高圧電源・制御ケーブルの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

High Voltage Power and Control Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 122 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755372

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

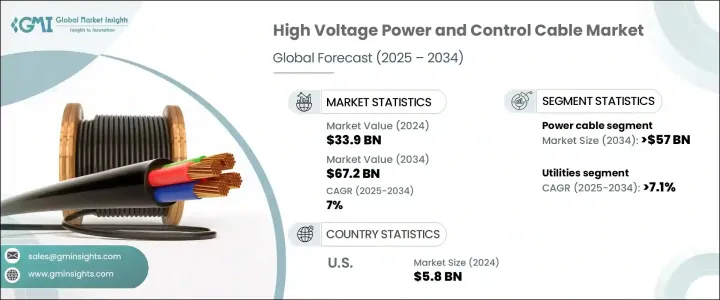

高圧電源・制御ケーブルの世界市場規模は、2024年に339億米ドルとなり、CAGR 7%で成長し、2034年には672億米ドルに達すると予測されています。

この成長を牽引しているのは、主に再生可能エネルギー源への世界の移行が加速していることです。世界各国がエネルギーシステムの脱炭素化に向けた取り組みを強化するなか、大容量で効率的な送電インフラに対する需要が大幅に伸びています。このシフトにより、高圧ケーブルは現代の送電ネットワークにおいて重要なコンポーネントとなっています。

これらのケーブルは、特に遠隔地の再生可能エネルギー設備から集中型送電網システムへの長距離送電に不可欠です。政府や民間企業は、拡大する再生可能エネルギー容量をサポートし、送電網の耐障害性を向上させるため、送電インフラのアップグレードに多額の投資を行っています。この動向は、進行中の産業開発と都市拡張と相まって、高度高圧ケーブルに対する一貫した需要を生み出しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 339億米ドル |

| 予測金額 | 672億米ドル |

| CAGR | 7% |

特に新興経済諸国では、信頼性の高い配電とスマートグリッド開発へのニーズが高まっており、こうした見通しの明るさに拍車をかけています。多くの新興地域では、急速な工業化と都市インフラの拡大が、堅牢な送電システムへの需要を押し上げています。同時に、先進経済諸国は老朽化したインフラの近代化と送電ロスの削減に注力しており、高圧ケーブルの役割をさらに高めています。

技術的進歩は市場情勢を大きく形成しています。メーカーは、架橋ポリエチレン(XLPE)などの高性能素材を導入し、進化する規制や環境基準を満たすために絶縁技術を革新しています。これらの技術革新は、熱的・機械的性能を向上させるだけでなく、安全性と耐久性も高めています。その結果、最新の高圧ケーブルはより効率的で信頼性が高くなり、産業、商業、公共事業の各分野の重要な用途に魅力的な選択肢となっています。さらに、研究開発投資の増加により、電力損失を最小限に抑えながら高電圧に対応できるケーブルの開発が促進されており、これは再生可能エネルギーによる長距離送電にとって極めて重要な要素となっています。

世界市場はまた、需要の地域シフトも経験しています。アジア太平洋諸国、特に中国、インド、日本は、より広範な経済開発戦略の一環として、電力インフラに多大な資源を割り当てています。これらの地域では大規模な都市化が進んでおり、電力消費の増加と安定した送電網の必要性が高まっています。一方、北米は、クリーンエネルギーの統合と送電網の近代化に焦点を当てた政府プログラムに支えられ、大幅な成長を続けています。電力供給の改善と排出量削減を目的としたインフラ・プロジェクトが、同地域の市場成長に弾みをつけています。

2034年までに、電力ケーブル分野だけで570億米ドルを超えると予測されています。この成長は、再生可能エネルギーや産業プロセスから発生する電力負荷の増加に対応できる大容量送電線のニーズが急増していることが主な要因です。都市が拡大し、スマートインフラが現実のものとなるにつれて、高性能ケーブルはこれまで以上に重要になっています。特に洋上風力発電所やソーラーパークから長距離にわたって効率的に電力を輸送する必要があるため、耐久性と高電圧に対応したソリューションに対する需要がさらに高まっています。

