自動車用ブーツリリースケーブルの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Automotive Boot Release Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1740847

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

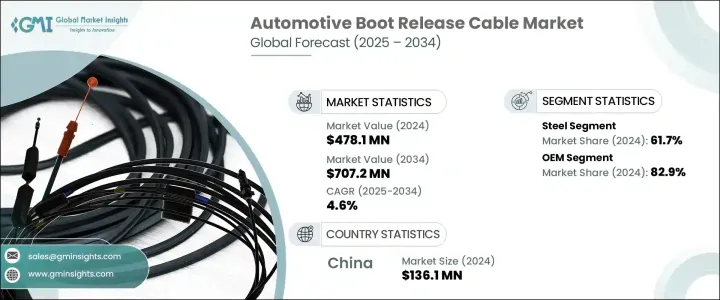

自動車用ブーツリリースケーブルの世界市場は、2024年には4億7,810万米ドルとなり、2034年にはCAGR 4.6%で成長して7億720万米ドルに達すると予測されています。

自動車の設計が進化し、消費者が自動車とのよりシームレスなインタラクションを求めるようになるにつれ、トランクアクセスシステムは著しい変貌を遂げています。かつては単純な機械部品であったブーツリリースケーブルは、現在では幅広いカテゴリーの車両で、よりスマートで安全、かつ効率的なトランクアクセスを可能にする重要な役割を果たしています。自動車メーカーがスマートモビリティと電気自動車技術を採用し続ける中、インテリジェント・トランク・システムの統合は、車両設計における重要な特徴となりつつあります。消費者は利便性とスピードを求め、自動車メーカーは機械的信頼性と最先端のエレクトロニクスを融合させた高性能ケーブルシステムを導入することで対応しています。

コネクテッドでテクノロジーに精通した自動車への嗜好の高まりは、自動車メーカーがトランク開口部のようなアクセス機能を設計する方法を形成しています。ジェスチャーベースのトリガーからモバイルアプリベースの機能まで、今日の消費者は手動レバー以上のものを求めています。この需要は、セキュリティ、快適性、ユーザーエクスペリエンスを向上させる自動車用ブーツリリースケーブルシステムの技術革新を促進しています。こうした開発は、特に電気自動車やハイブリッド車において顕著であり、効率性、軽量設計、スマートな統合がイノベーションの最前線となっています。自動車メーカーは現在、頻繁な使用や厳しい環境条件下でも高い耐久性と性能をサポートできる技術を活用しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 4億7,810万米ドル |

| 予測金額 | 7億720万米ドル |

| CAGR | 4.6% |

進化する規格に対応するため、メーカー各社は先端材料の使用と、よりスマートなエンジニアリング手法にシフトしています。ブーツリリースケーブルの生産では、軽量、耐腐食性、高張力材料が標準になりつつあります。これらの材料は、製品の寿命を向上させるだけでなく、全体的な重量を減らすことによって車両の効率を向上させます。素材の中ではスチールが依然としてトップの選択肢であり、2024年には市場の約61.7%のシェアを獲得し、2034年までのCAGRは5%で成長すると予測されています。その強度、手頃な価格、耐疲労性により、特にトランクへの頻繁なアクセスが必要な商用車や乗用電気自動車など、機械的なストレスを繰り返し受ける部品に最適です。

流通の面では、2024年にはOEMセグメントが82.9%の市場シェアを占めて世界を席巻し、予測期間中もそのリードを維持すると予想されます。自動車メーカーは現在、先進的なブートリリースシステムを標準部品として扱い、安全性と利便性の両方を高めるために生産時に組み込んでいます。OEMは、よりスマートで安全、かつエンドユーザーにとってより直感的な機能を提供する、車両アクセスの未来に沿った機械と電子のハイブリッドソリューションへの投資を増やしています。このシフトは、最初の接触点からユーザー体験を改善することで競争力を維持することを目指す世界自動車ブランドで特に顕著です。

中国は最も影響力のある地域市場として台頭しており、2024年の世界売上高の57.6%を占め、2034年には1億3,610万米ドルに達すると予測されています。同国の自動車生産台数の多さは、強固な自動車部品エコシステムと相まって、世界市場における戦略的優位性をもたらしています。中国の大手サプライヤーは、国際規格と需要を満たすため、高精度、耐腐食性、安全性を強化したケーブルシステムの製造に注力しています。研究開発への継続的な投資とスマートな製造手法により、中国は先進的な自動車用ケーブル技術の世界のハブとしての地位をさらに強化しています。

THB Group、Universal Cable、Leoni AG、Nexans Auto Electric、Birla Cable、Kei Industry、TE Connectivity、Polycab、住友電気工業、Sterlite Technologiesなどの大手企業は、この競争の激しい分野で優位に立つため、軽量で多機能なブートリリースケーブルシステムの設計に注力しています。これらの企業は、戦略的提携を通じて世界のプレゼンスを拡大し、自動化と次世代材料によって製造能力を向上させています。性能、耐久性、およびスマート車両プラットフォームとの互換性に重点を置くことで、自動車業界の進化するニーズに対応しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 製造業者

