自動車用回生ショックアブソーバーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Automotive Regenerative Shock Absorbers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766201

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

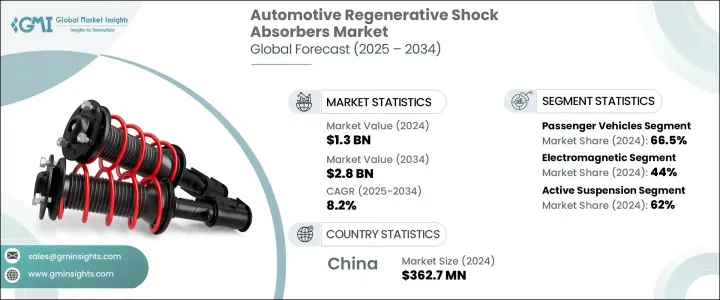

自動車用回生ショックアブソーバーの世界市場は、2024年には13億米ドルとなり、CAGR 8.2%で成長し、2034年には28億米ドルに達すると予測されています。

エネルギー効率の高い車両システムと燃料性能の向上に対する需要の高まりが、回生ショックアブソーバーの採用を後押しし続けています。これらのシステムは、サスペンションの動きや路面の振動によって生じる運動エネルギーを使用可能な電気に変換し、車両全体の効率に貢献します。電動化の動向が加速し、世界的に環境規制が強化されるにつれて、自動車メーカーは電気自動車、ハイブリッド車、従来型自動車により広くこのシステムを組み込むようになっています。車両サスペンション技術の進歩は、商用車と乗用車の両方に適用範囲を広げ、回生ソリューションをより現実的なものにしています。メーカーは、乗り心地とシステムの応答性を向上させながら燃費を支え、排出基準を満たすために、エネルギー回収技術に目を向けています。

自動車部門はエネルギー回収ソリューションにシフトしており、回生ショックアブソーバーは運転効率を達成するための重要なコンポーネントとして浮上しています。これらのシステムは、道路エネルギーを電気出力に再利用し、従来のエネルギー依存度を低下させる。低排出ガスと燃費向上を求める世界の規制の強化により、OEMはコンプライアンス戦略の一環としてエネルギー変換サスペンション技術の採用を迫られています。このような状況の中で、回生減衰システムは、さまざまな車両クラスや使用事例で脚光を浴びつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 13億米ドル |

| 予測金額 | 28億米ドル |

| CAGR | 8.2% |

2024年には乗用車が66.5%のシェアで市場をリードし、2034年までCAGR 8.5%で成長すると予測されます。乗用車の生産と販売が世界的に広がっていることが、この動向の大きな力となっています。消費者は、よりスムーズな乗り心地、優れたハンドリング、優れた燃費効率を提供する自動車をますます好むようになっています。その結果、回生ショックアブソーバーは普通乗用車にも高級乗用車にも搭載されるようになっています。自動車メーカーが航続距離の向上と環境負荷の低減に努めているため、電気自動車やハイブリッド乗用車の急速な普及がこの傾向をさらに加速させています。持続可能性の目標を達成しようとする相手先商標製品メーカーの努力は、電磁ダンパーと機械式ダンパーの統合を促しています。継続的な研究開発費と支援的な政府のイニシアチブは、技術革新を加速させ、このセグメントにおける回生サスペンションシステムの採用を強化しています。

電磁式回生ショックアブソーバーは、2024年には44%を占めて最大の市場シェアを占め、2025~2034年にはCAGR 8.3%で成長すると予測されています。これらのシステムは、電磁誘導を利用して路面の誘導運動からエネルギーを利用し、機械抵抗を最小限に抑えながら発電します。高効率で応答性に優れた設計により、従来の油圧式や機械式システムよりも優位性があります。OEM各社は、プレミアムモデルや電動モデルに電磁サスペンションを採用し、省エネ効果を得ながら性能を最大化しています。世界の嗜好がインテリジェントで効率的なモビリティソリューションにシフトするなか、このセグメントへの関心が高まり、急速に拡大しています。