用途別では、公益事業分野が2034年までCAGR 7.1%超で成長する見通しです。これは、送配電網の開発が急ピッチで進んでいることと、送電網の自動化が引き続き推進されていることが主な要因です。公益事業者は、エネルギー情勢の変化に対応するため、老朽化したインフラを近代化する必要に迫られています。これには、新技術の統合、信頼性の向上、より分散型の発電モデルへの準備などが含まれます。世界のエネルギー消費量が大幅に増加すると予測される中、電力会社は、環境への影響を最小限に抑えつつ、中断のない電力を供給できるインフラへの投資を迫られています。

米国は引き続きこの市場の主要企業であり、その高圧電源・制御ケーブル産業は2022年に49億米ドルと評価され、2023年には54億米ドル、2024年には58億米ドルに増加します。同国の強力な経済地位とクリーンエネルギーおよびインフラ開発に継続的に重点が置かれていることが、市場の着実な拡大に寄与しています。国営送電網の近代化に対する支援の高まりに伴い、先進的なケーブル・ソリューションに対する需要は今後も堅調に推移すると予想されます。

欧州もまた、化石燃料からの脱却を加速させ、持続可能なエネルギー慣行を重点的に採用していることから、市場拡大において極めて重要な役割を果たしています。この地域では、二酸化炭素排出量の削減と再生可能エネルギーの統合に取り組んでおり、電力インフラへの投資が拡大しています。欧州各国は、安定した電力供給を確保するために送電網の強化に多額の投資を行っており、高性能ケーブル・ソリューションへの需要がさらに高まっています。

業界競争は、世界市場シェアの20%以上を占める大手企業によって形成されています。エネルギーシステムとオートメーションに強い専門知識を持つ大手企業は、技術革新、性能、信頼性のベンチマークを設定し続けています。その技術的優位性と深い専門知識は、エネルギー効率が高く大容量のソリューションに対する世界の需要の高まりに対応するケーブルの供給において競争力を発揮しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 電源ケーブル

- 制御ケーブル

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- ユーティリティ

- 産業

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- オランダ

- イタリア

- スペイン

- ドイツ

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

- ペルー

第8章 企業プロファイル

- Bahra Electric

- Belden Inc.

- Elsewedy Electric

- FURUKAWA ELECTRIC

- Havells India.

- KEI Industries

- Klaus Faber

- Leoni Cables

- LS Cables

- NKT A/S

- Polycab

- Prysmian Group

- Riyadh Cables

- RR Kabel

- Southwire Company LLC

- Sumitomo Electric

- Thermo Cables

- Top Cables

目次

The Global High Voltage Power and Control Cable Market was valued at USD 33.9 billion in 2024 and is estimated to grow at a CAGR of 7% to reach USD 67.2 billion by 2034. The growth is driven primarily by the accelerating global transition toward renewable energy sources. As countries around the world intensify efforts to decarbonize their energy systems, the demand for high-capacity, efficient transmission infrastructure has grown substantially. This shift has made high voltage cables a critical component in modern electricity transmission networks.

These cables are indispensable for transporting power over long distances, particularly from remote renewable energy installations to centralized grid systems. Governments and private sector players are investing heavily in upgrading their transmission infrastructure to support the expanding renewable energy capacity and to improve grid resilience. This trend, coupled with ongoing industrial development and urban expansion, is creating consistent demand for advanced high voltage cables.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $33.9 Billion |

| Forecast Value | $67.2 Billion |

| CAGR | 7% |

The increasing need for reliable electricity distribution and smart grid development, especially in developing economies, is adding to this positive outlook. In many emerging regions, rapid industrialization and urban infrastructure expansion are pushing the demand for robust power transmission systems. Simultaneously, developed economies are focusing on modernizing aging infrastructure and reducing transmission losses, further amplifying the role of high voltage cables.

