硫酸アンモニウムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Ammonium Sulphate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766178

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

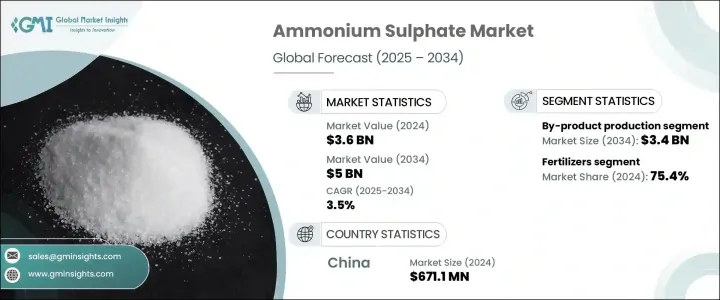

硫酸アンモニウムの世界市場規模は、2024年に36億米ドルとなり、CAGR 3.5%で成長し、2034年には50億米ドルに達すると予測されています。

この成長の原動力は、世界の食糧生産をサポートする必要性の高まり、農業経営の拡大、人口増加に対する食糧サプライチェーンの確保に対する需要の高まりです。硫酸アンモニウムは、主に窒素ベースの肥料としての重要な役割と、さまざまな産業セグメントでの用途の拡大により、引き続き強い牽引力を持っています。アルカリ土壌での高い溶解性と効率性により、特に稲作、トウモロコシ、小麦の栽培において、作物の収量を向上させるための好ましい選択肢となっています。サステイナブル農業を推進する政府のイニシアティブに支えられ、開発途上地域でこの化合物の重要性が高まっています。

世界の硫酸アンモニウム需要の75%以上は肥料使用によるものです。アジア太平洋の、特に中国やインドなどの国々では、人口が増加し、耕作地の拡大が重視されるようになったため、肥料の消費量が増加しています。また、水処理、医薬品製造、食品加工などの産業セグメントでも、この化合物の役割が高まっています。排煙脱硫装置への応用は、特に大気質基準が厳しい地域で重要性を増しています。排ガス規制技術を通じてよりクリーンな海運を目指す動きも、世界の規制強化が続く中、硫酸アンモニウムの使用量を押し上げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 36億米ドル |

| 予測金額 | 50億米ドル |

| CAGR | 3.5% |

2024年、製造方法は24億米ドルの貢献をしており、CAGR 3.5%を維持しながら2034年には34億米ドルに達すると予測されています。製品別生産が68.4%のシェアを占めるのは、その費用対効果と廃棄物ストリームの環境的に有利な利用によるものです。この方法は、コークス炉ガスやカプロラクタムのような材料の処理中や、石炭排ガスのスクラビング中に硫酸アンモニウムを回収します。特に、硫酸アンモニウムのような使用可能な形態への硫黄回収を促進する産業排出指令のような施策下では、このような方法によって生産コストを下げると同時に、環境への懸念にも対応することができます。

2024年の市場は、肥料セグメントが75.4%のシェアを占めました。このセグメントは、硫酸アンモニウムが効果的で低コストの窒素肥料として機能し、特にアルカリ性土壌での栄養分の取り込みを改善するのに役立つため、引き続き繁栄しています。自給自足レベルでも商業レベルでも、幅広い農業活動を支えています。トウモロコシ、コメ、その他の穀物などの作物は、その使いやすさと他の肥料との相性の良さから恩恵を受けています。アジア太平洋のとラテンアメリカ開発途上国は、政府補助金の増加と、効率を高め無駄を最小限に抑える精密農業のような近代的農業戦略への大きなシフトのおかげで、その採用をリードしています。

中国の硫酸アンモニウム2024年の市場規模は6億7,110万米ドルで、CAGR 3.6%で成長し、2034年には9億5,390万米ドルに達すると予測されています。この市場は、同国の旺盛な農業生産高に支えられて急速に拡大しています。世界の耕地面積の10%以下であるにもかかわらず、中国は世界の穀物の約25%を生産しており、特に稲作では硫酸アンモニウムのような土壌改良剤への依存度が高いです。同国は工業生産も拡大しており、圧縮硫酸アンモニウムの大量生産を目指した大規模な共同研究が、このセクタの勢いを加速させています。

