|

市場調査レポート

商品コード

1766241

ドセタキセルの市場機会、成長促進要因、産業動向分析、2025~2034年予測Docetaxel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ドセタキセルの市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年06月03日

発行: Global Market Insights Inc.

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

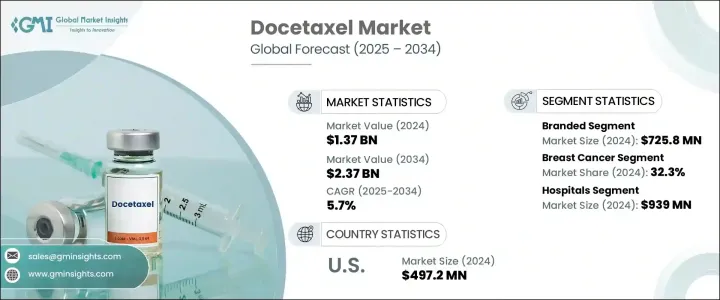

ドセタキセルの世界市場規模は、2024年に13億7,000万米ドルとなり、CAGR 5.7%で成長し、2034年には23億7,000万米ドルに達すると予測されています。

この成長は、ドセタキセルが広く使用されている乳がん、肺がん、前立腺がん、胃がんなど、さまざまながんの罹患率の増加が主な要因です。第二世代のタキサン系抗がん剤であるドセタキセルは微小管を安定化させ、がん細胞の分裂を停止させるため、化学療法レジメンの重要な一部となっています。併用療法において特に有効であり、トリプルネガティブ乳がんや去勢抵抗性前立腺がんなどの進行がん患者の生存率向上に役立っています。さらに、ナノ粒子製剤やリポソームカプセル化などのドラッグデリバリー法の革新により、バイオアベイラビリティが向上し、毒性も軽減されたため、臨床応用が拡大しています。

バイオシミラーやジェネリック医薬品の承認が進むにつれて、特に中低所得地域では薬剤がより入手しやすくなっており、一方、がん研究開発への注目の高まりがこの必須細胞毒性薬剤の需要を押し上げています。デジタルヘルス技術も、治療反応や副作用の遠隔モニタリングを通じて、より良い治療の個別化を可能にする役割を担っています。さらに、がんに対する意識の高まり、都市化、早期診断への取り組みが、化学療法やドセタキセルのような薬剤への依存度を高める一因となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 13億7,000万米ドル |

| 予測金額 | 23億7,000万米ドル |

| CAGR | 5.7% |

ドセタキセル市場のブランド品セグメントは、2024年に7億2,580万米ドルを創出し、確立された臨床的評判とオリジナル製剤の有効性から利益を得ています。ジェネリック医薬品の存在にもかかわらず、ブランド製品はその信頼できる安全性プロファイル、規制当局の承認、高品質な規格により、新興国市場では引き続き優位を占めています。乳がん、非小細胞肺がん(NSCLC)、前立腺がんなどの複雑ながんを治療する場合、特に病院での治療では、腫瘍専門医にブランド品のドセタキセルが好まれることが多いです。さらに、新しい投与方法や併用療法への投資が、このブランドの価値をさらに高めています。

2024年には、乳がん分野はHER2陰性およびトリプルネガティブ乳がん患者の早期および進行治療レジメンによって32.3%を占めました。TAC(ドセタキセル、ドキソルビシン、シクロホスファミド)のような併用治療で一般的に使用され、生存予後を改善することが示されています。個別化腫瘍学システムの進歩により、乳がん症例管理におけるドセタキセルの需要は増加の一途をたどっています。

米国のドセタキセル市場は2024年に4億9,720万米ドルと評価されました。有利な償還政策、精密腫瘍学サービスの拡大、個別化医療への注力といった要因が需要を後押ししています。さらに、外来化学療法へのアクセスの拡大、がんに対する意識の高まり、継続的な臨床研究が米国市場の成長を後押ししています。医薬品開発と市場開拓を加速させる製薬企業と研究センターの戦略的提携により、主要市場としての米国の役割はさらに強化されています。

世界のドセタキセル業界の主要企業には、Alchem International、Alkem Labs、Arch Pharmalabs、Aspen Pharmacare、Cipla、Cisen Pharmaceutical、LGM Pharma、Phyton Biotech、Qilu Pharmaceutical、Teva Active Pharmaceutical Ingredients(TAPI)、Teva Pharmaceuticals、Venus Remedies、Xiromedなどがあります。ドセタキセル市場で事業を展開する企業は、新しい製剤、送達方法、併用療法を提供することで、製品ポートフォリオの拡大に注力しています。研究機関や病院との提携は、ドセタキセルの臨床応用と採用を強化するために不可欠です。多くの企業がバイオシミラーやジェネリック医薬品に投資し、コストに敏感な市場に参入することで、この重要な医薬品への幅広いアクセスを確保しています。さらに、個別化医療や高度なデジタルヘルス技術の開発により、企業は患者のニーズによりよく対応し、治療成績を向上させることができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 世界のがん罹患率の上昇

- 併用療法の採用増加

- 好ましい規制承認とガイドライン

- 医薬品製剤における技術の進歩

- 業界の潜在的リスク&課題

- 重篤な副作用と毒性の懸念

- 特許の満了とジェネリック医薬品の競合

- 市場機会

- 個別化腫瘍治療アプローチの拡大

- 腫瘍学の研究開発への投資の増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- 償還シナリオ

- 償還政策が市場成長に与える影響

- 消費者行動分析

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- ブランド

- ジェネリック医薬品

第6章 市場推計・予測:適応症別、2021年~2034年

- 主要動向

- 乳がん

- 非小細胞肺がん(NSCLC)

