|

市場調査レポート

商品コード

1685062

船舶用エンジン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Marine Engines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 船舶用エンジン市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月13日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

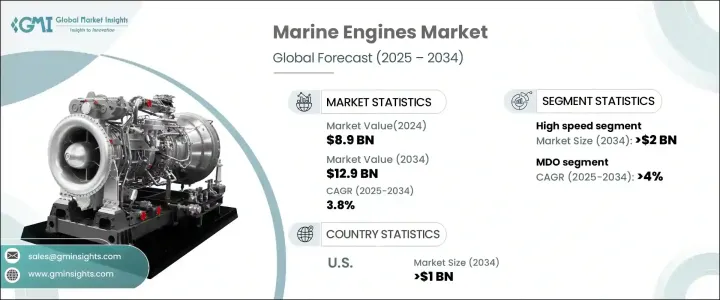

世界の船舶用エンジン市場は、2024年に89億米ドルと評価され、2025年から2034年までのCAGRは3.8%と予想され、着実な成長が見込まれています。

世界貿易と輸送が大きく変貌を遂げる中、進化するコスト、サプライチェーンモデル、ロジスティクスの枠組みが国際商取引の風景を再構築しています。こうした変化は各国の競合に影響を及ぼし、各国は世界な輸送ネットワークにさらに組み込まれつつあります。貿易は依然として経済開発に不可欠な原動力であり、より効率的な海洋エンジンへの需要を煽っています。港湾インフラへの投資の増加、船舶技術の急速な進歩、海上輸送量の増加は、すべて市場を強化する要因です。環境問題への関心が高まり続ける中、特に燃料効率や排出ガスの削減など、環境に優しいソリューションへのシフトが顕著になっています。世界的により厳しい規制が施行される中、持続可能な船舶用エンジン技術への注目が市場の中心的な促進要因となっています。

高速船舶用エンジンの需要は、2034年までに20億米ドルに達すると予測されています。この急増は、港湾施設の開発が進んでいることと、強力なタグボートの需要が増加していることに起因しています。小型船舶、ヨット、フェリー、漁船は、効率を向上させるだけでなく、燃料消費と運用コストを削減するコンパクトなエンジン設計を特に採用しています。これらのエンジンは、全体的な環境フットプリントの削減に貢献しながら優れた性能を発揮するため、さまざまな海洋用途で非常に魅力的な選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 89億米ドル |

| 予測金額 | 129億米ドル |

| CAGR | 3.8% |

一方、MDO(船舶用ディーゼルオイル)船舶用エンジン分野は、2034年までCAGR 4%で成長します。これらのエンジンは、その効率性と、騒音レベルを低く抑えながら高速運航を維持する能力により、人気が高まっています。4ストロークエンジンの設計は、1サイクルおきに燃料を消費することで燃料効率を高めており、ストロークごとに燃料を消費する2ストロークエンジンとは異なる特徴を持っています。さらに、MDOエンジンはオイルや潤滑油の注入を必要としないため、排出ガスが少なく環境に優しいです。

米国の船舶用エンジン市場も大幅に拡大しており、2034年までに10億米ドルを創出すると予測されています。ディーゼルエンジン技術の進歩は、メーカーが性能向上のために技術革新を続けているため、需要促進に重要な役割を果たしています。経済成長、信頼性の高いエンジン性能への注目の高まり、豪華で快適な機能への投資の増加は、この拡大の主な要因です。さらに、海上輸送の継続的な成長は、より高度で効率的な船船舶用エンジンに対する長期的なニーズを生み出しています。このような多面的な開発は、米国市場の持続的な成長軌道を反映しています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 市場推計・予測パラメータ

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的展望

- イノベーションと持続可能性の展望

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- MDO

- MGO

- LNG

- ハイブリッド

- その他

第6章 市場規模・予測:馬力別、2021年~2034年

- 主要動向

- 1,000HP未満

- 1,000~5,000HP

- 5,001~10,000HP

- 10,001~20,000HP

- 20,000HP以上

第7章 市場規模・予測:技術別、2021年~2034年

- 主要動向

- 低速

- 中速

- 高速

第8章 市場規模・予測:推進別、2021年~2034年

- 主要動向

- 2ストローク

- 4ストローク

第9章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 商船

- コンテナ船

- タンカー

- バルクキャリア

- ガスキャリア

- RO-RO船

- その他

- オフショア

- 掘削装置及び船舶

- アンカーハンドリング船

- オフショア支援船

- 浮体式生産ユニット

- プラットフォーム供給船

- クルーズ&フェリー

- クルーズ船

- 旅客フェリー

- 客船/貨物船

- 海軍

- その他

第10章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- イタリア

- ノルウェー

- フランス

- ロシア

- デンマーク

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- ベトナム

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- イラン

- アンゴラ

- エジプト

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

第11章 企業プロファイル

- AB Volvo Penta

- Anglo Belgian Corporation

- Brunswick Corporation

- Caterpillar

- Cummins

- Daihatsu Diesel

- DEUTZ

- Deere &Company

- Hyundai Heavy Industries

- IHI Corporation

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Rolls-Royce

- SociétéInternationale des Moteurs Baudouin

- Scania

- Shanghai Diesel Engine

- STX Engines

- Wärtsilä

- Weichai Holding

- Yamaha

- Yanmar

- Yuchai International

The Global Marine Engines Market, valued at USD 8.9 billion in 2024, is poised for steady growth with an expected CAGR of 3.8% from 2025 to 2034. As global trade and transportation undergo significant transformation, evolving costs, supply chain models, and logistics frameworks are reshaping the landscape of international commerce. These changes are influencing the competitiveness of nations, integrating them further into global transport networks. Trade remains an essential driver of economic development, fueling the demand for more efficient marine engines. The growing investments in port infrastructure, rapid advancements in vessel technology, and the increasing volume of seaborne transportation are all factors bolstering the market. As environmental concerns continue to rise, there is a notable shift towards eco-friendly solutions, particularly in fuel efficiency and emissions reduction. With more stringent regulations being enforced globally, the focus on sustainable marine engine technology is becoming a central market driver.

