コンデンスミルク・エバミルクの市場機会、成長促進要因、産業動向分析、予測、2025年~2034年

Condensed Or Evaporated Milk Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766171

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

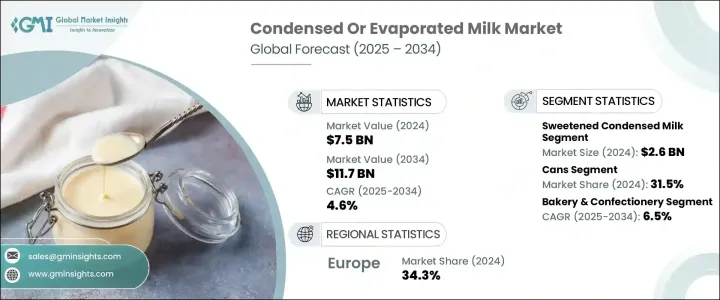

世界のコンデンスミルク・エバミルク市場は、2024年には75億米ドルと評価され、2034年には117億米ドルに達し、CAGRで4.6%の成長が予測されています。

特に冷蔵施設へのアクセスが限られている地域で、保存可能な乳製品の人気が高まっていることが、この成長の原動力となっています。消費者は、料理やお菓子作りに適し、新鮮な牛乳の代用品として長期保存可能な代用乳を求めるようになっています。需要は主に家庭用と、ベーカリー、カフェ、デザート店などの外食産業から生じています。

さらに、特にアジア太平洋とラテンアメリカでは、食の動向の変化により、コンデンスミルクを使ったレシピへの関心が再び高まっています。新しいフレーバー、低糖質オプション、植物性または乳糖不使用の代替品などのイノベーションが、製品の魅力を広げています。包装ソリューションの強化やオンライン小売の拡大がアクセスと利便性を向上させ、新鮮な乳製品や非乳製品との競合の中で市場の着実な拡大を支えています。先進国と新興国の両方で現代的で伝統的な食生活が進化しているため、市場は引き続き堅調です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 75億米ドル |

| 予測金額 | 117億米ドル |

| CAGR | 4.6% |

2024年には、加糖コンデンスミルクがシェア35.2%を占め、26億米ドルとなります。この分野は、消費者の嗜好に合わせた集中的なマーケティング努力と製品革新により引き続き繁栄しています。風味のないコンデンスミルクは調理用として高い人気を維持しているが、チョコレート、キャラメル、バニラなどの風味のあるコンデンスミルクは、特に贅沢なお菓子を求める若い消費者の間で人気を集めています。

缶包装セグメントは2024年に31.5%のシェアを占め、CAGR 4%で成長し、消費者の裾野を広げると予測されます。缶はその耐久性と製品の鮮度を維持する能力により、エバミルクの包装としては依然として支配的な選択肢ですが、重量が重く、製造コストが高いため、成長は急速というよりはむしろ着実です。一方、アセプティック技術を使用したテトラパックのカートンは、軽量でリサイクル可能であり、冷蔵せずに牛乳を保存できるため、環境意識の高い消費者にアピールできるため、人気が高まっています。

欧州のコンデンスミルク・エバミルク市場は、2024年に34.3%の市場シェアでした。地域の消費パターンと料理の伝統が市場力学に大きな影響を与えます。欧州市場は、料理や加工食品におけるエバミルクの広範な使用によって安定した需要を維持しています。北米は成熟した市場であり、主に製パンおよびコンビニエンスフードのセクターによって着実な成長を遂げています。対照的に、アジア太平洋地域は、都市化、食習慣の変化、これらの乳製品を使用する欧米スタイルのデザートや飲料の需要増に後押しされ、急速な拡大を経験しています。

世界のコンデンスミルク・エバミルク業界の主要企業には、Friesland Campina N.V.、Arla Foods、Danone S.A.、Nestle S.A.、The J.M. Smucker Company(Eagle Brand)などがあります。コンデンスミルク・エバミルク市場での地位を強化するため、各社は製品のイノベーションに注力し、多様な消費者の嗜好に対応するためにフレーバーの種類を増やしています。低糖質、植物性、乳糖不使用の選択肢の開発に重点を置くことで、健康や食生活への関心の高まりに対応しています。企業は、環境目標や消費者の嗜好に合わせて、リサイクル可能なカートンや軽量容器など、持続可能な包装ソリューションに投資しています。オンライン販売チャネルを戦略的に拡大することで、冷蔵設備が限られている地域でも製品へのアクセスが向上します。さらに、外食業者や小売業者との提携は、市場拡大の一助となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推定・予測:製品タイプ別、2021年~2034年

- 主要動向

- 加糖コンデンスミルク

- 無糖コンデンスミルク(エバミルク)

- フレーバーコンデンスミルク

- 低脂肪・無脂肪バリエーション

- オーガニックコンデンスミルク・エバミルク

- その他

第6章 市場推定・予測:包装タイプ別、2021年~2034年

- 主要動向

- 缶

- テトラパック

- ボトル

- チューブ

- ポーチ

- その他

第7章 市場推定・予測:流通チャネル別、2021年~2034年

- 主要動向

- スーパーマーケッ・ハイパーマーケット

- コンビニエンスストア

- オンライン小売

- 専門店

- フードサービス業界

- その他

第8章 市場推定・予測:アプリケーション別、2021年~2034年

- 主要動向

- ベーカリー・菓子類

- 飲料

- コーヒー・紅茶

- スムージー・ミルクシェイク

- その他の飲料

- デザート・アイスクリーム

- 幼児用食品

- ソース・スープ

- 直接消費

- その他

第9章 市場推定・予測:最終用途別、2021年~2034年

- 主要動向

- 家庭/小売消費者

- フードサービス業界

- 食品加工業界

- その他

第10章 市場推定・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第11章 企業プロファイル

- Nestle S.A.

