ペストリーとケーキの市場機会と促進要因、産業動向分析、2025~2034年予測

Pastry and Cakes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766232

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

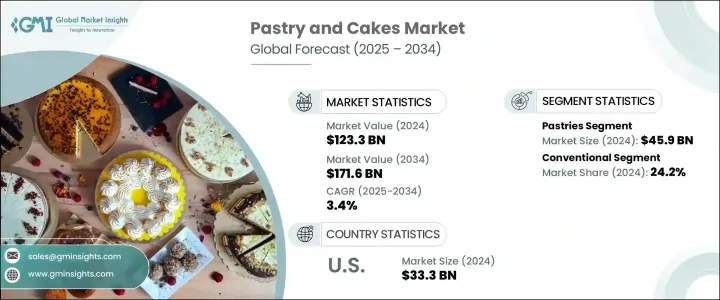

ペストリーとケーキの世界市場規模は2024年に1,233億米ドルとなり、CAGR 3.4%で成長し、2034年には1,716億米ドルに達すると予測されています。

地域や所得階層を超えた祝賀文化の高まりが、この市場を牽引する重要な役割を果たし続けています。消費者が日常のひとときや特別な日を記念して贅沢な食品にますます傾倒する中、ペストリーとケーキは感情的・社会的消費の両方で好まれる選択肢となっています。日常的な贅沢品への欲求による支出優先順位のシフトが、この動向にさらに拍車をかけています。焼き菓子は世界の食習慣の一貫であり、特にイベントや集まりの際には、その意義は単なる栄養補給にとどまらず、社会的表現や贈答の領域にまで及んでいます。

先進経済諸国でも新興経済諸国でも、焼き菓子は広く普及し続けています。ライフスタイルの進化や都市化の進展と相まって、利便性という要因が、人々が甘味スナックをいつ、どのように消費するかに一貫した変化をもたらしています。コンパクトでレディトゥイート焼き菓子は、特に消費者がペースの速い生活に合った商品を求めるようになり、人気が高まっています。この変化は、ペストリーやケーキの品揃えを充実させた食品小売店、スーパーマーケット、ハイパーマーケット、専門店の業績上昇にも反映されています。さらに、カフェ、ホテル、レストランなどの商業部門は、フォーマット、時間帯、顧客層を超えてこれらの商品を提供することで、市場収益に大きく貢献しています。

| 市場規模 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 1,233億米ドル |

| 予測金額 | 1,716億米ドル |

| CAGR | 3.4% |

市場成長のかなりの部分は、世界の中産階級の増加と、国際的な食の影響にさらされることにも関連しています。多様な食体験に対する意識が高まるにつれて、ペストリーとケーキのカテゴリー全体でも、製品デザイン、材料、フォーマットのどれをとっても、バラエティに対する需要が高まっています。オーガニック、グルテンフリー、ヴィーガン、低糖質など、食事に特化したバリエーションへの関心が高まる中、イノベーションへの動きも見られます。これらの商品は、味と満足感を提供しながらも、健康志向の消費者の支持を集めています。需要は、家庭で消費するために購入する住宅顧客と、より健康的でありながら贅沢な選択肢でメニューを一新しようとする業務用バイヤーの両方によって煽られています。

市場へのリーチと浸透という点では、実店舗が引き続き優位を占めているが、デジタルの状況も重要な手段として台頭してきています。オンライン小売チャネルは、様々な地域の消費者へのアクセスを拡大する上で、ますます重要になってきています。消費者への直接配送モデルとeコマース機能の強化により、ブランドは新たな人口動態の機会を引き出し、伝統的都市市場を超えて顧客基盤を拡大しています。

ペストリー部門だけでも、2024年の市場規模は459億米ドルで、2025~2034年のCAGRは2.7%と予測されています。このセグメントは市場全体で最大のシェアを占めており、その普遍的な魅力と、手軽なスナックからお祝いのお菓子まで、さまざまな消費シーンへの適応性がその原動力となっています。従来型小売店でもフードサービス店でも簡単に入手できることが、この製品の幅広い魅力に貢献しています。さらに、携帯性とポーションコントロールにより、ペストリーは嗜好性と消費しやすさの両方を求める消費者にとって便利な選択肢となっています。

材料別では、従来型セグメントが2024年に298億米ドルの金額で市場をリードし、シェア全体の24.2%を占めました。予測期間中のCAGRは3.3%で成長すると予想されます。従来型原料の優位性は、その汎用性、調達の容易さ、消費者の親しみやすさに起因します。これらの製品は、メーカーがスケールメリットの恩恵を受けながら、品質と味の一貫性を維持することを可能にします。また、先進市場でも成長市場でも広く受け入れられていることから競合もあり、市場への浸透を深め、流通戦略を合理化することができます。

