血栓溶解薬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Thrombolytic Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766280

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

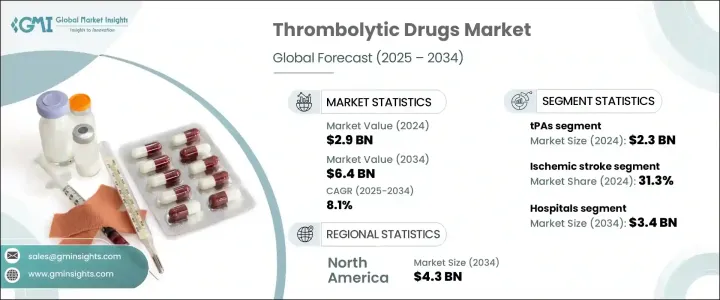

世界の血栓溶解薬市場は、2024年には29億米ドルと評価され、CAGR 8.1%で成長し、2034年には64億米ドルに達すると推定されています。

この着実な増加は、心臓発作、脳卒中、肺塞栓症、その他の血栓関連疾患など、世界中で心血管疾患の負担が増大していることを反映しています。座りがちなライフスタイル、肥満、高血圧、高齢化がますます一般的になるにつれて、血栓塞栓イベントの有病率は加速しています。このような動向は、緊急時に効果的に投与できる即効性の血栓溶解薬に対する大きな需要を促しています。医療システムは、特に患者の転帰を改善するために迅速な介入が重要である急性期医療現場において、このような治療の緊急性を認識しています。

市場を前進させる上で、技術は重要な役割を果たしています。薬剤開発とドラッグデリバリー法の進歩は、血栓溶解療法の精度と効率の向上に役立っています。投与法や製剤の革新も、より広範な臨床採用を後押ししています。こうした開発と並行して、診断技術や画像診断技術の向上により、早期介入に対する意識が高まっています。これらの薬剤が最もよく使用される病院や救急外来では、タイムリーな発見と迅速な治療が標準となりつつあります。臨床が進化するにつれて、効果的なだけでなく安全で投与が容易な治療薬も必要とされています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 29億米ドル |

| 予測金額 | 64億米ドル |

| CAGR | 8.1% |

血栓溶解薬は、しばしば線溶薬と呼ばれ、様々な心血管系疾患により形成される血栓を溶解するのに不可欠です。これらの薬剤は、体内の線溶系を活性化し、血栓に含まれる主要なタンパク質であるフィブリンを分解することで機能します。同市場は、組織プラスミノーゲン活性化薬(tPAs)、ストレプトキナーゼ、ウロキナーゼ型プラスミノーゲン活性化薬(uPAs)など、いくつかの主要カテゴリーで構成されており、その用途は主に病院や重症患者への治療に集中しています。

このうち、tPAs分野は世界市場をリードし、2024年には23億米ドルの売上を計上しました。このセグメントは、CAGR 8.2%で成長し、2034年には51億米ドルに達すると予想されています。tPAの優位性は、重大な健康イベント時の血栓溶解におけるその高い有効性に起因します。これらの薬剤は、急性症例に速やかに使用された場合の臨床的有用性が十分に立証されているため、広く処方されています。tPAの使用量増加の根本的な要因のひとつは、世界の糖尿病患者の急増です。糖尿病は、血管障害、血液凝固傾向の亢進、代謝の不均衡などを通じて血栓性イベントのリスクを高め、これらすべてが積極的な血栓溶解療法の必要性を高めています。

血栓溶解薬で治療される疾患としては、虚血性脳卒中が最大の適応症であり、2024年の世界市場シェアの31.3%を占めています。このセグメントは、世界的に脳卒中患者の大半を占める虚血性脳卒中の高い発生率に支えられ、2034年まで力強い成長を維持する見通しです。これらの脳卒中は通常、脳血流の障害によって引き起こされ、早急な治療が必要です。脳卒中症例の世界の増加に加え、脳卒中の予防と管理に対する意識の高まりが、血栓溶解療法の需要を高めています。糖尿病、高血圧、肥満といった一般的に脳卒中リスクと関連する疾患は、これらの薬剤を用いた効果的な医療介入の必要性をさらに高めています。

