドル |

| CAGR | 8.3% |

獣医整形外科手術は、コンパニオンアニマルの筋骨格系の疾患を治療するために特に需要が高いです。動物の怪我や変性疾患、特に関節や靭帯に関わる疾患の有病率は増加の一途をたどっており、外科用インプラントの使用が増加しています。また、体内で自然に溶解し、再手術の必要性をなくす生体吸収性インプラント材料の需要も高まっています。ポリ乳酸やポリグリコール酸のようなポリマーを用いて開発されることが多いこれらの材料は、安全性、効率性、コスト面で優れていることから人気を集めています。センサーや薬剤放出コーティングを組み込んだスマートインプラントなどの技術革新も、より顕著になってきています。これらのデバイスは治癒過程をモニターし、術後の感染を減らすのに役立ち、治療成績をさらに向上させる。

製品タイプ別に見ると、市場はインプラントと器具に区分されます。インプラントのカテゴリーはさらに、プレート、関節インプラント、骨ネジとアンカー、ピンとワイヤー、その他の関連部品に分類されます。この分野は2024年に市場をリードし、4億4,200万米ドルの評価額に達し、2034年には9億7,790万米ドルに成長すると予測されています。この優位性は、ペットの整形外科治療に対する意識の高まりと、洗練されたインプラント技術の利用可能性が高まっていることに起因しています。

動物の種類別に見ると、市場は小動物、中動物、大動物に分類されます。犬、猫、その他同程度の大きさの動物を含む小・中動物分野は、2024年の市場シェアの72.6%を占め、2034年までのCAGRは8.5%で拡大すると予測されています。このセグメントの成長を牽引しているのは、世界のペット数の増加と、骨折や関節障害などの整形外科的問題の頻度の増加です。さらに、外科治療へのアクセスが向上し、ペットの飼い主が質の高い治療に投資する意欲が高まっていることも、同分野の成長をさらに後押ししています。

用途別に分析すると、市場には脛骨高原水平化骨切り術(TPLO)、脛骨結節前転術(TTA)、関節置換術、外傷、その他の用途などの手術が含まれます。このうち、TPLO手術は依然として主要な用途であり、2024年には1億4,120万米ドルを占め、2034年にはCAGR 8.1%で3億320万米ドルに成長すると予測されています。この手術は、関節の安定性を回復させ、靭帯損傷に苦しむ動物の回復を早めることで特に知られています。

最終用途別に見ると、市場は動物病院・診療所とその他の動物医療施設に区分されます。2024年には、動物病院と診療所が5億3,710万米ドルの市場価値で優位を占め、2034年にはCAGR 8.5%で12億米ドルに達すると予想されます。設備の整った診療所や病院が堅調に存在し、総合的な獣医療に対する需要が高まっていることが、この分野を牽引しています。診療所や病院は、ほとんどの飼い主が最初に相談する場所でもあり、市場全体の収益に大きく貢献しています。

地域的には、北米が2024年の世界市場をリードし、41.9%のシェアを占めています。ペットの飼育率の高さ、可処分所得の増加、高度な獣医療に対する強い需要が、この地域の成長を後押しする中核的要因となっています。この地域はまた、複数の大手動物用インプラント製造業者の存在、規制の合理化、充実した臨床研究活動などの恩恵を受けており、これらすべてがこの市場の継続的拡大に寄与しています。

市場は適度に統合されており、主要企業は競争力を維持するために買収、提携、製品革新、研究開発投資などの戦略を採用しています。上位5社(DePuy Synthes社(Johnson &Johnson社)、Movora社(Vimian Group社)、Veterinary Instrumentation社、Arthrex Vet Systems社、Rita Leibinger GmbH社)は、合計で世界市場収益の約60%を占めています。これらの企業は、動物用整形外科医療に対する世界のニーズの高まりに対応するため、ポートフォリオの拡充と新市場への参入に引き続き注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 犬の整形外科疾患の発生率増加

