会計向け人工知能の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Artificial Intelligence for Accounting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766244

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

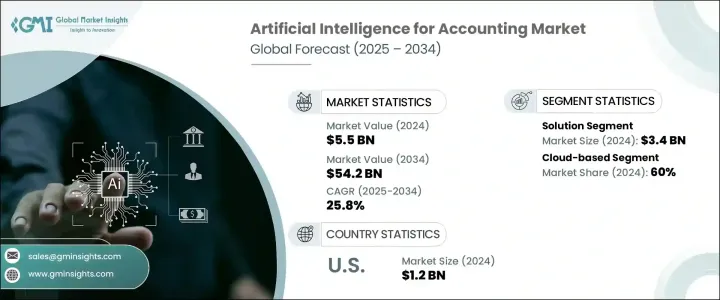

会計向け人工知能の世界市場規模は、2024年には55億米ドルとなり、CAGR 25.8%で成長し、2034年には542億米ドルに達すると予測されています。

この大幅な成長は、さまざまな部門における会計業務の自動化に対する需要の高まりによって後押しされています。企業が大量の財務情報を扱うようになるにつれ、従来の経理管理方法は非効率でミスを犯しやすいことがわかってきています。このような環境において、人工知能は変革の力として台頭しており、業務の合理化、リアルタイムの財務洞察、コンプライアンスの改善を全面的に提供しています。

取引処理や監査証跡から予測的な財務計画やリスク検知まで、すべてを処理できるAI搭載ツールに注目する企業が増えており、時間のかかる手作業をスマートな自動化システムに置き換えています。スピード、正確性、データ主導の意思決定へのニーズはかつてないほど高まっており、企業はAI主導の機能を会計ワークフローに統合する必要に迫られています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 55億米ドル |

| 予測金額 | 542億米ドル |

| CAGR | 25.8% |

AIは、請求書発行、照合、予測などのデータ集約的な作業を自動化することで、手作業によるミスを最小限に抑え、時間を節約することで、現代企業の財務機能に革命をもたらしています。さらに、動向を分析し、異常のフラグを立て、ダイナミックなレポートを作成できるインテリジェントシステムにより、財務チームは取引プロセスからより戦略的な役割へと重点を移すことができるようになっています。企業がコスト削減とリアルタイムのレポーティングをますます優先するようになる中、AIテクノロジーは拡張性があり、直感的で効率的なソリューションを提供するために参入しています。

また、クラウドベースのプラットフォームとAIの統合が進み、シームレスな更新、データへのアクセスの向上、企業業務全体への展開が容易になっていることも一因となっています。これらのプラットフォームにより、会計チームはどこからでもコラボレーションが可能になり、財務業務における継続的な接続性と俊敏性が確保されます。クラウドインフラストラクチャーは、ITに多大な負担をかけることなくAIソリューションを展開するのに必要な柔軟性を提供するため、各業界で採用が加速しています。

市場は構成要素に基づき、ソリューションとサービスに区分されます。2024年の市場規模は、ソリューションセグメンテーションが約34億米ドルを稼ぎ出し、市場を独占しました。AI主導のソリューションが好まれるのは、経費追跡、給与計算の自動化、規制当局への報告などの会計プロセスを強化する能力に起因します。これらのシステムは、リアルタイムの分析を提供し、ヒューマンエラーの余地を減らし、迅速なターンアラウンドタイムを促進することにより、透明性と意思決定を向上させます。企業が業務をデジタル化するにつれて、包括的なAIソリューションに対する需要はあらゆる規模の企業で着実に高まっています。

クラウドベースとオンプレミスの2つに市場は分かれています。2024年にはクラウドベースのセグメントが市場をリードし、世界売上の約60%を占める。クラウドソリューションは、拡張性、コスト削減、他の企業アプリケーションとの統合の容易さなど、大きな利点を提供します。ハイブリッドワークモデルをサポートし、遠隔地での財務管理を可能にするクラウドソリューションは、柔軟で将来性のあるソリューションを求める企業にとって最適な選択肢となっています。

組織規模別では、大企業が2024年の市場を独占しています。これらの企業は通常、複雑な金融エコシステムを管理しており、多様なワークフローと大量の取引に対応できる拡張性の高いAIツールを必要としています。先進技術への投資が可能なこれらの企業は、効率的な財務計画、コンプライアンス、不正検出のために、自然言語処理、機械学習アルゴリズム、予測分析などのAI機能を実装することができます。

用途別では、財務報告が2024年の市場で最大のシェアを占めています。組織がより高い精度と規制との整合性を目指す中、AIツールはリアルタイムの報告書、予測、分析を作成する上で不可欠であることが証明されています。これらのアプリケーションは、手作業への依存を大幅に減らし、動的な財務データの視覚化を可能にすることで、報告サイクルを加速し、精度を向上させる。