中国の自動車用回生ショックアブソーバー2024年の市場規模は3億6,270万米ドルで、シェアは69%。電気自動車の急速な普及は、現地でのサスペンション製造の進歩と相まって、中国を重要な成長ハブに位置づけています。電気自動車のバッテリー設計が重くなったことで、ハンドリングと乗り心地を改善する高度な衝撃吸収ソリューションの必要性が高まっています。中国の強固な自動車製造エコシステムは、国内の技術革新と研究開発への多額の投資とともに、回生サスペンションシステムの採用を後押ししています。電動モビリティと産業変革に対する政府の後押しが、軽量化と適応技術の開発をさらに後押ししています。性能と燃費に戦略的に重点を置く同国は、世界市場の拡大に大きく貢献しています。

自動車用回生ショックアブソーバーの世界市場を形成する主要企業には、ZF Friedrichshafen、SACHS、Trelleborg、Hitachi Astemo、KYB、Mando、Fox Factory、Endurance Technologies、ThyssenKrupp Bilstein、BWI Groupなどがあります。自動車用回生ショックアブソーバー市場での地位を固めるため、主要企業は技術革新、持続可能性、戦略的提携に注力しています。多くの企業は、モビリティの電動化に対応した電磁式および機械式のエネルギー回収システムを強化するため、研究開発投資を強化しています。メーカーはOEMと提携し、これらの技術を次世代電気自動車やハイブリッド車に統合しようとしています。もうひとつの主要戦略には、現地生産部門を通じた新興EV市場への地理的拡大が含まれます。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 電気自動車とハイブリッド車の需要増加

- 自動車技術の進歩

- ADAS(先進運転支援システム)(ADAS)との統合

- 快適性と安全性への需要の高まり

- 車両航続距離の延長の可能性

- 業界の潜在的リスク&課題

- 原材料価格の変動

- 激しい競合

- 市場機会

- 電気自動車(EV)との統合

- 自動運転車の導入増加

- プレミアム車と高級車の販売が増加

- 先進サスペンションシステムの研究開発資金

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- 電磁

- 油圧式

- 機械

- その他

第7章 市場推計・予測:サスペンション, 2021年~2034年

- 主要動向

- アクティブサスペンション

- セミアクティブサスペンション

第8章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 補助システムへの電源供給

- バッテリー充電(EV)

- 燃費向上のためのエネルギー回収

- 自律走行車システム

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- ADD Industry

- AL-KO Vehicle Technology Group

- BWI Group

- Endurance Technologies

- FOX Factory

- Gabriel India

- Hitachi Astemo

- KONI

- KYB

- Magneti Marelli

- Mando

- Multimatic

- Ohlins Racing

- Ride Control

- SACHS

- Showa Corporation

- Tenneco

- Thyssenkrupp Bilstein

- Trelleborg

- ZF Friedrichshafen

目次

The Global Automotive Regenerative Shock Absorbers Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 8.2% to reach USD 2.8 billion by 2034. Increasing demand for energy-efficient vehicle systems and enhanced fuel performance continues to drive the adoption of regenerative shock absorbers. These systems convert kinetic energy, produced by suspension movement and road vibrations, into usable electricity, contributing to overall vehicle efficiency. As electrification trends accelerate and environmental regulations tighten worldwide, automakers are integrating these systems more broadly into electric, hybrid, and conventional vehicles. Advances in vehicle suspension technologies are expanding the application scope across both commercial and passenger vehicles, making regenerative solutions more viable. Manufacturers are turning to energy-harvesting technologies to support fuel economy and meet emissions standards while improving ride quality and system responsiveness.

The automotive sector is shifting toward energy recovery solutions, and regenerative shock absorbers are emerging as key components in achieving operational efficiency. These systems repurpose road energy into electrical output, lowering traditional energy dependency. Stricter global mandates for lower emissions and improved fuel economy are pushing OEMs to embrace energy-converting suspension technologies as part of their compliance strategies. In this evolving landscape, regenerative damping systems are gaining prominence across various vehicle classes and use cases.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 8.2% |

In 2024, passenger vehicles led the market with a 66.5% share and are forecast to grow at 8.5% CAGR through 2034. The widespread production and sales of passenger cars worldwide are a major force behind this trend. Consumers are increasingly favoring vehicles that offer smoother rides, superior handling, and better fuel efficiency. As a result, regenerative shock absorbers are being incorporated into both standard and high-end passenger vehicles. The rapid growth of electric and hybrid passenger models is further accelerating this trend, as automakers strive to enhance range and reduce environmental impact. Efforts by original equipment manufacturers to meet sustainability goals are encouraging the integration of electromagnetic and mechanical dampers. Continued R&D spending and supportive government initiatives are accelerating innovation and bolstering the adoption of regenerative suspension systems in this segment.