Technological advancements are significantly shaping the market landscape. Manufacturers are introducing high-performance materials such as cross-linked polyethylene (XLPE) and innovating in insulation technologies to meet evolving regulatory and environmental standards. These innovations not only improve thermal and mechanical performance but also enhance safety and durability. As a result, modern high voltage cables are more efficient and dependable, making them an attractive choice for high-stakes applications across industrial, commercial, and utility sectors. Moreover, increased R&D investments are facilitating the development of cables that can handle higher voltages while minimizing power losses, which is a crucial factor for long-distance transmission from renewable sources.

The global market is also experiencing regional shifts in demand. Countries in Asia-Pacific, particularly China, India, and Japan, are allocating significant resources to power infrastructure as part of their broader economic development strategies. These regions are undergoing massive urbanization, leading to increased electricity consumption and the need for stable transmission networks. Meanwhile, North America continues to witness substantial growth supported by government programs focused on clean energy integration and grid modernization. Infrastructure projects aimed at improving electricity delivery and reducing emissions are giving a boost to market growth in the region.

By 2034, the power cable segment alone is projected to surpass USD 57 billion. This growth is largely attributed to the surging need for high-capacity transmission lines capable of accommodating the increasing power load generated from renewable energy and industrial processes. As cities expand and smart infrastructure becomes a reality, high-performance cables are becoming more critical than ever. The necessity to transport power efficiently across long distances, particularly from offshore wind farms and solar parks, adds another layer of demand for durable and high-voltage-capable solutions.

In terms of application, the utilities segment is poised to grow at a CAGR exceeding 7.1% through 2034. This is largely driven by the fast-paced development of electric transmission and distribution networks and the continued push toward grid automation. Utility providers are being pushed to modernize aging infrastructure to meet the needs of a changing energy landscape. This includes integrating new technologies, improving reliability, and preparing for a more decentralized power generation model. With global energy consumption projected to rise significantly, utility companies are under pressure to invest in infrastructure that can deliver uninterrupted power while minimizing environmental impact.

The United States continues to be a key player in this market, with its high voltage power and control cable industry valued at USD 4.9 billion in 2022, increasing to USD 5.4 billion in 2023 and USD 5.8 billion in 2024. The country's strong economic position and ongoing emphasis on clean energy and infrastructure development are contributing to steady market expansion. With growing support for modernizing the national grid, the demand for advanced cable solutions is expected to remain robust in the coming years.

Europe also plays a pivotal role in market expansion due to its accelerated shift away from fossil fuels and a focused adoption of sustainable energy practices. The region's commitment to reducing carbon emissions and integrating renewable energy is prompting widespread investments in electricity infrastructure. Countries across Europe are heavily investing in reinforcing their power transmission frameworks to ensure stable electricity flow, further strengthening demand for high-performance cable solutions.

Industry competition is shaped by major players that collectively hold over 20% of the global market share. Leading firms with strong expertise in energy systems and automation continue to set benchmarks in innovation, performance, and reliability. Their technological advantage and deep domain knowledge give them a competitive edge in supplying cables that meet the rising global demand for energy-efficient and high-capacity solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Power cable

- 5.3 Control cable

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Utilities

- 6.3 Industries

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Netherlands

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Germany

- 7.3.7 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Kuwait

- 7.5.5 South Africa

- 7.5.6 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Peru

Chapter 8 Company Profiles

- 8.1 Bahra Electric

- 8.2 Belden Inc.

- 8.3 Elsewedy Electric

- 8.4 FURUKAWA ELECTRIC

- 8.5 Havells India.

- 8.6 KEI Industries

- 8.7 Klaus Faber

- 8.8 Leoni Cables

- 8.9 LS Cables

- 8.10 NKT A/S

- 8.11 Polycab

- 8.12 Prysmian Group

- 8.13 Riyadh Cables

- 8.14 RR Kabel

- 8.15 Southwire Company LLC

- 8.16 Sumitomo Electric

- 8.17 Thermo Cables

- 8.18 Top Cables

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 122 Pages

- 納期

- 2~3営業日