|

市場調査レポート

商品コード

1766185

電気自動車(EV)用ベアリングの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年Electric Vehicle Bearings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電気自動車(EV)用ベアリングの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年 |

|

出版日: 2025年06月11日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

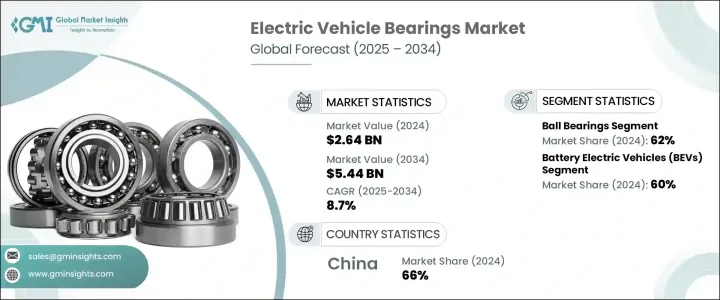

電気自動車(EV)用ベアリングの世界市場規模は、2024年に26億4,000万米ドルとなり、2034年には54億4,000万米ドルに達し、CAGRで8.7%の成長が予測されています。

電動モビリティへのシフトの高まりにより、電動ドライブトレインの効率、耐久性、性能を高める高度なベアリング技術のニーズが加速しています。市場の拡大は、高荷重に耐え、車両やバッテリーの寿命延長に貢献するエネルギー効率の高い低摩擦部品に対する需要の高まりが主な要因となっています。主要な自動車地域でEVの採用が進むにつれ、電気自動車特有の機械的・熱的ストレスに対応するよう設計された特殊ベアリングの需要が急速に高まっています。

世界各国の政府は、財政的な優遇措置や環境規制の強化によってこの移行を強化しており、自動車メーカーは軽量で精密設計のベアリングソリューションを優先するようになっています。さらに、高級電気自動車の生産台数が増加しているため、シームレスで洗練されたドライビング体験を提供する、超高信頼性でノイズを低減するコンポーネントへの需要が高まっています。電気自動車のドライブトレインアーキテクチャが進化し、マルチスピードシステムや統合されたe-アクスルが組み込まれるようになるにつれ、ベアリングサプライヤーは厳しい環境でも動作可能な高性能ソリューションを提供することが求められています。これに応えるため、大手メーカーは自動車セクターの高まる期待に応えるべく、設計革新を推し進めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 26億4,000万米ドル |

| 予測金額 | 54億4,000万米ドル |

| CAGR | 8.7% |

2024年、ボールベアリングは62%のシェアでEV用ベアリング市場をリードし、予測期間中のCAGRは9.8%を超えると予想されます。この分野は、大量生産をサポートし、一貫した品質を維持し、電動ドライブトレインの厳しい運用ニーズを満たす能力により、その地位を維持しています。摩擦を最小限に抑え、信頼性を最大限に高めることで知られるボールベアリングは、電気モーター、トランスミッション、ホイールハブなど、様々な電気自動車部品に広く組み込まれています。OEM(相手先商標製品製造会社)が、電動化、ADAS、インフォテインメント技術にまたがる次世代車両システムの展開を加速するにつれて、自動車メーカーは、独自の性能と耐久性のニーズに合わせた高度なエンジニアリングサービスとコンポーネントを求めるようになっています。

バッテリー電気自動車(BEV)は2024年に60%のシェアを占め、セグメントシェアで首位を確保します。BEVは、エネルギー効率の向上、高速運転、騒音の最小化をサポートする高精度部品を必要とすることで、電気自動車(EV)用ベアリングの状況を根本的に変えています。BEVシステムの性質上、最適な性能を維持しながら、より大きな熱変動と長期の動作サイクルに対応できるベアリングが要求されます。BEVが世界的に普及し続ける中、ベアリングメーカーは、高速電気モーターの進化する技術仕様に対応し、製品の長期的な信頼性を確保する高度なソリューションの開発に投資しています。

