|

市場調査レポート

商品コード

1766226

バスキュラーアクセスデバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Vascular Access Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| バスキュラーアクセスデバイスの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月13日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

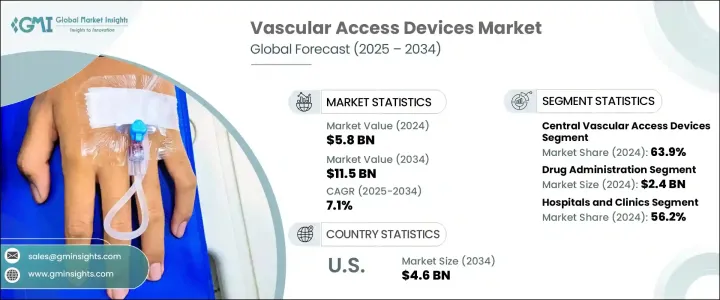

バスキュラーアクセスデバイスの世界市場規模は、2024年に58億米ドルとなり、CAGR7.1%で成長し、2034年までには115億米ドルに達すると予測されています。

これらの機器の需要は、長期的または反復的な静脈内治療を必要とする慢性的な健康状態の負担の増加によって推進されています。ヘルスケア全般において、重篤な疾患の治療を受けている患者は、持続的な薬剤投与、栄養補給、水分管理を必要とすることが多く、信頼性の高いバスキュラーアクセスソリューションが求められています。

臨床現場では、バスキュラーアクセスデバイスは、薬剤の供給、採血、輸液、その他の重要な処置の実施に不可欠です。集中治療、外科処置、特殊治療を必要とする患者の増加に伴い、その役割はさらに重要になっています。新興諸国ではヘルスケアシステムが拡大し、既存市場では技術がアップグレードされるにつれて、急性期、非急性期を問わずバスキュラーアクセスデバイスへのニーズは高まり続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 58億米ドル |

| 予測金額 | 115億米ドル |

| CAGR | 7.1% |

これらのデバイスは、さまざまな治療のために血流に直接、効率的にアクセスできるように特別に設計されています。外科手術のような短期的なシナリオから、透析や化学療法のような長期的な治療まで、幅広く使用されています。ヘルスケアの状況がより外来患者や在宅ケアモデルへとシフトするにつれ、病院外でのこれらの機器の使用も増加しています。器具の素材やデザインにおける技術革新は、感染症や血栓などの合併症を最小限に抑え、医療従事者の使いやすさを向上させるなど、安全性の向上に貢献しています。このように、バスキュラーアクセスデバイスは、患者の安全性と手技の効率性の両方を確保し、現代のヘルスケア提供に不可欠なものとなっています。

同市場は末梢型と中枢型に分類されます。2024年には、中心バスキュラーアクセスデバイスが圧倒的な地位を占め、市場総売上の63.9%を生み出しています。これらのデバイスは、特に複雑な治療レジメンにおいて、一貫したまたは繰り返しの静脈内治療を必要とする状況で頻繁に好まれています。長時間の留置が可能で、太い静脈に直接薬剤を送り込むことができるため、特に長期間の使用に適しています。さまざまなセントラルアクセスオプションの中でも、末梢挿入型セントラルカテーテル、トンネル型カテーテル、埋め込み型ポートなどのデバイスは、挿入頻度が低く患者の快適性が向上するため、広く使用されています。

このセグメントにおける最近の動向は、抗菌特性や抗凝血機能を改善したバスキュラー器具の開発につながっています。こうした製品のアップグレードは、カテーテル関連血流感染などの長期使用に伴うリスクを最小限に抑え、機器の信頼性を高めることを目的としています。さらに、挿入手技に画像技術を統合することで、より正確で安全な挿入が可能になり、治療プロトコルの全体的な効率化に寄与しています。

アプリケーションの観点からは、薬剤投与が最も高い収益を占め、2024年には24億米ドルに達します。この分野は、慢性疾患患者における持続点滴療法のニーズの高まりにより、引き続き成長しています。抗生物質、生物学的製剤、免疫療法などの薬剤は、しばしば長時間の点滴アクセスを必要とするため、バスキュラーアクセスデバイスが不可欠となっています。医療現場では、入院コストを削減するために在宅輸液サービスや外来治療を支援する傾向が強まっており、バスキュラーアクセスツールは在宅医療環境でも一般的になりつつあります。