世界の硫安産業の主要企業には、BASF SE、UBE Corporation、OCI Nitrogen、Evonik Industries AG、Lanxess AGなどがあります。硫酸アンモニウム市場の主要企業が採用する主要戦略は、戦略的提携による生産能力の拡大、コスト効率の高い生産技術の研究開発強化、付加価値の高い産業用途の開拓です。特にカプロラクタムやコークス炉プロセスからの製品別回収など、よりクリーンな生産ルートに投資しています。合弁事業や施設の拡大を通じて、アジア太平洋のような高成長地域での事業拠点を拡大することも、引き続き主要な優先事項となっています。さらに、主要企業は、特に肥料需要が急増している新興国において、より良いサービスの提供と地域密着型のサポートを確保するため、サプライチェーンと流通網を強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- 産業の潜在的リスク・課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品形態別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計

(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブル実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測:製造方法別、2021~2034年

- 主要動向

- 合成生産

- 製品別生産

- カプロラクタム生産

- コークス炉の操業

- メチルメタクリレートの生産

- その他の製品別源

第6章 市場推定・予測:製品形態別、2021~2034年

- 主要動向

- 固体

- 粒状

- 結晶質

- 液体

第7章 市場推定・予測:純度別、2021~2034年

- 主要動向

- 標準グレード(99%以下)

- 高純度グレード(99%以上)

第8章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 肥料

- ストレート肥料

- 複合肥料

- 特殊肥料

- 産業用途

- 繊維産業

- 水処理

- 食品添加物

- 難燃剤

- 化学製造

- その他

- 医薬品

- その他

第9章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

第10章 企業プロファイル

- BASF SE

- AdvanSix Inc.

- CF Industries Holdings, Inc.

- Domo Chemicals GmbH

- Domo Engineering Plastics US

- EuroChem Group AG

- Evonik Industries AG

- Grupa Azoty S.A.

- Helm AG

- Honeywell International Inc.

- JSC Kuibyshevazot

- Lanxess AG

- Novus International, Inc.

- Nutrien Ltd.

- OCI N.V.

- Ostchem Holding

- Sinopec

- Sumitomo Chemical Co., Ltd.

- Ube Industries, Ltd.

- Yara International ASA

目次

The Global Ammonium Sulphate Market was valued at USD 3.6 billion in 2024 and is estimated to grow at a CAGR of 3.5% to reach USD 5 billion by 2034. This growth is driven by the increasing need to support global food production, expanding agricultural operations, and the rising demand to secure food supply chains for a growing population. Ammonium sulphate continues to see strong traction primarily due to its critical role as a nitrogen-based fertilizer and its expanding applications across various industrial sectors. Its high solubility and efficiency in alkaline soils make it a preferred choice for enhancing crop yields, especially in rice, maize, and wheat farming. The compound's relevance is rising in developing regions, supported by governmental initiatives promoting sustainable agricultural practices.

More than 75% of global ammonium sulphate demand is attributed to fertilizer usage. In regions like Asia Pacific, especially countries such as China and India, the growing population and increased focus on arable land expansion have resulted in higher fertilizer consumption. The compound also plays a growing role in industrial fields like water treatment, pharmaceutical manufacturing, and food processing. Its application in flue gas desulfurization systems has gained significance, particularly in areas that enforce stringent air quality standards. The push toward cleaner shipping through emission control technologies has also boosted ammonium sulphate usage, as global regulations continue to tighten.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $5 Billion |

| CAGR | 3.5% |

In 2024, the by-product production method contributed USD 2.4 billion and is forecasted to reach USD 3.4 billion by 2034, maintaining a 3.5% CAGR. By-product production accounts for 68.4% share due to its cost-effectiveness and environmentally favorable use of waste streams. This method recovers ammonium sulphate during the processing of materials like coke oven gas and caprolactam, as well as during coal flue gas scrubbing. These routes lower production costs while addressing environmental concerns, especially under policies like the Industrial Emissions Directive, which promotes sulphur recovery into usable forms such as ammonium sulphate.