アジア太平洋の電気自動車(EV)用ベアリング市場は66%のシェアを占め、2024年には9億3,970万米ドルを創出しました。EV生産と輸出の世界的リーダーである中国は、強力な政策支援、拡大するサプライチェーン、急成長する国内自動車メーカーの恩恵を受けています。地元のベアリングメーカーは、研究開発を強化し、高効率の電気ドライブトレインに合わせた高性能ベアリングソリューションの生産を拡大することで、この需要に応えています。ベアリング技術の進歩への積極的な関与は、世界のEV用ベアリング市場における中心的なプレーヤーとしての地位を強調しています。

世界の電気自動車(EV)用ベアリング産業で革新と競争を牽引している主要企業には、 Schaeffler, SKF, JTEKT, NTN, Nachi-Fujikoshi, NSK, Timkenなどがあります。市場の足場を固めるため、電気自動車(EV)用ベアリングメーカーはいくつかの重点戦略を採用しています。これには、電気駆動系に最適化された高速、低摩擦、熱安定性の軸受技術を開発するための大規模な研究開発投資が含まれます。各社はまた、自動車メーカーと長期的なパートナーシップを結んでカスタムソリューションを共同開発し、統合されたe-モビリティプラットフォームへのシフトに歩調を合わせています。主要なEV市場、特にアジアと北米で製造拠点を拡大することも重要なアプローチです。さらに各社は、進化するドライブトレインアーキテクチャに対応する小型・軽量・高耐久設計を提供することで製品ポートフォリオを強化するとともに、エネルギー効率の向上とサービス間隔の延長を図っています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 政府の支援を受けて電気自動車の世界の普及が進む

- 軽量でスマートなベアリング技術の進歩により、効率と耐久性が向上します

- 新興市場におけるEV製造の拡大

- センサー対応ベアリングによる予測メンテナンスの統合

- 業界の潜在的リスク&課題

- 初期費用が高め

- 複雑な設置とメンテナンス

- 市場機会

- 世界のEV生産の急増

- OEMとの研究開発および共同開発

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- 価格動向

- 地域別

- コンポーネント別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推定・予測:タイプ別、2021年~2034年

- 主要動向

- ボールベアリング

- ローラーベアリング

- その他

第6章 市場推定・予測:車両別、2021年~2034年

- 主要動向

- バッテリー電気自動車(BEV)

- プラグインハイブリッド電気自動車(PHEV)

- ハイブリッド電気自動車(HEV)

- 燃料電池電気自動車(FCEV)

第7章 市場推定・予測:材料別、2021年~2034年

- 主要動向

- スチールベアリング

- セラミックベアリング

- ポリマーベアリング

- その他

第8章 市場推定・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推定・予測:ベアリングサイズ別、2021年~2034年

- 主要動向

- 小型ベアリング

- 中型ベアリング

- 大型ベアリング

第10章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

第11章 企業プロファイル

- ILJIN

- BRK

- C&U Group

- Fersa

- IKO Nippon Thompson

- JTEKT

- Luoyang LYC Bearing

- MinebeaMitsumi

- Nachi-Fujikoshi

- NBC

- NMB Technologies

- NSK

- NSK-Warner

- NTN

- RBC Bearings

- Schaeffler

- SKF

- The Timken

- THK

- ZWZ

The Global Electric Vehicle Bearings Market was valued at USD 2.64 billion in 2024 and is estimated to grow at a CAGR of 8.7% to reach USD 5.44 billion by 2034. The rising shift toward electric mobility is accelerating the need for advanced bearing technologies that enhance the efficiency, durability, and performance of electric drivetrains. Market expansion is largely driven by rising demand for energy-efficient, low-friction components that can withstand high loads and contribute to prolonged vehicle and battery life. With the growing adoption of EVs across major automotive regions, demand for specialized bearings designed to address the unique mechanical and thermal stresses of electric vehicles is increasing rapidly.