- The J.M. Smucker Company(Eagle Brand)

- Arla Foods amba

- FrieslandCampina N.V.

- Goya Foods, Inc.

- Dairy Farmers of America, Inc.

- Borden Dairy Company

- Fonterra Co-operative Group Limited

- Danone S.A.

- Amul(Gujarat Cooperative Milk Marketing Federation Ltd.)

- California Dairies, Inc.

- Almarai Company

- Saputo Inc.

- Alaska Milk Corporation(Royal FrieslandCampina)

目次

The Global Condensed Or Evaporated Milk Market was valued at USD 7.5 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 11.7 billion by 2034. The rising popularity of shelf-stable dairy products, especially in regions with limited refrigeration access, is driving this growth. Consumers increasingly seek long-lasting milk alternatives suitable for cooking and baking, and as substitutes for fresh milk. Demand stems largely from household use and the food service sector, including bakeries, cafes, and dessert outlets.

Additionally, shifting food trends have sparked renewed interest in recipes incorporating condensed milk, especially across Asia-Pacific and Latin America, fueled by the growth of convenience foods and ready-to-eat desserts. Innovations such as new flavors, low-sugar options, and plant-based or lactose-free alternatives are broadening the product's appeal. Enhanced packaging solutions and expanded online retail availability are improving access and convenience, supporting steady market expansion amid competition from fresh and non-dairy milk products. The market remains robust as modern and traditional diets evolve in both developed and emerging regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.5 Billion |

| Forecast Value | $11.7 Billion |

| CAGR | 4.6% |

In 2024, sweetened condensed milk accounted for a 35.2% share, valued at USD 2.6 billion. This segment continues to thrive due to focused marketing efforts and product innovation that align with consumer preferences. While unflavored condensed milk retains significant popularity for cooking applications, flavored variants-such as those with chocolate, caramel, or vanilla-are gaining traction, especially among younger consumers seeking indulgent treats.

The canned packaging segment held a 31.5% share in 2024 and is projected to grow at a 4% CAGR, expanding its consumer reach. Although cans remain the dominant packaging choice for evaporated milk due to their durability and ability to maintain product freshness, their heavier weight and higher production costs mean growth is steady rather than rapid. Meanwhile, Tetra Pak cartons using aseptic technology are becoming more popular because they are lightweight, recyclable, and preserve milk without refrigeration, appealing to environmentally conscious consumers.

Europe Condensed or Evaporated Milk Market held a 34.3% share in 2024. Regional consumption patterns and culinary traditions heavily influence market dynamics. The European market maintains steady demand driven by the widespread use of evaporated milk in cooking and processed foods. North America represents a mature market with steady growth, largely fueled by the baking and convenience food sectors. In contrast, the Asia-Pacific region is experiencing rapid expansion, propelled by urbanization, changing eating habits, and increased demand for Western-style desserts and beverages that use these dairy products.

Key players in the Global Condensed or Evaporated Milk Industry include Friesland Campina N.V., Arla Foods, Danone S.A., Nestle S.A., and The J.M. Smucker Company (Eagle Brand). To strengthen their position in the condensed or evaporated milk market, companies are focusing on product innovation and expanding flavor varieties to meet diverse consumer tastes. Emphasis on developing low-sugar, plant-based, and lactose-free options addresses growing health and dietary concerns. Firms are investing in sustainable packaging solutions, such as recyclable cartons and lightweight containers, to align with environmental goals and consumer preferences. Strategic expansion of online sales channels improves product accessibility in regions with limited refrigeration. Additionally, partnerships with food service providers and retailers help broaden market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (000’ Liters)

- 5.1 Key trends

- 5.2 Sweetened condensed milk

- 5.3 Unsweetened condensed milk (Evaporated milk)

- 5.4 Flavored condensed milk

- 5.5 Low-fat & fat-free variants

- 5.6 Organic condensed & evaporated milk

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Billion) (000’ Liters)

- 6.1 Key trends

- 6.2 Cans

- 6.3 Tetra packs

- 6.4 Bottles

- 6.5 Tubes

- 6.6 Pouches

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (000’ Liters)

- 7.1 Key trends

- 7.2 Supermarkets & Hypermarkets

- 7.3 Convenience stores

- 7.4 Online retail

- 7.5 Specialty stores

- 7.6 Foodservice industry

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (000’ Liters)

- 8.1 Key trends

- 8.2 Bakery & confectionery

- 8.3 Beverages

- 8.3.1 Coffee & tea

- 8.3.2 Smoothies & milkshakes

- 8.3.3 Other beverages

- 8.4 Desserts & ice cream

- 8.5 Infant food

- 8.6 Sauces & soups

- 8.7 Direct consumption

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (000’ Liters)

- 9.1 Key trends

- 9.2 Household/retail consumers

- 9.3 Food service industry

- 9.4 Food processing industry

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (000’ Liters)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Nestle S.A.

- 11.2 The J.M. Smucker Company (Eagle Brand)

- 11.3 Arla Foods amba

- 11.4 FrieslandCampina N.V.

- 11.5 Goya Foods, Inc.

- 11.6 Dairy Farmers of America, Inc.

- 11.7 Borden Dairy Company

- 11.8 Fonterra Co-operative Group Limited

- 11.9 Danone S.A.

- 11.10 Amul (Gujarat Cooperative Milk Marketing Federation Ltd.)

- 11.11 California Dairies, Inc.

- 11.12 Almarai Company

- 11.13 Saputo Inc.

- 11.14 Alaska Milk Corporation (Royal FrieslandCampina)

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日