最終用途産業別に評価すると、2024年の市場シェアは金融サービスが最大となりました。高度に規制された環境とデータの正確性に対する絶え間ないニーズにより、同業界はAI主導の会計ツールから多大な恩恵を受けています。これらのツールは、大規模なデータセットの管理、監査の合理化、不正行為の監視、一貫した規制遵守の確保を支援します。金融規制の複雑化は、エラーのない透明性の高い財務報告のためにAIを導入する金融機関をさらに後押ししています。

地域別では、米国が北米の会計向け人工知能市場をリードし、2024年には12億米ドルの収益を上げ、2034年までのCAGRは26.7%で成長すると予測されています。同国の先進的なデジタル・インフラと、業務全般にわたるAIの迅速な導入が、このリーダーシップの中心的役割を果たしました。会計事務所がサービスを近代化するにつれて、AIを搭載したツールはクライアントサービスの標準コンポーネントとなりつつあり、カスタマイズされたインサイトを提供し、ターンアラウンド・タイムを改善するのに役立っています。

現在の市場戦略は、幅広い会計ニーズに対応する柔軟で統合的なAIモジュールの提供が中心となっています。自動データ収集、異常検知、インテリジェント予測などの機能を備えたこれらのモジュール式システムにより、企業は大規模なオーバーホールを行うことなく、既存の会計インフラを迅速にアップグレードすることができます。

ベンダーは、中小企業から大企業まで、それぞれのニーズに合った拡張性のある使いやすいソリューションに注力しています。さらに、AIはもはや単なるサポートツールとは見なされず、戦略的なイネーブラーとして認識されつつあります。企業は、財務チームが長期的な計画を推進し、組織の階層を超えてパフォーマンスを最適化できるよう支援する、コンテキスト分析と実用的な洞察を提供するAIプラットフォームに投資しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料供給者

- 部品供給業者

- 製造業者

- テクノロジープロバイダー

- 流通チャネル分析

- 最終用途

- 利益率分析

- サプライヤーの情勢

- テクノロジーとイノベーションの情勢

- 特許分析

- 規制情勢

- コスト内訳分析

- 主なニュースと取り組み

- 影響要因

- 促進要因

- リアルタイムの金融情報に対する需要の高まり

- 不正検出とリスク管理への注目の高まり

- 日常的な会計業務の自動化

- クラウドベースの会計プラットフォームとの統合

- 自然言語処理(NLP)と機械学習の進歩

- 業界の潜在的リスク&課題

- 高い導入コスト

- データのプライバシーとセキュリティに関する懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- コアGL自動化

- 予測分析と予測

- 文書と請求書のインテリジェンス

- 不正検出と異常スコアリング

- サービス

- マネージドサービス

- 実装と統合

- トレーニングとサポート

第6章 市場推計・予測:展開別、2021年~2034年

- 主要動向

- クラウドベース

- オンプレミス

第7章 市場推計・予測:組織規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 財務報告

- 監査

- 不正行為検出

- 税務管理

- 給与管理

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 金融サービス

- ヘルスケア

- 教育

- 政府

- 製造業

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- AppZen

- BlackLine

- Botkeeper

- Docyt

- EY

- FloQast

- IBM

- Intuit

- KPMG

- Microsoft

- Oracle

- Pilot

- PwC

- Sage

- SAP SE

- Thomson Reuters

- Vic.ai

- Workday

- Xero

目次

The Global Artificial Intelligence for Accounting Market was valued at USD 5.5 billion in 2024 and is estimated to grow at a CAGR of 25.8% to reach USD 54.2 billion by 2034. This substantial growth is being fueled by the rising demand for automation in accounting tasks across various sectors. As companies deal with growing volumes of financial information, traditional methods of managing accounts are proving inefficient and prone to error. In this environment, artificial intelligence is emerging as a transformative force, offering streamlined operations, real-time financial insights, and improved compliance across the board.

Businesses are increasingly turning to AI-powered tools that can handle everything from transaction processing and audit trails to predictive financial planning and risk detection, replacing time-consuming manual tasks with smart, automated systems. The need for speed, accuracy, and data-driven decision-making has become more critical than ever, pushing enterprises to integrate AI-driven capabilities into their accounting workflows.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.5 Billion |

| Forecast Value | $54.2 Billion |

| CAGR | 25.8% |

AI is revolutionizing the financial functions of modern enterprises by automating data-intensive tasks like invoicing, reconciliation, and forecasting, thereby minimizing manual errors and saving time. Additionally, intelligent systems that can analyze trends, flag anomalies, and generate dynamic reports are enabling finance teams to shift focus from transactional processes to more strategic roles. As companies increasingly prioritize cost reduction and real-time reporting, AI technologies are stepping in to deliver scalable, intuitive, and efficient solutions.