Governments worldwide are reinforcing this transition with financial incentives and tighter environmental regulations, prompting automakers to prioritize lightweight, precision-engineered bearing solutions. Additionally, the rising production of premium electric vehicles is fueling the demand for ultra-reliable, noise-reducing components that deliver seamless and refined driving experiences. As EV drivetrain architectures evolve-incorporating multi-speed systems and integrated e-axles-bearing suppliers are required to offer high-performance solutions capable of operating in demanding environments. In response, leading manufacturers continue to push design innovation to meet the growing expectations of the automotive sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.64 Billion |

| Forecast Value | $5.44 Billion |

| CAGR | 8.7% |

In 2024, the ball bearings category led the EV bearings market with a dominant 62% share and is expected to expand at a CAGR exceeding 9.8% during the forecast timeline. The segment holds its position due to its ability to support high-volume manufacturing, maintain consistent quality, and meet the demanding operational needs of electric drivetrains. Known for offering minimal friction and maximum reliability, ball bearings are widely integrated into various EV components, including electric motors, transmissions, and wheel hubs. As original equipment manufacturers (OEMs) accelerate the rollout of next-gen vehicle systems-spanning electrification, ADAS, and infotainment technologies-automakers increasingly seek advanced engineering services and components tailored to their unique performance and durability needs.

Battery electric vehicles (BEVs) accounted for a 60% share in 2024, securing the leading segment share. BEVs are fundamentally reshaping the electric vehicle bearings landscape by requiring high-precision components that support enhanced energy efficiency, high-speed operation, and noise minimization. The nature of BEV systems demands bearings that can handle greater thermal fluctuations and extended operating cycles while maintaining optimal performance. As BEVs continue to gain popularity globally, bearing manufacturers are investing in the development of advanced solutions that meet the evolving technical specifications of high-speed electric motors and ensure long-term product reliability.

Asia Pacific Electric Vehicle Bearings Market held a 66% share and generated USD 939.7 million in 2024. As a global leader in EV production and export, China benefits from strong policy support, an expanding supply chain, and a rapidly growing number of domestic automakers. Local bearing manufacturers are responding to this demand by ramping up R&D and scaling production of high-performance bearing solutions tailored for high-efficiency electric drivetrains. The country's active involvement in advancing bearing technologies underscores its position as a central player in the global EV bearings market.

The key companies driving innovation and competition in the Global Electric Vehicle Bearings Industry include Schaeffler, SKF, JTEKT, NTN, Nachi-Fujikoshi, NSK, and Timken. To strengthen their market foothold, electric vehicle-bearing manufacturers are adopting several focused strategies. These include heavy R&D investment to develop high-speed, low-friction, and thermally stable bearing technologies optimized for electric drivetrains. Companies are also forging long-term partnerships with automakers to co-develop custom solutions, aligning with the shift toward integrated e-mobility platforms. Expanding manufacturing footprints in key EV markets, particularly across Asia and North America, is another key approach. In addition, firms are enhancing product portfolios by offering compact, lightweight, and durable designs that meet evolving drivetrain architectures while improving energy efficiency and extending service intervals.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global adoption of electric vehicles supported by government incentives

- 3.2.1.2 Advancements in lightweight and smart bearing technologies improve efficiency and durability

- 3.2.1.3 Expansion of EV manufacturing in emerging markets

- 3.2.1.4 Integration of predictive maintenance through sensor-enabled bearings.

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial costs

- 3.2.2.2 Complex installation and maintenance

- 3.2.3 Market opportunities

- 3.2.3.1 Surging global EV production

- 3.2.3.2 R&D and co-development with OEMs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By component

- 3.10 Production statistics

- 3.10.1 Production hubs

- 3.10.2 Consumption hubs

- 3.10.3 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Ball bearings

- 5.3 Roller bearings

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Battery electric vehicles (BEVs)

- 6.3 Plug-in hybrid electric vehicles (PHEVs)

- 6.4 Hybrid electric vehicles (HEVs)

- 6.5 Fuel cell electric vehicles (FCEVs)

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Steel bearings

- 7.3 Ceramic bearings

- 7.4 Polymer bearings

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Bearing Size, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Small bearings

- 9.3 Medium bearings

- 9.4 Large bearings

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ILJIN

- 11.2 BRK

- 11.3 C&U Group

- 11.4 Fersa

- 11.5 IKO Nippon Thompson

- 11.6 JTEKT

- 11.7 Luoyang LYC Bearing

- 11.8 MinebeaMitsumi

- 11.9 Nachi-Fujikoshi

- 11.10 NBC

- 11.11 NMB Technologies

- 11.12 NSK

- 11.13 NSK-Warner

- 11.14 NTN

- 11.15 RBC Bearings

- 11.16 Schaeffler

- 11.17 SKF

- 11.18 The Timken

- 11.19 THK

- 11.20 ZWZ