エンドユーザー別では、病院が2024年に市場の54.8%を占める主要セグメントとなりました。このセグメントはCAGR 7.7%で推移し、2034年には34億米ドルに達する見込みです。病院は、迅速な診断と遅滞のない治療開始が可能なため、血栓溶解療法を必要とする患者の一次治療を行う場所として機能しています。心臓発作や脳卒中による緊急入院の頻度が増加していることが、引き続き病院の需要を支えています。さらに、クリティカルケアインフラへの世界の投資により、特に都市部や先進ヘルスケアシステムにおいて、こうした治療へのアクセスが拡大しています。外来患者センターが普及しつつある一方で、病院環境は依然として血栓溶解薬投与の要です。

地域別では、北米が2024年の市場をリードし、20億米ドルの収益を上げました。同地域はCAGR 7.9%で成長し、2034年には43億米ドルに達すると予測されています。北米が市場をリードしているのは、先進的なヘルスケアインフラ、良好な償還環境、血栓性疾患の有病率の高さなどに起因しています。同地域では、先進的な治療法の採用が増加し、ヘルスケア政策も充実しているため、血栓溶解薬の需要が引き続き高まっています。加えて、医薬品の技術革新、強固な臨床パイプライン、強力な業界プレゼンスが、この地域の世界の優位性に寄与しています。

競合環境は、主要企業が研究投資を行い、製品ラインを拡大し、新興市場をターゲットにしてアクセスを拡大することで定義されます。企業は、規制が厳しく実績重視の市場において優位性を維持するため、ドラッグの安全性プロファイルの改善やデリバリー方法の合理化に努めています。このような努力は、技術革新、臨床需要、戦略的ポジショニングによって形成される血栓溶解薬開発の継続的な進化を強調するものです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 心血管および脳血管イベントの発生率の上昇

- 一次脳卒中センターおよび救急医療インフラの拡張

- 血栓溶解薬製剤の進歩

- 好ましいガイドラインとプロトコルの組み込み

- 業界の潜在的リスク&課題

- 出血リスクが高く、治療域が狭い

- 機械的介入および直接経口抗凝固薬(DOAC)との競合

- 市場機会

- 政府の取り組みと資金

- 希少血液凝固障害に合わせた血栓溶解薬の開発

- 促進要因

- 成長可能性分析

- パイプライン分析

- 将来の市場動向

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 臨床試験分析

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 拡張計画

第5章 市場推計・予測:薬剤クラス別、2021年~2034年

- 主要動向

- 組織プラスミノーゲン活性化因子(tPA)

- ストレプトキナーゼ誘導体

- ウロキナーゼ型プラスミノーゲン活性化因子(uPA)

第6章 市場推計・予測:適応症別、2021年~2034年

- 主要動向

- 虚血性脳卒中

- 心筋梗塞

- 肺塞栓症

- 深部静脈血栓症

- カテーテル閉塞

- その他の適応症

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- その他最終の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- Boehringer Ingelheim

- Chiesi Farmaceutici

- Genentech(F. Hoffmann-La Roche)

- Gennova Biopharmaceuticals

- Karma Pharmatech

- Lupin

- MicrobixBiosystems

- Reliance Lifesciences

- TechpoolBio-Pharma(Shanghai Pharma)

目次

The Global Thrombolytic Drugs Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 6.4 billion by 2034. This steady rise reflects the growing burden of cardiovascular diseases across the globe, including heart attacks, strokes, pulmonary embolism, and other clot-related conditions. As sedentary lifestyles, obesity, hypertension, and aging populations become increasingly common, the prevalence of thromboembolic events is accelerating. These trends are driving significant demand for fast-acting clot-dissolving medications that can be administered effectively in emergencies. Health systems are recognizing the urgency of such treatments, especially in acute care settings, where rapid intervention is critical for improving patient outcomes.

Technology is playing a vital role in propelling the market forward. Advancements in drug development and delivery methods are helping enhance the precision and efficiency of thrombolytic therapies. Innovations in dosing and formulation are also supporting broader clinical adoption. Alongside these developments, awareness surrounding early intervention is growing, thanks to improved diagnostic and imaging technologies. Timely detection and prompt treatment are becoming the standard in hospitals and emergency rooms, where these drugs are most commonly used. As clinical practice evolves, so does the need for therapeutics that are not only effective but also safe and easy to administer.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 8.1% |

Thrombolytic drugs, often referred to as fibrinolytic agents, are essential in dissolving blood clots that form due to various cardiovascular conditions. These medications work by activating the body's fibrinolytic system to break down fibrin, the primary protein found in clots. The market comprises several key categories, including tissue plasminogen activators (tPAs), streptokinase, and urokinase-type plasminogen activators (uPAs), with applications mostly concentrated in hospitals and critical care settings.