市場はまた、病院・診療所、外来手術センター、在宅ケア環境、その他を含むエンドユーザー別に区分されます。病院・診療所が主要セグメントとして浮上しており、2024年の市場シェアは56.2%です。手術件数の一貫した増加に加え、急性期治療と慢性期治療の両方で患者流入が増加しているため、これらの施設ではバスキュラー器具の需要が高まっています。これらの施設では、日常的な処置には末梢静脈路、より複雑な治療には中心静脈路の両方が頻繁に使用されます。感染予防と規制基準の遵守は重要な関心事であるため、病院は閉鎖システム設計と抗菌材料を組み込んだ高度なアクセスデバイスへの投資を促しています。

地域別では北米が市場をリードし、2024年には26億米ドルの収益を上げ、今後10年間のCAGRは7%で成長すると予測されています。この地域では、米国が2024年の23億米ドルから2034年までには46億米ドルに成長すると予測されています。長期的な健康状態の蔓延の増加と、外来治療や在宅治療プログラムへのシフトが、市場の継続的拡大を支えています。効果的で耐久性があり、より安全なバスキュラーアクセスオプションに対する需要は依然として高く、質の高い治療結果と患者中心のソリューションを求めるヘルスケアプロバイダーがその原動力となっています。

同市場の競合情勢には、技術革新と製品性能に重点を置く業界の有力企業が含まれます。Becton Dickinson and Company、Teleflex、B. Braun、Medtronic、Fresenius Medical Careなどの企業が、2024年の世界市場シェアの約60%を占めています。市場力学は、特に価格に敏感な地域では、製品技術の進歩やコストへの配慮に大きく影響されます。多国籍企業はしばしば、手頃な価格と品質のバランスを取る必要に迫られる一方、現地メーカーはコスト効率に優れ、なおかつコンプライアンスに適合した代替品のプロバイダーとしての地位を確立しています。イノベーションとアクセシビリティのバランスは、今後もバスキュラーアクセスデバイス市場の特徴であり続けると考えられています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- 慢性疾患の有病率の増加

- 低侵襲手術への関心の高まり

- 技術的進歩

- 在宅ヘルスケアの需要の高まり

- 業界の潜在的リスク・課題

- カテーテル関連血流感染症(CRBSI)のリスクが高め

- 高度なバスキュラーアクセスデバイスの高コスト

- 成長促進要因

- 成長可能性分析

- テクノロジーの情勢

- 価格分析

- ギャップ分析

- 将来の市場動向

- 規制情勢

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 周辺機器バスキュラーアクセスデバイス

- 中心バスキュラーアクセスデバイス

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 薬剤投与

- 水分・栄養の投与

- 輸血

- 診断検査

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 外来手術センター

- 在宅医療

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Access Vascular

- AngioDynamics

- B Braun

- Becton Dickinson and Company

- ConvaTec

- Cook Medical

- Fresenius Medical Care

- ICU Medical

- Medical Components

- Medtronic

- Nipro

- Penumbra

- Teleflex

- Terumo

- Vygon

The Global Vascular Access Devices Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 11.5 billion by 2034. Demand for these devices is being propelled by the rising burden of chronic health conditions that require long-term or repeated intravenous therapies. Across the healthcare spectrum, patients undergoing treatment for serious ailments often require sustained drug delivery, nutritional support, or fluid management, which calls for dependable vascular access solutions.

In clinical settings, vascular access devices are essential for delivering medications, drawing blood, administering fluids, and performing other critical procedures. Their role becomes even more vital with the growing number of patients needing intensive care, surgical procedures, and specialized treatments. As healthcare systems expand in developing countries and upgrade technologies in established markets, the need for vascular access equipment continues to grow in both acute and non-acute care environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 7.1% |

These devices are specifically designed to provide direct and efficient access to the bloodstream for a range of treatments. They are widely used in both short-term scenarios, such as surgical procedures, and for long-duration therapies like dialysis or chemotherapy. As the healthcare landscape shifts toward more outpatient and home-based care models, the use of these devices outside hospital settings is also gaining traction. Innovations in device materials and design have contributed to greater safety, minimizing complications like infections and blood clots, and improving ease of use for medical personnel. Vascular access equipment has thus become integral to modern healthcare delivery, ensuring both patient safety and procedural efficiency.