米国は世界市場への主要貢献国として際立っており、2024年のペストリーとケーキ部門の市場規模は333億米ドルとなりました。2025~2034年のCAGRは3.3%で拡大すると予測されています。同国では、ベーカリー、専門店、クイックサービスレストランが数多く存在し、ベーカリーに対する消費支出が旺盛であるため、需要水準は常に高く維持されています。製品の革新、頻繁な季節キャンペーン、機能性成分の配合は、消費者の関心を維持するために用いられている戦略です。デジタルプラットフォームやアプリを使った注文の利便性は、特に郊外や都市部でのアクセスをさらに強化しています。

世界市場の競合情勢は、製品開発、ブランディング、消費者リーチの拡大に注力する数多くの大手企業によって形成されています。競合の中心は、高所得層を対象とした健康志向の製剤にますますシフトしており、各ブランドはウェルネス志向の製品ラインへと製品をシフトさせています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

- TAM分析、2025~2034年

- CXOの視点:戦略的必須事項

- 経営上の意思決定ポイント

- 重要な成功要因

- 将来の展望と戦略的提言

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 高級品や職人技の製品に対する需要の高まり

- インスタント食品の消費量の増加

- 可処分所得の増加と都市化

- カフェ文化とベーカリーチェーンの拡大

- 産業の潜在的リスク・課題

- 健康と食事に関する懸念

- 原料価格の変動

- 市場機会

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測、製品タイプ別、2021~2034年

- 主要動向

- ケーキ

- レイヤーケーキ

- カップケーキ

- シートケーキ

- チーズケーキ

- お祝いケーキ

- その他

- ペストリー

- デニッシュペストリー

- クロワッサン

- パイ生地

- エクレア

- タルト

- その他

- 甘味パイ

- フルーツパイ

- クリームパイ

- その他

- デザートバーとブラウニー

- その他

第6章 市場推定・予測、コンポーネント別、2021~2034年

- 主要動向

- 従来型

- オーガニック

- グルテンフリー

- 無糖/減糖

- ヴィーガン

- その他

第7章 市場推定・予測、流通チャネル別、2021~2034年

- 主要動向

- 小売パン屋

- 職人パン屋

- チェーン店のベーカリー

- スーパーマーケットとハイパーマーケット

- コンビニエンスストア

- 専門食品店

- オンライン小売

- eコマースプラットフォーム

- 消費者直接販売ウェブサイト

- 食品サービス部門

- カフェやレストラン

- ホテル

- ケータリングサービス

- その他

第8章 市場推定・予測、最終用途別、2021~2034年

- 主要動向

- 住宅用

- 業務用

- カフェやベーカリーチェーン

- レストランとホテル

- ケータリングサービス

- イベント運営会社

- その他

第9章 市場推定・予測、地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AAK AB

- Archer Daniels Midland Company

- Associated British Foods plc

- Bakels Group

- BASF SE

- Cargill, Incorporated

- Corbion N.V.

- Dawn Food Products, Inc.

- DuPont de Nemours, Inc.

- Flowers Foods, Inc.

- General Mills, Inc.

- Grupo Bimbo, S.A.B. de C.V.

- Ingredion Incorporated

- Kerry Group plc

- Koninklijke DSM N.V.

- Lesaffre Group

- Mondelez International, Inc.

- Puratos Group

- DSM-Firmenich AG

- Tate & Lyle PLC

目次

The Global Pastry and Cakes Market was valued at USD 123.3 billion in 2024 and is estimated to grow at a CAGR of 3.4% to reach USD 171.6 billion by 2034. The rising culture of celebration across regions and income brackets continues to play a significant role in driving this market. As consumers increasingly lean toward indulgent food items to commemorate daily moments and special occasions alike, pastries and cakes have become a preferred choice for both emotional and social consumption. The shift in spending priorities, driven by a desire for everyday luxuries, has fueled this trend further. With baked goods being a consistent part of global dietary habits, particularly during events and gatherings, their significance goes beyond simple nourishment and enters the territory of social expression and gifting.

In both established and developing economies, baked goods continue to witness widespread adoption. The convenience factor-combined with evolving lifestyles and increasing urbanization-is leading to consistent changes in how and when people consume sweet snacks. Compact, ready-to-eat baked items are enjoying growing popularity, especially as consumers seek out products that match their fast-paced lives. This shift is also mirrored in the rising performance of food retailers, supermarkets, hypermarkets, and specialty outlets that now feature an expanded array of pastry and cake products. Moreover, commercial sectors such as cafes, hotels, and restaurants are contributing notably to market revenues by offering these items across formats, time slots, and customer segments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $123.3 Billion |

| Forecast Value | $171.6 Billion |

| CAGR | 3.4% |

A significant portion of market growth is also tied to the growing global middle class and its exposure to international food influences. As awareness around diverse culinary experiences rises, so does the demand for variety across the pastry and cake category, whether it's in terms of product design, ingredients, or formats. A move toward innovation is visible, with increasing interest in diet-specific variants such as organic, gluten-free, vegan, and low-sugar options. These offerings are gaining favor among health-conscious consumers while still delivering on flavor and satisfaction. The demand is being fueled by both residential customers buying for home consumption and commercial buyers looking to update their menus with healthier yet indulgent choices.

