低電圧電源・制御ケーブルの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Low Voltage Power and Control Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 122 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750549

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

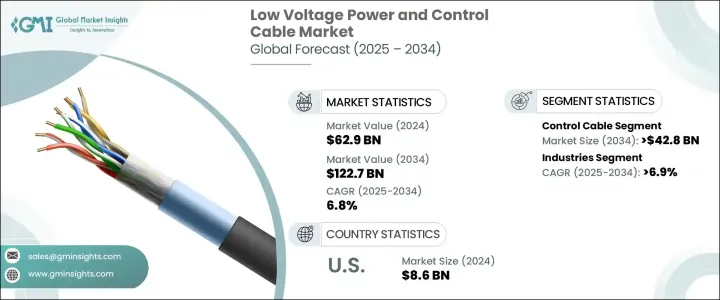

世界の低電圧電源・制御ケーブル市場は、2024年には629億米ドルと評価され、住宅、商業、産業部門からの需要増加に牽引され、CAGR 6.8%で成長し、2034年には1,227億米ドルに達すると推定されています。

先進国や開発途上国で都市化が進むにつれ、信頼性が高く効率的な配電システムの必要性が高まっています。また、メーカーがケーブルの絶縁性、難燃性、全体的な耐久性の向上に注力し、安全基準や性能への期待の高まりに応えていることから、技術の進歩も重要な役割を果たしています。さらに、温度、負荷、故障をリアルタイムで監視できるスマート・ケーブルなどの技術革新が人気を集めており、市場をさらに促進しています。

アジア太平洋地域は、堅調なインフラ開拓と産業成長により、低電圧電力・制御ケーブル市場で圧倒的な存在感を示しています。欧州と北米は、送電網の近代化とエネルギー効率の高い技術の導入を目指して多額の投資を行っており、これに続いています。世界の競争は依然として激しく、Prysmian Group、Nexans、KEI Industriesをはじめとする業界の主要企業は、市場シェアを拡大するため、一貫して技術革新と能力拡張に取り組んでいます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 629億米ドル |

| 予測金額 | 1,227億米ドル |

| CAGR | 6.8% |

電力ケーブル分野は大きな成長を遂げ、2034年には796億米ドルを超えると予想されています。この拡大は、住宅、商業、工業環境で重要な効率的な配電システムに対する需要の増加が主な要因です。スマートグリッドの急速な採用と交通システムの電化は、高度な電力ケーブルの必要性をさらに高めています。エネルギー効率が世界的に注目される中、これらの電力ケーブルの開発と導入は、エネルギーインフラの未来を形作る上で極めて重要な役割を果たすと予想されます。より持続可能なエネルギー源とスマートインフラプロジェクトへのシフトは、信頼性が高く高性能な電力ケーブルの需要を引き続き促進すると思われます。

産業部門も力強い増加傾向を示しており、自動化システムや高度な製造プロセスへのニーズが高まっている新興市場での工業化の進行が原動力となって、2034年までCAGR 6.9%で成長すると予測されています。さらに、産業界がより高い効率を追求するにつれて、信頼性の高い電力および制御システムへの需要が高まっています。工場や製造装置にオートメーションとスマート技術を統合することで、安定した操業とエネルギー管理を保証する低電圧電源および制御ケーブルの必要性が高まっています。

米国低電圧電源・制御ケーブル2024年の市場規模は86億米ドルで、住宅および商業部門の拡大が原動力となっています。同国のインフラと送電網システムの近代化は、低電圧ケーブルの需要を刺激するもう一つの重要な要因です。特に、電気自動車(EV)充電ステーションの普及とともに、エネルギー効率の高い技術の採用が米国市場の拡大に大きく貢献しています。さらに、スマートビルディングやその他のエネルギー効率の高いインフラの建設が、より高度なケーブルシステムの必要性を高めています。

低電圧電源・制御ケーブル世界市場の主要企業には、Southwire Company、古河電工、KEC International、LS Cable &System、Belden、住友電気工業、NKT A/Sなどがあります。これらの企業は、高品質で耐久性のある製品を開発し、市場でのプレゼンスを拡大する最前線にいます。市場での地位を強化するため、低電圧電源・制御ケーブル業界の企業はいくつかの重要な戦略に重点を置いています。第一に、研究開発に投資し、進化する安全基準を満たし、エネルギー効率を向上させ、リアルタイム監視システムなどの先進技術を統合した製品を革新しています。第二に、製造能力と世界な流通網を拡大し、製品の可用性を高めています。第三に、戦略的パートナーシップと買収を推進し、製品の多様化と新興国での市場シェア拡大を図っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:製品別、2021-2034

