|

市場調査レポート

商品コード

1755391

船舶用レシプロエンジンの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Marine Reciprocating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 船舶用レシプロエンジンの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月23日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

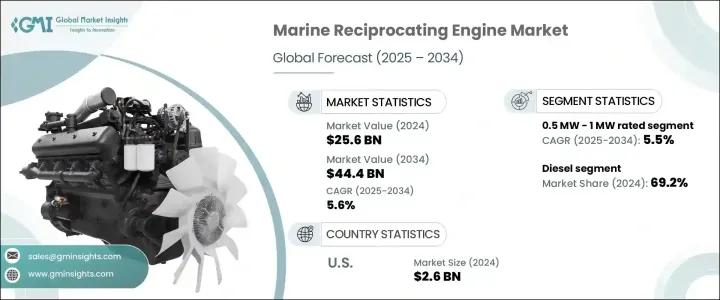

船舶用レシプロエンジンの世界市場規模は、2024年に256億米ドルとなり、CAGR5.6%で成長し、2034年までには444億米ドルに達すると予測されています。

この成長の原動力は、世界の排出規制の厳格化と、コストや入手可能性に応じて燃料の種類をシフトできる燃料フレキシブルシステムに対する需要の高まりです。船舶所有者や運航会社は、環境要件を満たし燃料消費を削減するためにエンジンシステムをアップグレードしており、市場の成長をさらに後押ししています。

加えて、開発途上国の港湾インフラの拡大が海上交通量を増加させており、効率的で環境に適合したパワーソリューションへのニーズが高まっています。また、リアルタイムの監視・診断機能の技術的向上により、オペレーターは主要性能指標を追跡して予期せぬ故障を防ぎ、システムの信頼性と稼働率を高めることができます。メーカー各社は、小型船舶、オフショア支援船、限られたスペースの船舶用途のニーズを満たすため、よりコンパクトなエンジンの設計に注力しており、ニッチ分野での採用が進んでいます。国際海事機関のTier III基準などの規制枠組みは、エンジンの高精度化と最適化を引き続き推進しており、メーカーは進化する海洋エネルギー情勢の中で競争力を維持するために迅速な技術革新を促しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 256億米ドル |

| 予測金額 | 444億米ドル |

| CAGR | 5.6% |

定格出力0.5MWから1MWの船舶用レシプロエンジン分野は、中型船におけるコンパクトで効率的な推進システムに対する需要の高まりに後押しされ、2034年までCAGR5.5%で成長すると予測されます。これらのエンジンは、サイズ、出力、運用コストの理想的なバランスを提供するため、操縦性と燃費が不可欠な様々な用途に好んで選ばれています。沿岸警備船、旅客フェリー、小型貨物船への配備が増加しており、採用が加速しています。さらに、これらのエンジンはメンテナンスが容易で、船内の限られたスペースに組み込むことができるため、性能やコンプライアンスを犠牲にすることなく、船舶のレイアウトを最適化したいと考えているオペレーターにも魅力的です。

ガスエンジン船舶用レシプロエンジン分野は、2034年までCAGR6.5%で成長すると予想されます。この成長は、世界の排出規制の強化や、海運業界全体における持続可能性への関心の高まりと密接に関連しています。規制当局がよりクリーンな海上運航を強制する中、船舶運航者は、温室効果ガスの排出量が大幅に少なく、硫黄含有量も少ないガス燃料エンジンにシフトしています。これらのエンジンは、国際的な規制に対応するだけでなく、特に排ガス規制のある地域では、よりクリーンで経済的な燃料を使用することにより、長期的なコストメリットをもたらします。

米国の船舶用レシプロエンジン市場規模は2024年に26億米ドルでした。この成長は、国際輸送量の着実な増加、オフショア石油・風力エネルギーインフラへの継続的投資、レジャーボート活動の堅調な増加に起因します。同国の整備された港湾システムと支援的な規制環境は、先進的な海洋推進技術の導入をさらに促進します。このような良好なエコシステムは、商業用およびレジャー用の船舶運航会社が、最新の性能と環境基準を満たす、より新しく効率的なエンジンに投資することを後押ししています。

