|

市場調査レポート

商品コード

1766180

自動車用量子ドット(QD)バックライトユニットの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年Automotive Quantum Dot Backlight Units Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 自動車用量子ドット(QD)バックライトユニットの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年 |

|

出版日: 2025年06月13日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

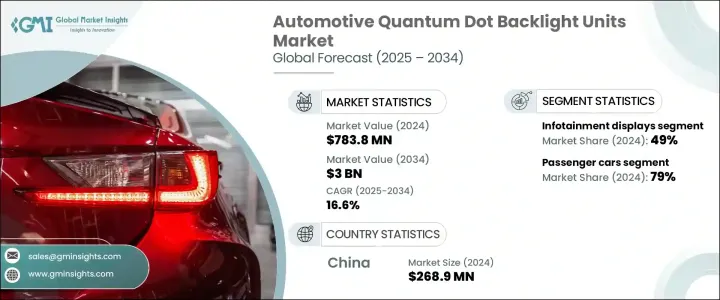

自動車用量子ドット(QD)バックライトユニットの世界市場規模は、2024年に7億8,380万米ドルとなり、2034年には30億米ドルに達し、CAGRで16.6%の成長が予測されています。

この成長の原動力は、没入型デジタルディスプレイに対する消費者の期待の高まりと、自動車におけるインフォテインメントとスマートコックピットシステムの採用の加速です。自動車の内装がデジタルコマンドセンターへと進化するにつれて、優れた色忠実度、高いコントラスト比、高輝度を実現するディスプレイへのニーズが急速に高まっています。量子ドット(QD)バックライトユニットは、こうした高度な視覚機能を実現するための中核部品として台頭してきています。車載コネクティビティ、リアルタイムの走行データ、マルチメディア機能に対する需要が高まる中、QDで強化されたスクリーンは、今日のコネクテッドカーに求められる性能、効率、耐久性を提供します。

自動車メーカーは車室設計を見直し、インフォテインメント、クラスター、ヘッドアップディスプレイ(HUD)を包含する統一ディスプレイプラットフォームへと移行しています。このシフトは、一貫したユーザーインターフェースと合理化された製造をサポートします。電気自動車やハイブリッドモデルからハイエンドの自律走行プラットフォームに至るまで、自動車セグメント全体でモジュール式ディスプレイシステムが普及するにつれて、QDバックライトユニットが標準的な機能になりつつあります。QDバックライトユニットの適応性、色精度、省エネルギーは、次世代の車載デジタル体験におけるQDバックライトユニットの地位を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7億8,380万米ドル |

| 予測金額 | 30億米ドル |

| CAGR | 16.6% |

2024年までに、乗用車セグメントは79%のシェアを占め、2025年から2034年までのCAGRは18%と予測されます。このセグメントでは、QDバックライトユニットが、より豊かな色再現性、より高い輝度、エネルギー消費の改善を実現することで、ディスプレイ性能を変革しています。こうした強化により、QDバックライトユニットは、可変照明条件下で優れた性能を発揮する必要があるインフォテインメント、ヘッドアップディスプレイ、デジタルドライバーダッシュボードに特に適しています。量子ドット強化フィルム(QDEF)によるハイダイナミックレンジ(HDR)ビジュアルは、コネクテッドビークルシステムの安全性と機能性をサポートしながら、没入感をもたらします。LCDベースや曲面ディスプレイ形式へのシームレスな統合により、最新のコックピットレイアウト、特に中級から高級のEVモデルに最適です。QDディスプレイはまた、長期的な車載展開に不可欠な車載グレードの耐久性基準も満たしています。

インフォテインメントディスプレイセグメントは、2024年に49%のシェアを占め、2034年まで15%のCAGRで成長すると予想されています。応答性が高く、鮮やかで、高精細な車内デジタル体験への需要が、車両インフォテインメントシステムへのQD統合を後押ししています。QDバックライトユニットは、マルチメディアの表示、ナビゲーションの鮮明さ、ユーザーインターフェースの応答性を高めます。QDOGやQDEFなどの技術は、中央制御ディスプレイに必要な広色域、高速リフレッシュレート、高輝度レベルを実現します。明るい周囲環境でも画質を維持できるこれらの技術は、ドライバーと同乗者の双方向体験を向上させます。ユーザー体験が競争上の差別化要因になりつつある現在、これらのディスプレイは、従来型車両と電気自動車の両方のセンタースタックシステムに不可欠なものとなっています。