While brick-and-mortar stores continue to dominate in terms of market reach and penetration, the digital landscape is emerging as a key enabler. Online retail channels are becoming increasingly crucial in expanding access to consumers across diverse geographies. With direct-to-consumer delivery models and enhanced e-commerce capabilities, brands are unlocking new demographic opportunities and increasing their customer base beyond traditional urban markets.

The pastry segment alone was valued at USD 45.9 billion in 2024 and is projected to register a CAGR of 2.7% from 2025 to 2034. This segment holds the largest share of the overall market, driven by its universal appeal and adaptability across various consumption scenarios-from quick snacks to celebratory treats. Easy availability through both traditional retail and foodservice outlets contributes to its widespread appeal. Additionally, portability and portion control make pastries a convenient choice for consumers seeking both indulgence and ease of consumption.

In terms of ingredients, the conventional segment led the market with a value of USD 29.8 billion in 2024, accounting for 24.2% of the total share. It is expected to grow at a CAGR of 3.3% over the forecast period. The dominance of conventional ingredients stems from their versatility, ease of procurement, and consumer familiarity. These products enable manufacturers to maintain consistency in quality and taste while benefiting from economies of scale. Their wide acceptance in both advanced and growing markets also provides them with a competitive edge, allowing for deeper market penetration and streamlined distribution strategies.

The United States stood out as a key contributor to the global market, with the pastry and cakes sector valued at USD 33.3 billion in 2024. It is anticipated to expand at a CAGR of 3.3% from 2025 through 2034. The country's strong consumer spending on baked goods, coupled with a robust presence of retail bakeries, specialty stores, and quick-service restaurants, keeps demand levels consistently high. Product innovation, frequent seasonal campaigns, and the inclusion of functional ingredients are strategies being used to maintain consumer interest. The convenience of digital platforms and app-based ordering has further strengthened accessibility, particularly in suburban and urban areas.

The competitive landscape of the global market is shaped by numerous leading players focused on product development, branding, and expanding their consumer reach. Competition is increasingly centered around health-forward formulations aimed at high-income consumers, leading brands to shift their offerings toward wellness-driven product lines.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1.1 Regional

- 2.2.1.2 Product type

- 2.2.1.3 Ingredient

- 2.2.1.4 Distribution channel

- 2.2.1.5 End use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for premium and artisanal products

- 3.2.1.2 Increasing consumption of convenience foods

- 3.2.1.3 Rising disposable income and urbanization

- 3.2.1.4 Expanding cafe culture and bakery chains

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Health and dietary concerns

- 3.2.2.2 Fluctuating raw material prices

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cakes

- 5.2.1 Layer cakes

- 5.2.2 Cupcakes

- 5.2.3 Sheet cakes

- 5.2.4 Cheesecakes

- 5.2.5 Celebration cakes

- 5.2.6 Others

- 5.3 Pastries

- 5.3.1 Danish pastries

- 5.3.2 Croissants

- 5.3.3 Puff pastries

- 5.3.4 Eclairs

- 5.3.5 Tarts

- 5.3.6 Others

- 5.4 Sweet pies

- 5.4.1 Fruit pies

- 5.4.2 Cream pies

- 5.4.3 Others

- 5.5 Dessert bars and brownies

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Ingredient, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Organic

- 6.4 Gluten-free

- 6.5 Sugar-free / reduced sugar

- 6.6 Vegan

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Retail bakeries

- 7.2.1 Artisanal bakeries

- 7.2.2 Chain bakeries

- 7.3 Supermarkets and hypermarkets

- 7.4 Convenience stores

- 7.5 Specialty food stores

- 7.6 Online retail

- 7.6.1 E-commerce platform

- 7.6.2 Direct-to-consumer websites

- 7.7 Food service sector

- 7.7.1 Cafes and restaurants

- 7.7.2 Hotels

- 7.7.3 Catering services

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Cafes and bakery chains

- 8.3.2 Restaurants and hotels

- 8.3.3 Catering services

- 8.3.4 Event management companies

- 8.3.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AAK AB

- 10.2 Archer Daniels Midland Company

- 10.3 Associated British Foods plc

- 10.4 Bakels Group

- 10.5 BASF SE

- 10.6 Cargill, Incorporated

- 10.7 Corbion N.V.

- 10.8 Dawn Food Products, Inc.

- 10.9 DuPont de Nemours, Inc.

- 10.10 Flowers Foods, Inc.

- 10.11 General Mills, Inc.

- 10.12 Grupo Bimbo, S.A.B. de C.V.

- 10.13 Ingredion Incorporated

- 10.14 Kerry Group plc

- 10.15 Koninklijke DSM N.V.

- 10.16 Lesaffre Group

- 10.17 Mondel?z International, Inc.

- 10.18 Puratos Group

- 10.19 DSM-Firmenich AG

- 10.20 Tate & Lyle PLC

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日