The market is categorized into peripheral and central vascular access devices. In 2024, central vascular access devices held the dominant position, generating 63.9% of the total market revenue. These devices are frequently preferred in situations requiring consistent or repeated intravenous treatments, especially in complex therapeutic regimens. Their ability to remain in place for extended durations and deliver drugs directly into large veins makes them particularly suitable for long-term applications. Among the various central access options, devices such as peripherally inserted central catheters, tunneled catheters, and implantable ports are widely used due to their lower insertion frequency and enhanced patient comfort.

Recent advancements in this segment have led to the development of vascular devices with improved antimicrobial properties and anti-clotting features. These product upgrades are designed to minimize risks associated with prolonged usage, such as catheter-related bloodstream infections, and enhance device reliability. Additionally, the integration of imaging technologies in insertion techniques has made placements more accurate and safer, contributing to the overall efficiency of treatment protocols.

From an application standpoint, drug administration accounted for the highest revenue, reaching USD 2.4 billion in 2024. This segment continues to thrive due to the growing need for continuous infusion therapies in patients with chronic illnesses. Medications, including antibiotics, biologics, and immunotherapies, often require prolonged intravenous access, which makes vascular access devices indispensable. As medical practices increasingly support home infusion services and outpatient therapy to reduce hospitalization costs, vascular access tools are becoming more common in homecare environments as well.

The market is also segmented by end users, including hospitals and clinics, ambulatory surgical centers, homecare settings, and others. Hospitals and clinics emerged as the leading segment, with a market share of 56.2% in 2024. The consistent rise in surgical volumes, along with a higher patient inflow for both acute and chronic care, sustains a strong demand for vascular devices in these facilities. These settings frequently utilize both peripheral IVs for routine procedures and central lines for more complex treatment needs. Infection prevention and compliance with regulatory standards are critical concerns, prompting hospitals to invest in advanced access devices that incorporate closed-system designs and antimicrobial materials.

Regionally, North America led the market, generating USD 2.6 billion in revenue in 2024 and is forecasted to grow at a CAGR of 7% over the next decade. Within this region, the United States is expected to see its vascular access device market grow from USD 2.3 billion in 2024 to USD 4.6 billion by 2034. The increasing prevalence of long-term health conditions, combined with a shift toward outpatient care and at-home treatment programs, supports continued market expansion. The demand for effective, durable, and safer vascular access options remains high, driven by healthcare providers striving for quality outcomes and patient-centered solutions.

The competitive landscape of the market includes prominent industry players that focus on innovation and product performance. Companies such as Becton Dickinson and Company, Teleflex, B. Braun, Medtronic, and Fresenius Medical Care collectively captured approximately 60% of the global market share in 2024. Market dynamics are heavily influenced by advancements in product technology and cost considerations, particularly in price-sensitive regions. Multinational corporations often face pressure to balance affordability with quality, while local manufacturers position themselves as providers of cost-effective yet compliant alternatives. This balance between innovation and accessibility will remain a defining feature of the vascular access devices market in the years ahead.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Growing preference for minimally invasive procedures

- 3.2.1.3 Technological advancements

- 3.2.1.4 Rising demand for home healthcare

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High risk of catheter-related bloodstream infections (CRBSIs)

- 3.2.2.2 High cost of advanced vascular access devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Pricing analysis

- 3.6 Gap analysis

- 3.7 Future market trends

- 3.8 Regulatory landscape

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Peripheral vascular access devices

- 5.3 Central vascular access devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Drug administration

- 6.3 Fluid and nutrition administration

- 6.4 Blood transfusion

- 6.5 Diagnostic testing

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers

- 7.4 Homecare settings

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Access Vascular

- 9.2 AngioDynamics

- 9.3 B Braun

- 9.4 Becton Dickinson and Company

- 9.5 ConvaTec

- 9.6 Cook Medical

- 9.7 Fresenius Medical Care

- 9.8 ICU Medical

- 9.9 Medical Components

- 9.10 Medtronic

- 9.11 Nipro

- 9.12 Penumbra

- 9.13 Teleflex

- 9.14 Terumo

- 9.15 Vygon