- 獣医整形外科技術の進歩

- ペット保険の適用範囲拡大

- 整形外科的問題に関するペット飼い主の意識の高まり

- 業界の潜在的リスク&課題

- 整形外科手術とインプラントの高額な費用

- 熟練した獣医整形外科医の不足

- 市場機会

- インプラントメーカーと動物病院の協力とパートナーシップの強化

- 新興市場における急速な都市化と所得増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- テクノロジーの情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- インプラント

- プレート

- TPLOプレート

- TTAプレート

- 外傷プレート

- 特製プレート

- その他のプレート

- 関節インプラント

- 骨ネジとアンカー

- ピンとワイヤー

- その他のインプラント

- プレート

- 機器

第6章 市場推計・予測:動物の種類別、2021年~2034年

- 主要動向

- 小型・中型動物

- 犬

- 猫

- その他の小型・中型動物

- 大型動物

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 脛骨プラトー水平骨切り術(TPLO)

- 脛骨結節前進術(TTA)

- 関節置換術

- 股関節置換術

- 膝関節置換術

- 肘関節置換術

- 足首置換術

- トラウマ

- その他の用途

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 動物病院・診療所

- その他の最終用途

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AmerisourceBergen Corporation(Cencora, Inc.)

- Arthrex Vet Systems

- B. Braun

- BlueSAO

- DePuy Synthes(Johnson &Johnson)

- Fusion Implants

- GerVetUSA

- GPC Medical Ltd.

- Integra LifeSciences

- Movora(Vimian Group)

- Narang Medical Limited

- Ortho Max

- Orthomed

- Rita Leibinger

- Veterinary Instrumentation

目次

The Global Veterinary Orthopedic Implants Market was valued at USD 622.9 million in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 1.4 billion by 2034. This growth is largely influenced by the rising number of pet owners worldwide, which continues to drive demand for advanced veterinary services such as orthopedic procedures and bone contouring. Technological advancements in veterinary surgery-especially minimally invasive techniques like arthroscopy-are also helping to accelerate recovery time, increasing acceptance among pet parents.

Furthermore, greater awareness about the benefits of modern surgical implants in animals has created new opportunities for industry participants. Investments in animal healthcare infrastructure in emerging economies have further reinforced market expansion. Additionally, ongoing R&D efforts are focused on developing cost-effective and user-friendly implant technologies, which are expected to significantly boost adoption rates across both developed and developing markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $622.9 Million |

| Forecast Value | $1.4 Billion |

| CAGR | 8.3% |

Veterinary orthopedic procedures are in particularly high demand for treating musculoskeletal conditions in companion animals. The prevalence of injuries and degenerative diseases in animals, especially those involving joints and ligaments, continues to rise, prompting increased use of surgical implants. Demand is also climbing for bioabsorbable implant materials that dissolve naturally in the body, eliminating the need for follow-up removal surgeries. These materials, often developed using polymers like polylactic acid and polyglycolic acid, are gaining popularity for their safety, efficiency, and cost advantages. Innovations such as smart implants embedded with sensors or drug-releasing coatings are also becoming more prominent. These devices help monitor healing processes and reduce post-operative infections, further enhancing treatment outcomes.

In terms of product type, the market is segmented into implants and instruments. The implants category is further broken down into plates, joint implants, bone screws and anchors, pins and wires, and other related components. This segment led the market in 2024, reaching a valuation of USD 442 million, and is expected to grow to USD 977.9 million by 2034. This dominance can be attributed to growing awareness around orthopedic care in pets and the increasing availability of sophisticated implant technologies.

By animal type, the market is categorized into small and medium animals and large animals. The small and medium animals segment-which includes dogs, cats, and other similarly sized animals-accounted for 72.6% of the market share in 2024 and is projected to expand at a CAGR of 8.5% through 2034. Growth in this segment is driven by the rising global pet population and the increasing frequency of orthopedic issues, such as fractures and joint disorders. Additionally, enhanced accessibility to surgical treatments and a greater willingness among pet owners to invest in high-quality care are further propelling segment growth.