- 原材料サプライヤー

- 自動車OEM

- 流通チャネル

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- 価格分析

- 推進

- 地域

- 影響要因

- 促進要因

- 車両セキュリティおよびアクセスシステムの重要性の高まり

- 設置が簡単でメンテナンスも簡単

- モジュラーコンポーネントのOEM優先

- 世界の自動車生産の伸び

- 業界の潜在的リスク&課題

- 電子化・スマート化トランクシステムへの移行

- 交換頻度が低い

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:材料別、2021-2034

- 主要動向

- 鋼鉄

- アルミニウム

- プラスチック

- その他

第6章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 軽作業

- 中型

- ヘビーデューティー

第7章 市場推計・予測:推進力別、2021-2034

- 主要動向

- ガソリン

- ディーゼル

- 電気

- PHEV

- ハイブリッド車

- 燃料電池自動車

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Auto7

- Birla Cable

- Chuhatsu

- CMA

- Dorman Products

- Dura Automotive Systems

- GEMO

- HI-LEX

- Infac Corporation

- Kei Industries

- Kongsberg Automotive

- L&P Automotive Group

- Leoni AG

- Nexans Auto Electric

- Polycab

- Sterlite Technology

- Sumitomo Electric Industries

- TE connectivity

- THB Group

- Universal Cable

目次

The Global Automotive Boot Release Cable Market was valued at USD 478.1 million in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 707.2 million by 2034, fueled by rising global vehicle production and the growing demand for advanced vehicle access solutions. As vehicle designs evolve and consumers demand more seamless interactions with their automobiles, trunk access systems have seen a notable transformation. Boot release cables, once simple mechanical components, are now playing a vital role in enabling smarter, more secure, and more efficient trunk access across a wide range of vehicle categories. As automakers continue to embrace smart mobility and electric vehicle technologies, the integration of intelligent trunk systems is becoming a critical feature in vehicle design. Consumers expect convenience and speed, and vehicle manufacturers are responding by deploying high-performance cable systems that blend mechanical reliability with cutting-edge electronics.

The increasing preference for connected, tech-savvy vehicles is shaping how automakers design access features like trunk openings. From gesture-based triggers to mobile app-based functionalities, today's consumers want more than manual levers-they want systems that work in harmony with their digital lifestyles. This demand is driving innovation in automotive boot release cable systems that offer enhanced security, comfort, and user experience. These developments are especially visible in electric and hybrid vehicles, where efficiency, lightweight design, and smart integration are at the forefront of innovation. Automakers are now leveraging technologies that can support high durability and performance even under frequent usage and challenging environmental conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $478.1 Million |

| Forecast Value | $707.2 Million |

| CAGR | 4.6% |

To meet the evolving standards, manufacturers are shifting toward the use of advanced materials and smarter engineering practices. Lightweight, corrosion-resistant, and high-tensile materials are becoming standard in boot release cable production. These materials not only improve product longevity but also enhance vehicle efficiency by reducing overall weight. Steel remains the top choice among materials, capturing nearly 61.7% share of the market in 2024 and projected to grow at a CAGR of 5% through 2034. Its strength, affordability, and resistance to fatigue make it ideal for parts subject to repetitive mechanical stress, especially in commercial and passenger electric vehicles that require frequent trunk access.

In terms of distribution, the OEM segment dominated the global landscape in 2024, accounting for an 82.9% market share, and is expected to maintain its lead through the forecast period. Vehicle manufacturers now treat advanced boot release systems as standard components, integrating them during production to enhance both security and convenience. OEMs are increasingly investing in hybrid mechanical-electronic solutions that align with the future of vehicle access-offering smarter, safer, and more intuitive features for the end user. This shift is particularly prominent among global automotive brands that aim to stay competitive by improving user experience from the first point of interaction.

China is emerging as the most influential regional market, representing 57.6% of global revenue in 2024, with projections hitting USD 136.1 million by 2034. The country's high volume of vehicle production, combined with its robust automotive components ecosystem, gives it a strategic edge in the global market. Leading suppliers in China are focusing on manufacturing high-precision, corrosion-resistant, and safety-enhanced cable systems to meet international standards and demand. Continuous investments in R&D and smart manufacturing practices further strengthen China's position as a global hub for advanced automotive cable technologies.

To stay ahead in this competitive space, major players like THB Group, Universal Cable, Leoni AG, Nexans Auto Electric, Birla Cable, Kei Industry, TE Connectivity, Polycab, Sumitomo Electric Industries, and Sterlite Technologies are focusing on designing lightweight, multi-functional boot release cable systems. These companies are expanding their global presence through strategic alliances and improving their manufacturing capabilities with automation and next-gen materials. Their collective focus on performance, durability, and compatibility with smart vehicle platforms ensures they remain aligned with the evolving needs of the automotive industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Manufacturers

- 3.2.2 Raw material suppliers

- 3.2.3 Automotive OEM

- 3.2.4 Distribution channel

- 3.2.5 End-use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing analysis

- 3.9.1 Propulsion

- 3.9.2 Region

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 Growing emphasis on vehicle security & access systems

- 3.10.1.2 Easy installation and low maintenance

- 3.10.1.3 OEM preference for modular components

- 3.10.1.4 Global vehicle production growth

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Shift towards electronic & smart trunk systems

- 3.10.2.2 Low replacement frequency

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Steel

- 5.3 Aluminium

- 5.4 Plastic

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light duty

- 6.3.2 Medium duty

- 6.3.3 Heavy duty

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

- 7.4 Electric

- 7.5 PHEV

- 7.6 HEV

- 7.7 FCEV

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Auto7

- 10.2 Birla Cable

- 10.3 Chuhatsu

- 10.4 CMA

- 10.5 Dorman Products

- 10.6 Dura Automotive Systems

- 10.7 GEMO

- 10.8 HI-LEX

- 10.9 Infac Corporation

- 10.10 Kei Industries

- 10.11 Kongsberg Automotive

- 10.12 L&P Automotive Group

- 10.13 Leoni AG

- 10.14 Nexans Auto Electric

- 10.15 Polycab

- 10.16 Sterlite Technology

- 10.17 Sumitomo Electric Industries

- 10.18 TE connectivity

- 10.19 THB Group

- 10.20 Universal Cable

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日