中国の自動車用量子ドット(QD)バックライトユニット市場は、2024年に63%のシェアを占め、2億6,890万米ドルを創出しました。インテリジェントコックピット技術の拡大に伴い、中国の自動車市場はデジタルクラスター、ADASビジュアライゼーション、車内エンターテインメント向けのQD強化システムへと急速にシフトしています。技術開発、製造の現地化、スマートモビリティを支援する公共政策が、QD採用の勢いをさらに強めています。ハイエンドデジタルコックピットソリューションの推進は、QDディスプレイの統合を促進しており、特に、プレミアムディスプレイ技術を標準機能として採用する傾向が強まっている成長中の電気自動車やハイブリッド車セグメントで顕著です。

世界の自動車用量子ドット(QD)バックライトユニット市場の主要企業には、Samsung Display、BOE Technology Group、シャープ、Kyulux、AU Optronics Corp.(AUO)、Nanosys、CSOT(China Star Optoelectronics Technology)、ソニー、Innolux、LG Displayなどがあります。市場での存在感を高めるため、自動車用量子ドット(QD)バックライトユニットの各社は、製品の革新、戦略的提携、生産能力の拡大に注力しています。各社は、QD技術の効率と耐久性を高めると同時に生産コストを削減するため、研究開発に多額の投資を行っています。自動車OEMやTier-1サプライヤーとの提携により、先進QDシステムの新車プラットフォームへの早期統合が可能になっています。また、サプライチェーンの安定性と性能の一貫性を確保するため、複数の企業が垂直統合生産モデルに取り組んでいます。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 高解像度ディスプレイの需要増加

- インフォテインメントシステムの統合の進展

- ADAS(先進運転支援システム)(ADAS)の導入拡大

- 量子ドット材料の技術的進歩

- 業界の潜在的リスク&課題

- 量子ドットディスプレイの高コスト

- カドミウムベースのQDの毒性に関する懸念

- 市場機会

- 自律走行車および半自律走行車への統合

- アフターマーケットのディスプレイアップグレードの増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- コスト内訳分析

- ソフトウェア開発およびライセンシング費用

- 導入と統合のコスト

- 保守・サポート費用

- サイバーセキュリティとコンプライアンスのコスト

- トレーニングと変更管理コスト

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

- 消費者行動と採用動向

- ユーザーエクスペリエンスとインターフェースの動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推定・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- ハッチバック

- SUV

- 商用車

- 小型

- 中型

- 大型

第6章 市場推定・予測:アプリケーション別、2021年~2034年

- 主要動向

- インフォテインメントディスプレイ

- 計器クラスター

- ヘッドアップディスプレイ(HUD)

- 後部座席エンターテインメントシステム

- 先進運転支援システム(ADAS)ディスプレイ

第7章 市場推定・予測:技術別、2021年~2034年

- 主要動向

- 量子ドット増強フィルム(QDEF)バックライト

- 量子ドットオンガラス(QDOG)

- 量子ドットオンLED(QD-LED)

- 量子ドットカラーフィルター(QDCF)

第8章 市場推定・予測:流通チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第9章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AU Optronics Corp.(AUO)

- BOE Technology Group

- CSOT(China Star Optoelectronics Technology)

- Helio Display Materials

- Innolux Corporation

- Kyulux

- LG Display

- Luminit LLC

- Nanoco Group

- Nanosys

- Noctiluca

- OSRAM Continental

- PixelDisplay

- QD Laser

- Quantum Solutions

- Samsung Display

- Sharp Corporation

- Sony Corporation

- Toray Industries

- Visionox

The Global Automotive Quantum Dot Backlight Units Market was valued at USD 783.8 million in 2024 and is estimated to grow at a CAGR of 16.6% to reach USD 3 billion by 2034. This growth is driven by rising consumer expectations for immersive digital displays and the accelerating adoption of infotainment and smart cockpit systems in vehicles. As automotive interiors evolve into digital command centers, the need for displays that deliver superior color fidelity, higher contrast ratios, and enhanced brightness is growing rapidly. Quantum dot (QD) backlight units are emerging as core components for delivering these advanced visual capabilities. With demand increasing for in-vehicle connectivity, real-time driving data, and multimedia functions, QD-enhanced screens offer the performance, efficiency, and durability required by today's connected vehicles.