Electromagnetic regenerative shock absorbers held the largest market share in 2024, accounting for 44%, and are projected to grow at a CAGR of 8.3% during 2025-2034. These systems harness energy from road-induced motion using electromagnetic induction, generating electricity while minimizing mechanical drag. Their high efficiency and responsive design give them an edge over traditional hydraulic or mechanical systems. OEMs are adopting electromagnetic suspension for premium and electric models to maximize performance while achieving energy-saving benefits. As global preferences shift toward intelligent and efficient mobility solutions, this segment is seeing heightened interest and rapid expansion.

China Automotive Regenerative Shock Absorbers Market generated USD 362.7 million in 2024 and held a 69% share. The rapid uptake of electric vehicles, coupled with advancements in local suspension manufacturing, has positioned China as a key growth hub. Heavier EV battery designs are driving the need for advanced shock absorption solutions that improve handling and ride quality. China's robust automotive manufacturing ecosystem, along with substantial investments in domestic innovation and R&D, is bolstering the adoption of regenerative suspension systems. Government backing for electric mobility and industry transformation is further encouraging the development of lightweight and adaptive technologies. The country's strategic focus on performance and fuel economy is making it a significant contributor to global market expansion.

Key players shaping the Global Automotive Regenerative Shock Absorbers Market include ZF Friedrichshafen, SACHS, Trelleborg, Hitachi Astemo, KYB, Mando, Fox Factory, Endurance Technologies, ThyssenKrupp Bilstein, and BWI Group. To solidify their position in the automotive regenerative shock absorbers market, leading companies are focusing on innovation, sustainability, and strategic collaborations. Many are ramping up R&D investments to enhance electromagnetic and mechanical energy recovery systems that align with the shift to electrified mobility. Manufacturers are partnering with OEMs to integrate these technologies into next-generation electric and hybrid vehicles. Another major strategy includes geographic expansion into emerging EV markets through localized production units.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Technology

- 2.2.4 Suspension

- 2.2.5 Sales channel

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for electric and hybrid vehicles

- 3.2.1.2 Advancements in automotive technology

- 3.2.1.3 Integration with advanced driver assistance systems (ADAS)

- 3.2.1.4 Rising demand for comfort and safety

- 3.2.1.5 Potential for extended vehicle range

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Volatility in raw material prices

- 3.2.2.2 Intense competition

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with electric vehicles (EVs)

- 3.2.3.2 The rise in adoption of autonomous vehicles

- 3.2.3.3 Growing premium and luxury vehicle sales

- 3.2.3.4 R&D funding in advanced suspension systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($ Billion, units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicles (LCV)

- 5.3.2 Medium commercial vehicles (MCV)

- 5.3.3 Heavy commercial vehicles (HCV)

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($ Billion, Units)

- 6.1 Key trends

- 6.2 Electromagnetic

- 6.3 Hydraulic

- 6.4 Mechanical

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Suspension, 2021 - 2034 ($ Billion, Units)

- 7.1 Key trends

- 7.2 Active suspension

- 7.3 Semi-active suspension

Chapter 8 Market Estimates & Forecast, By Sales channel, 2021 - 2034 ($ Billion, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Billion, Units)

- 9.1 Key trends

- 9.2 Power supply to auxiliary systems

- 9.3 Battery charging (EVs)

- 9.4 Energy recovery for fuel efficiency

- 9.5 Autonomous vehicle systems

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 ADD Industry

- 11.2 AL-KO Vehicle Technology Group

- 11.3 BWI Group

- 11.4 Endurance Technologies

- 11.5 FOX Factory

- 11.6 Gabriel India

- 11.7 Hitachi Astemo

- 11.8 KONI

- 11.9 KYB

- 11.10 Magneti Marelli

- 11.11 Mando

- 11.12 Multimatic

- 11.13 Ohlins Racing

- 11.14 Ride Control

- 11.15 SACHS

- 11.16 Showa Corporation

- 11.17 Tenneco

- 11.18 Thyssenkrupp Bilstein

- 11.19 Trelleborg

- 11.20 ZF Friedrichshafen

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日