- ホルモン抵抗性前立腺がん

- 胃腺がん

- 頭頸部扁平上皮がん(HNSCC)

- その他の適応症

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 腫瘍学クリニック

- その他の最終用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Alchem International

- Alkem Labs

- Arch Pharmalabs

- Aspen Pharmacare

- Cipla

- Cisen Pharmaceutical

- LGM Pharma

- Phyton Biotech

- Qilu Pharmaceutical

- Teva Active Pharmaceutical Ingredients(TAPI)

- Teva Pharmaceuticals

- Venus Remedies

- Xiromed

The Global Docetaxel Market was valued at USD 1.37 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 2.37 billion by 2034. This growth is largely driven by the increasing incidence of various cancers, including breast, lung, prostate, and gastric cancers, where docetaxel is widely used. As a second-generation taxane, docetaxel stabilizes microtubules and halts the division of cancer cells, making it a crucial part of chemotherapy regimens. It is particularly effective in combination therapies, helping to improve survival rates for patients with advanced cancers, such as triple-negative breast cancer and castration-resistant prostate cancer. Additionally, innovations in drug delivery methods, such as nanoparticle formulations and liposomal encapsulations, have improved their bioavailability and reduced toxicity, expanding their clinical applications.

The growing approvals for biosimilars and generic docetaxel are making the drug more accessible, particularly in lower-middle-income regions, while the increasing focus on oncology R&D boosts demand for this essential cytotoxic agent. Digital health technologies also play a role by enabling better treatment personalization through remote monitoring of treatment responses and side effects. Furthermore, greater cancer awareness, urbanization, and early diagnosis efforts are contributing to the broader reliance on chemotherapy and drugs like docetaxel.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.37 Billion |

| Forecast Value | $2.37 Billion |

| CAGR | 5.7% |

The branded segment of the docetaxel market generated USD 725.8 million in 2024, benefiting from the established clinical reputation and efficacy of original formulations. Despite the presence of generics, branded products continue to dominate in developed markets due to their trusted safety profiles, regulatory approvals, and high-quality standards. Branded docetaxel is often preferred by oncologists for treating complex cancers such as breast cancer, non-small cell lung cancer (NSCLC), and prostate cancer, particularly in hospital settings. Moreover, the investment in new delivery methods and combination therapies further strengthens the brand's value.

In 2024, breast cancer segment held 32.3% driven by early and advanced treatment regimens for HER2-negative and triple-negative breast cancer patients. It is commonly used in combination treatments like TAC (docetaxel, doxorubicin, and cyclophosphamide), which have been shown to improve survival outcomes. Advances in personalized oncology systems continue to increase the demand for docetaxel in managing breast cancer cases.

U.S. Docetaxel Market was valued at USD 497.2 million in 2024. Factors such as favorable reimbursement policies, growing precision oncology services, and a focus on personalized medicine are fueling the demand. Furthermore, the expansion of outpatient chemotherapy access, increasing cancer awareness, and continuous clinical research are reinforcing the U.S. market's growth. The role of the U.S. as a key market is further strengthened by strategic partnerships between pharmaceutical companies and research centers, which accelerate drug development and market growth.

Leading players in the Global Docetaxel Industry include Alchem International, Alkem Labs, Arch Pharmalabs, Aspen Pharmacare, Cipla, Cisen Pharmaceutical, LGM Pharma, Phyton Biotech, Qilu Pharmaceutical, Teva Active Pharmaceutical Ingredients (TAPI), Teva Pharmaceuticals, Venus Remedies, and Xiromed. Companies operating in the docetaxel market are focusing on expanding their product portfolios by offering new formulations, delivery methods, and combination therapies. Partnerships with research institutions and hospitals are vital to enhancing the clinical applications and adoption of docetaxel. Many players are investing in biosimilars and generics to tap into cost-sensitive markets, ensuring broader access to this essential drug. Additionally, the development of personalized medicine and advanced digital health technologies allows companies to better cater to patient needs, improving treatment outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Indication

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global cancer prevalence

- 3.2.1.2 Increasing adoption of combination therapies

- 3.2.1.3 Favorable regulatory approvals and guidelines

- 3.2.1.4 Technological advancements in drug formulation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Severe side effects and toxicity concerns

- 3.2.2.2 Patent expirations and generic competition

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of personalized oncology treatment approaches

- 3.2.3.2 Increasing investments in oncology research and development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Reimbursement scenario

- 3.10.1 Impact of reimbursement policies on market growth

- 3.11 Consumer behaviour analysis

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded

- 5.3 Generics

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Breast cancer

- 6.3 Non-small cell lung cancer (NSCLC)

- 6.4 Hormone refractory prostate cancer

- 6.5 Gastric adenocarcinoma

- 6.6 Head and neck squamous cell carcinoma (HNSCC)

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Oncology clinics

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alchem International

- 9.2 Alkem Labs

- 9.3 Arch Pharmalabs

- 9.4 Aspen Pharmacare

- 9.5 Cipla

- 9.6 Cisen Pharmaceutical

- 9.7 LGM Pharma

- 9.8 Phyton Biotech

- 9.9 Qilu Pharmaceutical

- 9.10 Teva Active Pharmaceutical Ingredients (TAPI)

- 9.11 Teva Pharmaceuticals

- 9.12 Venus Remedies

- 9.13 Xiromed