Automakers are rethinking their cabin designs, moving toward unified display platforms that encompass infotainment, clusters, and head-up displays (HUDs). This shift supports a consistent user interface and streamlined manufacturing. As modular display systems gain traction across vehicle segments-from electric and hybrid models to high-end autonomous platforms-QD backlight units are becoming a standard feature. Their adaptability, color precision, and energy savings are reinforcing their position in the next generation of digital automotive experiences.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $783.8 Million |

| Forecast Value | $3 Billion |

| CAGR | 16.6% |

By 2024, the passenger vehicles segment held a 79% share and is predicted to grow at a CAGR of 18% from 2025 to 2034. Within this segment, QD backlight units are transforming display performance by delivering richer color reproduction, elevated brightness, and improved energy use. These enhancements make them especially suitable for infotainment, head-up displays, and digital driver dashboards that need to perform well under variable lighting conditions. High-dynamic-range (HDR) visuals powered by Quantum Dot Enhancement Films (QDEF) bring an immersive experience while supporting safety and functionality in connected vehicle systems. Their seamless integration into LCD-based and curved display formats makes them ideal for modern cockpit layouts, particularly within mid-range to luxury EV models. QD displays also meet automotive-grade durability standards, which are essential for long-term in-vehicle deployment.

The infotainment displays segment held a 49% share in 2024 and is expected to grow at 15% CAGR through 2034. The demand for responsive, vibrant, and highly detailed in-cabin digital experiences is pushing QD integration within vehicle infotainment systems. QD backlight units enhance multimedia viewing, navigation clarity, and user interface responsiveness. Technologies such as QD-on-Glass and QDEF deliver wide color gamuts, faster refresh rates, and high brightness levels necessary for central control displays. Their ability to retain image quality in bright ambient environments enhances the interactive experience for both drivers and passengers. With user experience becoming a competitive differentiator, these displays are now integral to center-stack systems across both conventional and electric vehicles.

China Automotive Quantum Dot Backlight Units Market held a 63% share and generated USD 268.9 million in 2024, propelled by its large-scale vehicle production and strong demand for high-tech automotive displays. With the expansion of intelligent cockpit technologies, China's automotive market is rapidly shifting toward QD-enhanced systems for digital clusters, ADAS visualization, and in-car entertainment. Public policies supporting tech development, localized manufacturing, and smart mobility have further strengthened the momentum behind QD adoption. The push for high-end digital cockpit solutions is driving the integration of QD displays, especially in the growing electric and hybrid vehicle segments, which are increasingly adopting premium display technologies as standard features.

Key players actively shaping the Global Automotive Quantum Dot Backlight Units Market include Samsung Display, BOE Technology Group, Sharp, Kyulux, AU Optronics Corp. (AUO), Nanosys, CSOT (China Star Optoelectronics Technology), Sony, Innolux, and LG Display. To strengthen their market presence, companies in the automotive quantum dot backlight unit space are focusing on product innovation, strategic alliances, and capacity expansion. Firms are investing heavily in R&D to enhance the efficiency and durability of QD technologies while reducing production costs. Partnerships with automotive OEMs and Tier-1 suppliers are allowing for early integration of advanced QD systems into new vehicle platforms. Several players are also working on vertically integrated production models to ensure supply chain stability and performance consistency.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Application

- 2.2.4 Technology

- 2.2.5 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for high-resolution displays

- 3.2.1.2 Rising integration of infotainment systems

- 3.2.1.3 Growing adoption of Advanced Driver Assistance Systems (ADAS)

- 3.2.1.4 Technological advancements in quantum dot materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of quantum dot displays

- 3.2.2.2 Toxicity concerns with cadmium-based QDs

- 3.2.3 Market opportunities

- 3.2.3.1 Integration in autonomous and semi-autonomous vehicles

- 3.2.3.2 Growing aftermarket display upgrades

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

- 3.13 Consumer behaviour & adoption trends

- 3.14 User experience & interface trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Infotainment displays

- 6.3 Instrument clusters

- 6.4 Head-Up Displays (HUDs)

- 6.5 Rear-seat entertainment systems

- 6.6 Advanced Driver Assistance System (ADAS) displays

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Quantum Dot Enhancement Film (QDEF) backlights

- 7.3 Quantum Dot on Glass (QDOG)

- 7.4 Quantum Dot on LED (QD-LED)

- 7.5 Quantum Dot Color Filters (QDCF)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AU Optronics Corp. (AUO)

- 10.2 BOE Technology Group

- 10.3 CSOT (China Star Optoelectronics Technology)

- 10.4 Helio Display Materials

- 10.5 Innolux Corporation

- 10.6 Kyulux

- 10.7 LG Display

- 10.8 Luminit LLC

- 10.9 Nanoco Group

- 10.10 Nanosys

- 10.11 Noctiluca

- 10.12 OSRAM Continental

- 10.13 PixelDisplay

- 10.14 QD Laser

- 10.15 Quantum Solutions

- 10.16 Samsung Display

- 10.17 Sharp Corporation

- 10.18 Sony Corporation

- 10.19 Toray Industries

- 10.20 Visionox