- 主要動向

- 電源ケーブル

- 制御ケーブル

第6章 市場規模・予測:用途別、2021-2034

- 主要動向

- ユーティリティ

- 産業

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- オランダ

- イタリア

- スペイン

- ドイツ

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- クウェート

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

- ペルー

第8章 企業プロファイル

- Bergen Cable Technology

- Belden

- Ducab

- Furukawa Electric

- KEI Industries

- KEC International

- Klaus Faber

- LS Cable &System

- NKT A/S

- Nexans

- Prysmian Group

- Riyadh Cables

- RR Kabel

- Southwire Company

- Sumitomo Electric

目次

The Global Low Voltage Power and Control Cable Market was valued at USD 62.9 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 122.7 billion by 2034, driven by the increasing demand from residential, commercial, and industrial sectors. As urbanization grows in developed and developing countries, the need for reliable and efficient power distribution systems intensifies. Technological advancements also play a significant role, as manufacturers focus on improving cable insulation, flame-retardant properties, and overall durability to meet rising safety standards and performance expectations. Moreover, innovations such as smart cables that can monitor temperature, load, and faults in real-time are gaining traction, further propelling the market.

The Asia Pacific region stands out as the dominant player in the low-voltage power and control cable market, thanks to its robust infrastructure development and industrial growth. Europe and North America follow closely, with substantial investments aimed at modernizing electrical grids and implementing energy-efficient technologies. Global competition remains fierce, with key industry players, including Prysmian Group, Nexans, and KEI Industries, consistently innovating and expanding their capacities to capture greater market share.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $62.9 Billion |

| Forecast Value | $122.7 Billion |

| CAGR | 6.8% |

The power cable segment is poised to experience significant growth, expected to exceed USD 79.6 billion by 2034. This expansion is largely driven by the increasing demand for efficient power distribution systems, crucial in residential, commercial, and industrial settings. The rapid adoption of smart grids and the electrification of transportation systems further amplify the need for advanced power cables. As energy efficiency becomes a focal point globally, the development and deployment of these power cables are expected to play a pivotal role in shaping the future of energy infrastructure. The shift towards more sustainable energy sources and smart infrastructure projects will continue to propel the demand for reliable and high-performance power cables.

The industrial sector is also witnessing a strong upward trend, projected to grow at a CAGR of 6.9% till 2034, driven by the ongoing industrialization in emerging markets, where there is a rising need for automated systems and sophisticated manufacturing processes. Additionally, as industries strive for greater efficiency, the demand for reliable power and control systems is growing. Integrating automation and smart technologies in factories and manufacturing units intensifies the need for low-voltage power and control cables to ensure stable operations and energy management.

United States Low Voltage Power and Control Cable Market was valued at USD 8.6 billion in 2024, driven by the expansion of the residential and commercial sectors. The modernization of infrastructure and grid systems in the country is another key factor stimulating the demand for low-voltage cables. In particular, the adoption of energy-efficient technologies, alongside the proliferation of electric vehicle (EV) charging stations, is significantly contributing to the expansion of the U.S. market. Additionally, the construction of smart buildings and other energy-efficient infrastructure drives the need for more advanced cable systems.

Major players in the Global Low Voltage Power and Control Cable Market include Southwire Company, Furukawa Electric, KEC International, LS Cable & System, Belden, Sumitomo Electric, and NKT A/S. These companies are at the forefront of developing high-quality, durable products and expanding their market presence. To strengthen their market position, companies in the low voltage power and control cable industry focus on several key strategies. First, they invest in research and development to innovate products that meet evolving safety standards, improve energy efficiency, and integrate advanced technologies like real-time monitoring systems. Second, they are expanding their manufacturing capabilities and global distribution networks to enhance product availability. Third, strategic partnerships and acquisitions are being pursued to diversify their product offerings and increase their market share in emerging economies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Power cable

- 5.3 Control cable

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Utilities

- 6.3 Industries

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Netherlands

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Germany

- 7.3.7 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Kuwait

- 7.5.5 South Africa

- 7.5.6 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Peru

Chapter 8 Company Profiles

- 8.1 Bergen Cable Technology

- 8.2 Belden

- 8.3 Ducab

- 8.4 Furukawa Electric

- 8.5 KEI Industries

- 8.6 KEC International

- 8.7 Klaus Faber

- 8.8 LS Cable & System

- 8.9 NKT A/S

- 8.10 Nexans

- 8.11 Prysmian Group

- 8.12 Riyadh Cables

- 8.13 RR Kabel

- 8.14 Southwire Company

- 8.15 Sumitomo Electric

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 122 Pages

- 納期

- 2~3営業日