The demand for high-speed marine engines is projected to reach USD 2 billion by 2034. This surge can be attributed to the ongoing development of port facilities and the increasing demand for powerful tugboats. Small vessels, yachts, ferries, and fishing boats are particularly adopting compact engine designs that not only improve efficiency but also cut down fuel consumption and operational costs. These engines offer excellent performance while helping to reduce the overall environmental footprint, making them a highly attractive option across various marine applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.9 Billion |

| Forecast Value | $12.9 Billion |

| CAGR | 3.8% |

On the other hand, the MDO (Marine Diesel Oil) marine engine segment is set to grow at a CAGR of 4% through 2034. These engines are increasingly popular due to their efficiency and ability to maintain high-speed operations while keeping noise levels low. Their four-stroke engine design enhances fuel efficiency by consuming fuel every other cycle, a feature that distinguishes them from two-stroke engines that consume fuel with every stroke. Additionally, MDO engines don't require oil or lubricant injections, making them more eco-friendly by producing fewer emissions, thus aligning with tightening environmental regulations.

The U.S. marine engines market is also witnessing considerable expansion, projected to generate USD 1 billion by 2034. Advancements in diesel engine technology are playing a significant role in driving demand as manufacturers continue to innovate for better performance. Economic growth, an increasing focus on reliable engine performance, and rising investment in luxury and comfort features are key contributors to this expansion. Furthermore, the continuous growth in seaborne transportation is creating a long-term need for more advanced and efficient marine engines. This multi-faceted development reflects the sustained growth trajectory of the market in the U.S.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (Units & USD Million)

- 5.1 Key trends

- 5.2 MDO

- 5.3 MGO

- 5.4 LNG

- 5.5 Hybrid

- 5.6 Others

Chapter 6 Market Size and Forecast, By Power, 2021 – 2034 (Units & USD Million)

- 6.1 Key trends

- 6.2 < 1,000 HP

- 6.3 1,000 - 5,000 HP

- 6.4 5,001 - 10,000 HP

- 6.5 10,001 - 20,000 HP

- 6.6 > 20,000 HP

Chapter 7 Market Size and Forecast, By Technology, 2021 – 2034 (Units & USD Million)

- 7.1 Key trends

- 7.2 Low speed

- 7.3 Medium speed

- 7.4 High speed

Chapter 8 Market Size and Forecast, By Propulsion, 2021 – 2034 (Units & USD Million)

- 8.1 Key trends

- 8.2 2 stroke

- 8.3 4 stroke

Chapter 9 Market Size and Forecast, By Application, 2021 – 2034 (Units & USD Million)

- 9.1 Key trends

- 9.2 Merchant

- 9.2.1 Container vessels

- 9.2.2 Tankers

- 9.2.3 Bulk carriers

- 9.2.4 Gas carriers

- 9.2.5 RO-RO

- 9.2.6 Others

- 9.3 Offshore

- 9.3.1 Drilling RIGS & ships

- 9.3.2 Anchor handling vessels

- 9.3.3 Offshore support vessels

- 9.3.4 Floating production units

- 9.3.5 Platform supply vessels

- 9.4 Cruise & Ferry

- 9.4.1 Cruise vessels

- 9.4.2 Passenger ferries

- 9.4.3 Passenger/cargo vessels

- 9.5 Navy

- 9.6 Others

Chapter 10 Market Size and Forecast, By Region, 2021 – 2034 (Units & USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 Italy

- 10.3.4 Norway

- 10.3.5 France

- 10.3.6 Russia

- 10.3.7 Denmark

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Vietnam

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Iran

- 10.5.4 Angola

- 10.5.5 Egypt

- 10.5.6 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Mexico

Chapter 11 Company Profiles

- 11.1 AB Volvo Penta

- 11.2 Anglo Belgian Corporation

- 11.3 Brunswick Corporation

- 11.4 Caterpillar

- 11.5 Cummins

- 11.6 Daihatsu Diesel

- 11.7 DEUTZ

- 11.8 Deere & Company

- 11.9 Hyundai Heavy Industries

- 11.10 IHI Corporation

- 11.11 MAN Energy Solutions

- 11.12 Mitsubishi Heavy Industries

- 11.13 Rolls-Royce

- 11.14 Société Internationale des Moteurs Baudouin

- 11.15 Scania

- 11.16 Shanghai Diesel Engine

- 11.17 STX Engines

- 11.18 Wärtsilä

- 11.19 Weichai Holding

- 11.20 Yamaha

- 11.21 Yanmar

- 11.22 Yuchai International