The fertilizer segment dominated the market in 2024, holding a 75.4% share. This segment continues to thrive as ammonium sulphate serves as an effective and low-cost nitrogen fertilizer, especially valuable in improving nutrient uptake in alkaline soils. It supports a wide range of agricultural activities at both subsistence and commercial levels. Crops like maize, rice, and other cereals benefit from its ease of use and compatibility with other fertilizers. Developing nations in Asia Pacific and Latin America are leading in its adoption, thanks to increased government subsidies and a greater shift toward modern agricultural strategies like precision farming, which enhances efficiency and minimizes waste.

China Ammonium Sulphate Market generated USD 671.1 million in 2024 and is projected to grow at a 3.6% CAGR, reaching USD 953.9 million by 2034. This market is expanding rapidly, underpinned by the country's robust agricultural output. Despite having under 10% of the world's arable land, China produces around 25% of global grain, reinforcing its heavy reliance on soil enhancers like ammonium sulphate, particularly for rice cultivation. The country also benefits from growing industrial production, and large-scale collaborations aimed at manufacturing significant volumes of compacted ammonium sulphate are boosting the sector's momentum.

Major players in the global ammonium sulfate industry include BASF SE, UBE Corporation, OCI Nitrogen, Evonik Industries AG, and Lanxess AG. Key strategies adopted by leading companies in the ammonium sulphate market focus on expanding capacity through strategic collaborations, boosting R&D for cost-efficient production technologies, and tapping into value-added industrial applications. Companies are investing in cleaner production routes, especially by-product recovery from caprolactam and coke oven processes, which allow cost savings and align with regulatory pressures for environmental sustainability. Expanding footprint in high-growth regions like Asia Pacific through joint ventures and facility expansions also remains a major priority. Additionally, key firms are strengthening their supply chains and distribution networks to ensure better service delivery and localized support, especially in emerging economies where fertilizer demand is booming.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Production Method

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product form

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics

( Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Production Method, 2021 – 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Synthetic production

- 5.3 By-product production

- 5.3.1 Caprolactam production

- 5.3.2 Coke oven operations

- 5.3.3 Methyl methacrylate production

- 5.3.4 Other by-product sources

Chapter 6 Market Estimates and Forecast, By Product Form, 2021 – 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Solid

- 6.2.1 Granular

- 6.2.2 Crystalline

- 6.3 Liquid

Chapter 7 Market Estimates and Forecast, By Purity Grade, 2021 – 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Standard grade (≤99%)

- 7.3 High purity grade (>99%)

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Fertilizers

- 8.2.1 Straight fertilizers

- 8.2.2 Compound fertilizers

- 8.2.3 Specialty fertilizers

- 8.3 Industrial applications

- 8.3.1 Textile industry

- 8.3.2 Water treatment

- 8.3.3 Food additives

- 8.3.4 Flame retardants

- 8.3.5 Chemical manufacturing

- 8.3.6 Others

- 8.4 Pharmaceutical

- 8.5 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 AdvanSix Inc.

- 10.3 CF Industries Holdings, Inc.

- 10.4 Domo Chemicals GmbH

- 10.5 Domo Engineering Plastics US

- 10.6 EuroChem Group AG

- 10.7 Evonik Industries AG

- 10.8 Grupa Azoty S.A.

- 10.9 Helm AG

- 10.10 Honeywell International Inc.

- 10.11 JSC Kuibyshevazot

- 10.12 Lanxess AG

- 10.13 Novus International, Inc.

- 10.14 Nutrien Ltd.

- 10.15 OCI N.V.

- 10.16 Ostchem Holding

- 10.17 Sinopec

- 10.18 Sumitomo Chemical Co., Ltd.

- 10.19 Ube Industries, Ltd.

- 10.20 Yara International ASA

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日