同市場の主要企業には、Caterpillar、Wartsila、Perkins Engines、IHI Corporation、MAN Energy Solutions、Yanmar HOLDINGS、General Electric、Briggs &Stratton、Kawasaki Heavy Industries、Cummins、Yamaha Motor、Scania、AB Volvo Penta、Rehlko、KUBOTA Corporation、MITSUBISHI HEAVY INDUSTRIES、Rolls-Royce、J C Bamford Excavators、American Honda Motor、Guascor Energyなどがあります。各社は市場での地位を向上させるため、研究開発に投資して規制対応に合わせた低排出ガス・低燃費エンジンを開発するなどの戦略を活用しています。その多くは、ハイブリッドやガスエンジン技術に重点を置き、脱炭素化の動向に合わせています。造船会社や船隊運航会社とのパートナーシップは長期供給契約の確保に役立ち、新興沿岸経済圏での地理的拡大は新たな収益源を開きます。先進的なデジタル監視システムを取り入れて、予知保全とリアルタイムの診断を提供します。各ブランドは、アフターセールスサポートを向上させるためにサービスネットワークを拡大し、長期的な顧客エンゲージメントと、性能が重視される用途における信頼性を確保します。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 規制情勢

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:燃料別、2021年~2034年

- 主要動向

- ディーゼル

- ガス

- その他

第6章 市場規模・予測:定格出力別、2021年~2034年

- 主要動向

- 0.5MW~1MW

- 1MW~2MW以上

- 2MW~3.5MW以上

- 3.5MW~5MW以上

- 5MW~7.5MW以上

- 7.5MW以上

第7章 市場規模・予測:シリンダー構成別、2021年~2034年

- 主要動向

- インライン

- V型

- ラジアル

- 対向ピストン

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- スペイン

- オランダ

- デンマーク

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- タイ

- シンガポール

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- カタール

- オマーン

- クウェート

- エジプト

- トルコ

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第9章 企業プロファイル

- AB Volvo Penta

- American Honda Motor

- Briggs &Stratton

- Caterpillar

- Cummins

- General Electric

- Guascor Energy

- IHI Corporation

- J C Bamford Excavators

- Kawasaki Heavy Industries

- KUBOTA Corporation

- MAN Energy Solutions

- MITSUBISHI HEAVY INDUSTRIES

- Perkins Engines

- Rehlko

- Rolls-Royce

- Scania

- Wartsila

- Yamaha Motor

- Yanmar HOLDINGS

The Global Marine Reciprocating Engine Market was valued at USD 25.6 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 44.4 billion by 2034. The growth is driven by the stricter global emission regulations, combined with rising demand for fuel-flexible systems that can shift between fuel types based on cost and availability. Ship owners and operators are upgrading their engine systems to meet environmental requirements and reduce fuel consumption, further fueling market growth.

In addition, expanding port infrastructure across developing nations is boosting marine traffic, intensifying the need for efficient and environmentally compliant power solutions. Technological improvements in real-time monitoring and diagnostic capabilities also allow operators to track key performance indicators prevent unexpected failures and raise system reliability and uptime. Manufacturers are focusing on designing more compact engines to meet the needs of smaller vessels, offshore support crafts, and limited-space marine applications, enhancing adoption across niche sectors. Regulatory frameworks such as the International Maritime Organization's Tier III standards continue to push for higher engine precision and optimization, prompting manufacturers to innovate rapidly to stay competitive in the evolving marine energy landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25.6 Billion |

| Forecast Value | $44.4 Billion |

| CAGR | 5.6% |

The 0.5 MW to 1 MW rated marine reciprocating engine segment is projected to grow at a CAGR of 5.5% through 2034, fueled by rising demand for compact and efficient propulsion systems in medium-duty vessels. These engines offer the ideal balance between size, power, and operational cost, making them a preferred choice for various applications where maneuverability and fuel economy are essential. Increasing deployment in coastal security vessels, passenger ferries, and small cargo ships accelerates their adoption. Additionally, these engines are easier to maintain and integrate into limited space on board, which appeals to operators looking to optimize vessel layout without sacrificing performance or compliance.