Among these, the tPAs segment led the global market, generating USD 2.3 billion in revenue in 2024. This segment is expected to rise to USD 5.1 billion by 2034, growing at a CAGR of 8.2%. The dominance of tPAs stems from their high efficacy in clot resolution during critical health events. These agents are widely prescribed due to well-documented clinical benefits when used promptly in acute cases. One of the underlying drivers of increased tPA utilization is the global surge in diabetes cases. The disease heightens the risk of thrombotic events through vascular damage, increased clotting tendencies, and metabolic imbalances, all of which raise the need for aggressive clot-busting therapies.

In terms of medical conditions treated with thrombolytics, ischemic stroke represented the largest indication segment, accounting for 31.3% of the global market share in 2024. This segment is on track to maintain strong growth through 2034, supported by the high incidence of ischemic strokes, which make up the majority of stroke cases globally. These strokes are typically caused by obstructions in cerebral blood flow and require immediate medical attention. The growing number of stroke cases worldwide, combined with rising awareness of stroke prevention and management, is increasing the demand for thrombolytic therapies. Conditions such as diabetes, high blood pressure, and obesity-commonly linked to stroke risk-are further boosting the need for effective medical intervention using these drugs.

By end user, hospitals emerged as the leading segment in 2024, holding a 54.8% share of the market. This segment is expected to reach USD 3.4 billion by 2034, progressing at a CAGR of 7.7%. Hospitals serve as the primary point of care for patients requiring thrombolytic treatment, thanks to their ability to conduct rapid diagnostics and initiate therapy without delay. The increasing frequency of emergency admissions due to heart attacks and strokes continues to support hospital demand. Additionally, global investment in critical care infrastructure is expanding access to such treatments, especially in urban areas and developed healthcare systems. While outpatient centers are gaining traction, hospital settings remain the cornerstone of thrombolytic drug administration.

Regionally, North America led the market in 2024, generating USD 2 billion in revenue. The region is forecasted to reach USD 4.3 billion by 2034, growing at a CAGR of 7.9%. The market leadership of North America can be attributed to its advanced healthcare infrastructure, favorable reimbursement environment, and high prevalence of thrombotic disorders. The increased adoption of advanced therapies and supportive healthcare policies in this region continue to drive the demand for thrombolytics. Additionally, pharmaceutical innovation, a robust clinical pipeline, and strong industry presence contribute to the region's dominance in the global landscape.

The competitive environment is defined by leading players investing in research, expanding product lines, and targeting emerging markets to broaden access. Companies are striving to improve drug safety profiles and streamline delivery methods to maintain their edge in a tightly regulated, performance-focused market. These efforts underscore the ongoing evolution of thrombolytic drug development, shaped by innovation, clinical demand, and strategic positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drug class

- 2.2.3 Indication

- 2.2.4 End use

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of cardiovascular and cerebrovascular events

- 3.2.1.2 Expansion of primary stroke centers and emergency care infrastructure

- 3.2.1.3 Advancements in thrombolytic drug formulations

- 3.2.1.4 Favorable guidelines and protocol inclusion

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk of bleeding and narrow therapeutic window

- 3.2.2.2 Competition from mechanical interventions and direct oral anticoagulants (DOACs)

- 3.2.3 Market opportunities

- 3.2.3.1 Government initiatives and funding

- 3.2.3.2 Development of thrombolytics tailored to rare clotting disorders

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.7 Clinical trial analysis

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers and acquisitions

- 4.5.2 Partnerships and collaborations

- 4.5.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Tissue plasminogen activators (tPAs)

- 5.3 Streptokinase derivatives

- 5.4 Urokinase-type plasminogen activators (uPAs)

Chapter 6 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Ischemic stroke

- 6.3 Myocardial infarction

- 6.4 Pulmonary embolism

- 6.5 Deep vein thrombosis

- 6.6 Catheter occlusion

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Boehringer Ingelheim

- 9.3 Chiesi Farmaceutici

- 9.4 Genentech (F. Hoffmann-La Roche)

- 9.5 Gennova Biopharmaceuticals

- 9.6 Karma Pharmatech

- 9.7 Lupin

- 9.8 MicrobixBiosystems

- 9.9 Reliance Lifesciences

- 9.10 TechpoolBio-Pharma (Shanghai Pharma)

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日