When analyzed by application, the market includes procedures such as Tibial Plateau Leveling Osteotomy (TPLO), Tibial Tuberosity Advancement (TTA), joint replacement, trauma, and other uses. Among these, TPLO surgery remains a primary application, accounting for USD 141.2 million in 2024, and is projected to grow to USD 303.2 million by 2034, with a CAGR of 8.1%. This procedure is particularly known for restoring joint stability and promoting faster recovery in animals suffering from ligament injuries.

On the basis of end use, the market is segmented into veterinary hospitals and clinics and other veterinary care facilities. In 2024, veterinary hospitals and clinics dominated with a market value of USD 537.1 million, expected to reach USD 1.2 billion by 2034 at a CAGR of 8.5%. The robust presence of well-equipped clinics and hospitals, paired with the growing demand for comprehensive veterinary care, has been instrumental in driving this segment forward. Clinics and hospitals also serve as the initial point of consultation for most pet owners, making them key contributors to overall market revenue.

Geographically, North America led the global market in 2024, holding a share of 41.9%. High levels of pet ownership, rising disposable incomes, and strong demand for advanced veterinary care are core factors fueling regional growth. The region also benefits from the presence of several major veterinary implant manufacturers, streamlined regulatory pathways, and substantial clinical research activities, all of which contribute to the continued expansion of this market.

The market is moderately consolidated, with key players adopting strategies such as acquisitions, partnerships, product innovation, and R&D investments to maintain their competitive edge. The top five companies- DePuy Synthes (Johnson & Johnson), Movora (Vimian Group), Veterinary Instrumentation, Arthrex Vet Systems, and Rita Leibinger GmbH-collectively accounted for approximately 60% of global market revenue. These firms continue to focus on expanding their portfolios and entering new markets to address the growing global need for veterinary orthopedic care.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Animal type

- 2.2.4 Application

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing incidence of orthopedic conditions in dogs

- 3.2.1.2 Advancement in veterinary orthopedic technology

- 3.2.1.3 Expansion of pet insurance coverage

- 3.2.1.4 Increasing awareness among pet owners about orthopedic problems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of orthopedic procedures and implants

- 3.2.2.2 Limited availability of skilled veterinary orthopedic surgeons

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing collaboration and partnership between implant manufacturers and veterinary hospitals

- 3.2.3.2 Rapid urbanization and income growth in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Implants

- 5.2.1 Plates

- 5.2.1.1 TPLO plates

- 5.2.1.2 TTA plates

- 5.2.1.3 Trauma plates

- 5.2.1.4 Specialty plates

- 5.2.1.5 Other plates

- 5.2.2 Joint implants

- 5.2.3 Bone screws and anchors

- 5.2.4 Pins and Wires

- 5.2.5 Other implants

- 5.2.1 Plates

- 5.3 Instruments

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Small and medium animals

- 6.2.1 Dogs

- 6.2.2 Cats

- 6.2.3 Other small and medium animals

- 6.3 Large animals

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Tibial Plateau Leveling Osteotomy (TPLO)

- 7.3 Tibial Tuberosity Advancement (TTA)

- 7.4 Joint replacement

- 7.4.1 Hip replacement

- 7.4.2 Knee replacement

- 7.4.3 Elbow replacement

- 7.4.4 Ankle replacement

- 7.5 Trauma

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospitals and clinics

- 8.3 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AmerisourceBergen Corporation (Cencora, Inc.)

- 10.2 Arthrex Vet Systems

- 10.3 B. Braun

- 10.4 BlueSAO

- 10.5 DePuy Synthes (Johnson & Johnson)

- 10.6 Fusion Implants

- 10.7 GerVetUSA

- 10.8 GPC Medical Ltd.

- 10.9 Integra LifeSciences

- 10.10 Movora (Vimian Group)

- 10.11 Narang Medical Limited

- 10.12 Ortho Max

- 10.13 Orthomed

- 10.14 Rita Leibinger

- 10.15 Veterinary Instrumentation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日