Another contributing factor is the rising integration of AI with cloud-based platforms, which allows for seamless updates, better data accessibility, and easier deployment across enterprise operations. These platforms make it possible for accounting teams to collaborate from anywhere, ensuring continuous connectivity and agility in financial operations. With cloud infrastructure offering the flexibility needed to deploy AI solutions without the burden of heavy IT overheads, adoption across industries continues to accelerate.

Based on component, the market is segmented into solutions and services. The solutions segment dominated the market in 2024, generating approximately USD 3.4 billion in revenue. The preference for AI-driven solutions stems from their ability to enhance accounting processes such as expense tracking, payroll automation, and regulatory reporting. These systems improve transparency and decision-making by offering real-time analytics, reducing the margin for human error, and facilitating faster turnaround times. As businesses digitize their operations, demand for comprehensive AI solutions is rising steadily among enterprises of all sizes.

Deployment-wise, the market is split between cloud-based and on-premises systems. The cloud-based segment led the market in 2024, accounting for around 60% of the global revenue. Cloud solutions offer significant advantages including scalability, cost savings, and ease of integration with other enterprise applications. Their ability to support hybrid work models and enable remote financial management has made them the go-to choice for businesses looking for flexible and future-ready solutions.

By organization size, large enterprises dominated the market in 2024. These companies typically manage complex financial ecosystems and require scalable AI tools that can handle diverse workflows and high transaction volumes. Their ability to invest in advanced technologies allows them to implement AI features such as natural language processing, machine learning algorithms, and predictive analytics for efficient financial planning, compliance, and fraud detection.

In terms of application, financial reporting held the largest share of the market in 2024. As organizations strive for greater accuracy and regulatory alignment, AI tools have proven vital in producing real-time reports, forecasts, and analyses. These applications significantly reduce reliance on manual intervention and enable dynamic financial data visualization, thereby accelerating the reporting cycle and improving accuracy.

When evaluated by end-use industry, financial services accounted for the largest market share in 2024. With highly regulated environments and a constant need for data accuracy, the sector benefits immensely from AI-driven accounting tools. These tools help manage large datasets, streamline audits, monitor for fraudulent activities, and ensure consistent regulatory compliance. The growing complexity of financial regulations is further pushing institutions to adopt AI for error-free and transparent financial reporting.

Regionally, the United States led the North America artificial intelligence for accounting market, generating USD 1.2 billion in revenue in 2024 and projected to grow at a CAGR of 26.7% through 2034. The country's advanced digital infrastructure and quick uptake of AI across business operations have played a central role in this leadership. As accounting firms modernize their offerings, AI-powered tools are becoming standard components in client servicing, helping deliver customized insights and improve turnaround time.

Current market strategies are centered around offering flexible and integrative AI modules that cater to a wide spectrum of accounting needs. These modular systems-featuring capabilities like automated data capture, anomaly detection, and intelligent forecasting-allow companies to quickly upgrade their existing accounting infrastructure without major overhauls.

Vendors are focusing on scalable and user-friendly solutions that suit the unique needs of small, medium, and large enterprises. Furthermore, AI is no longer viewed as just a support tool; it is increasingly recognized as a strategic enabler. Companies are investing in AI platforms that offer contextual analysis and actionable insights, helping finance teams drive long-term planning and optimize performance across organizational layers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Growing demand for real-time financial insights

- 3.7.1.2 Rising focus on fraud detection and risk management

- 3.7.1.3 Automation of routine accounting tasks

- 3.7.1.4 Integration with cloud-based accounting platforms

- 3.7.1.5 Advancements in natural language processing (NLP) and machine learning

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High implementation costs

- 3.7.2.2 Data privacy and security concerns

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Solutions

- 5.2.1 Core GL automation

- 5.2.2 Predictive analytics & forecasting

- 5.2.3 Document & invoice intelligence

- 5.2.4 Fraud detection & anomaly scoring

- 5.3 Services

- 5.3.1 Managed services

- 5.3.2 Implementation & integration

- 5.3.3 Training & support

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premises

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Small and medium-sized enterprises

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Financial reporting

- 8.3 Auditing

- 8.4 Fraud detection

- 8.5 Tax management

- 8.6 Payroll management

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Financial services

- 9.3 Healthcare

- 9.4 Education

- 9.5 Government

- 9.6 Manufacturing

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 AppZen

- 11.2 BlackLine

- 11.3 Botkeeper

- 11.4 Docyt

- 11.5 EY

- 11.6 FloQast

- 11.7 Google

- 11.8 IBM

- 11.9 Intuit

- 11.10 KPMG

- 11.11 Microsoft

- 11.12 Oracle

- 11.13 Pilot

- 11.14 PwC

- 11.15 Sage

- 11.16 SAP SE

- 11.17 Thomson Reuters

- 11.18 Vic.ai

- 11.19 Workday

- 11.20 Xero

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日