The gas-powered marine reciprocating engine segment is expected to grow at a CAGR of 6.5% through 2034. This growth is closely linked to the tightening of global emissions standards and a heightened focus on sustainability across the marine industry. As regulators enforce cleaner maritime operations, vessel operators shift toward gas-fueled engines due to their significantly lower greenhouse gas emissions and reduced sulfur content. These engines not only support compliance with international mandates but also offer long-term cost benefits by using cleaner, often more economical fuel sources, especially in emission-controlled areas.

United States Marine Reciprocating Engine Market was valued at USD 2.6 billion in 2024. This growth stems from the steady rise in international shipping traffic, continued investment in offshore oil and wind energy infrastructure, and a robust increase in leisure boating activities. The country's well-developed port systems and supportive regulatory environment further enhance the uptake of advanced marine propulsion technologies. This favorable ecosystem encourages commercial and recreational marine operators to invest in newer, more efficient engines that meet modern performance and environmental standards.

Key players in the market include Caterpillar, Wartsila, Perkins Engines, IHI Corporation, MAN Energy Solutions, Yanmar HOLDINGS, General Electric, Briggs & Stratton, Kawasaki Heavy Industries, Cummins, Yamaha Motor, Scania, AB Volvo Penta, Rehlko, KUBOTA Corporation, MITSUBISHI HEAVY INDUSTRIES, Rolls-Royce, J C Bamford Excavators, American Honda Motor, and Guascor Energy. To enhance their market standing, companies leverage strategies such as investing in R&D to develop low-emission, fuel-efficient engines tailored for regulatory compliance. Many focus on hybrid and gas engine technologies to align with decarbonization trends. Partnerships with shipbuilders and fleet operators help secure long-term supply agreements, while geographic expansion in emerging coastal economies opens new revenue streams. Advanced digital monitoring systems are being incorporated to offer predictive maintenance and real-time diagnostics. Brands expand service networks to improve aftersales support, ensuring long-term customer engagement and reliability in performance-critical applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel, 2021 - 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 Diesel

- 5.3 Gas

- 5.4 Others

Chapter 6 Market Size and Forecast, By Rated Power, 2021 - 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 0.5 MW - 1 MW

- 6.3 > 1 MW - 2 MW

- 6.4 > 2 MW - 3.5 MW

- 6.5 > 3.5 MW - 5 MW

- 6.6 > 5 MW - 7.5 MW

- 6.7 > 7.5 MW

Chapter 7 Market Size and Forecast, By Cylinder Configuration, 2021 - 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 Inline

- 7.3 V-Type

- 7.4 Radial

- 7.5 Opposed piston

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & MW)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Denmark

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Thailand

- 8.4.7 Singapore

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 Qatar

- 8.5.4 Oman

- 8.5.5 Kuwait

- 8.5.6 Egypt

- 8.5.7 Turkey

- 8.5.8 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

Chapter 9 Company Profiles

- 9.1 AB Volvo Penta

- 9.2 American Honda Motor

- 9.3 Briggs & Stratton

- 9.4 Caterpillar

- 9.5 Cummins

- 9.6 General Electric

- 9.7 Guascor Energy

- 9.8 IHI Corporation

- 9.9 J C Bamford Excavators

- 9.10 Kawasaki Heavy Industries

- 9.11 KUBOTA Corporation

- 9.12 MAN Energy Solutions

- 9.13 MITSUBISHI HEAVY INDUSTRIES

- 9.14 Perkins Engines

- 9.15 Rehlko

- 9.16 Rolls-Royce

- 9.17 Scania

- 9.18 Wartsilä

- 9.19 Yamaha Motor

- 9.20 Yanmar HOLDINGS