|

市場調査レポート

商品コード

1755346

産業用低電圧デジタル変電所市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)Industrial Low Voltage Digital Substation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 産業用低電圧デジタル変電所市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年05月21日

発行: Global Market Insights Inc.

ページ情報: 英文 121 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

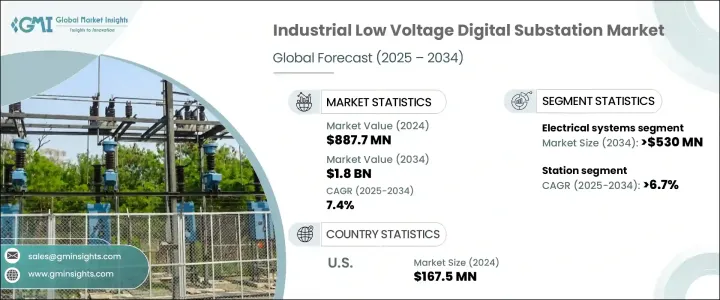

産業用低電圧デジタル変電所の世界市場は、2024年には8億8,770万米ドルとなり、CAGR 7.4%で成長し、2034年には18億米ドルに達すると予測されています。

IoTデバイス、人工知能、機械学習を組み込むことで、リアルタイムの監視と予知保全が可能になり、機器の故障を減らし、エネルギー消費を最適化することができます。政府や産業界は、将来のエネルギーシステムの基幹となるスマートグリッドの開発にますます力を入れており、この需要がデジタル変電所の導入を加速させています。これらの変電所は、配電網内の通信、自動化、制御を改善し、送電網の安定性と効率を高めます。

従来の電気機械システムとは異なり、デジタル変電所ではインテリジェント電子機器(IED)が使用され、リアルタイムのデータ収集、迅速な意思決定、予防保全が可能になります。さらに、風力や太陽光のような再生可能エネルギー源の増加により、断続的な電力を管理し、安定したエネルギー配給を確保するデジタル変電所が求められています。しかし、電気部品の輸入に影響を与える政府の政策により、変圧器やサーキットブレーカーなどの主要部品の価格が上昇する可能性があり、業界は課題に直面する可能性があります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 8億8,770万米ドル |

| 市場規模予測 | 18億米ドル |

| CAGR | 7.4% |

産業用低電圧デジタル変電所市場の電気システム部門は、2034年までに5億3,000万米ドルに達すると予測されます。この成長の原動力は、配電ネットワークにおける自動化、ロボット化、デジタル化の需要の高まりです。これらの分野が発展するにつれて、低電圧運転を効果的に管理し、システムの安全性を確保するために、変圧器、サーキットブレーカー、バスバーのような、より精密で信頼性の高い機器が必要とされています。これらの部品は、ますます複雑化・自動化する送電網において、円滑かつ効率的な配電を維持するために不可欠です。

2024年に32.8%のシェアを占めるベイ・セグメントは、デジタル変電所の運用に不可欠です。フィーダー・レベルでのスイッチング、保護、制御に不可欠な役割を果たし、局所的な意思決定を可能にし、システム全体の信頼性を高め、迅速な故障切り分けを保証します。この機能は、無停電電力供給が最も重要な大規模ユーティリティ・ネットワークにとって不可欠です。ベイレベルアーキテクチャは、システムの回復力に貢献し、最新の変電所に不可欠なコンポーネントとなっています。

米国の産業用低電圧デジタル変電所の2024年の市場規模は1億6,750万米ドルで、支援的な政策イニシアチブのほか、企業がエネルギー効率と排出量削減に注力するよう促す環境・社会・ガバナンス(ESG)原則の採用が増加していることが要因となっています。こうした要因から、エネルギー消費を最適化し、持続可能な取り組みを支援するデジタル変電所に対する需要が高まっています。

産業用低電圧デジタル変電所世界市場の主要企業には、シーメンス、シュナイダーエレクトリック、日立エネルギー、東芝エネルギーシステム&ソリューション、WEGなどがあります。これらの企業は、戦略的パートナーシップ、技術革新、効率的で自動化されたソリューションの需要増に対応する製品開拓を通じて、市場での存在感を高めることに注力しています。IoT、機械学習、AI主導の分析といった高度なデジタル・ソリューションを取り入れることで、これらの企業は製品の機能性を高めています。さらに、再生可能エネルギーや大規模な産業用途で高性能変電所に対するニーズの高まりに対応するため、より信頼性が高く、費用対効果が高く、拡張性の高いソリューションを開発するために、多くの企業が研究開発に投資しています。

目次

第1章 分析手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスクと課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略的ダッシュボード

- イノベーションと持続可能性の情勢

第5章 市場の推計・予測:コンポーネント別(2021~2034年)

- 主要動向

- 変電所自動化システム

- 通信ネットワーク

- 電気システム

- 監視制御システム

- その他

第6章 市場の推計・予測:アーキテクチャ別(2021~2034年)

- 主要動向

- プロセス

- ベイ

- ステーション

第7章 市場の推計・予測:設備別(2021~2034年)

- 主要動向

- 新規

- 改修

第8章 市場の推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- ABB

- Cisco Systems, Inc.

- Eaton Corporation

- General Electric

- Hitachi Energy

- Hubbell

- Larson &Toubro Limited

- Locamation

- Netcontrol Group

- NR Electric Co. Ltd.

- Ormazabal

- Powell Industries

- Schneider Electric

- Siemens

- Toshiba Energy Systems &Solutions Corporation

- WEG

- WAGO

The Global Industrial Low Voltage Digital Substation Market was valued at USD 887.7 million in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 1.8 billion by 2034, driven by the increasing adoption of digital substations across various industries is enhancing operational efficiency and reliability. Incorporating IoT devices, artificial intelligence, and machine learning enables real-time monitoring and predictive maintenance, reducing equipment failures and optimizing energy consumption. Governments and industries are increasingly focused on developing smart grids, which act as the backbone of future energy systems, and this demand is accelerating the implementation of digital substations. These substations improve communication, automation, and control within the power distribution network enhancing grid stability and efficiency.

Unlike traditional electromechanical systems, digital substations use intelligent electronic devices (IEDs) that enable real-time data collection, swift decision-making, and preventive maintenance. Furthermore, the rise in renewable energy sources like wind and solar is pushing for digital substations to manage intermittent power, ensuring stable energy distribution. However, industry may face challenges due to government policies impacting the importation of electrical components, leading to potential price inflation of key parts like transformers and circuit breakers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $887.7 Million |

| Forecast Value | $1.8 Billion |

| CAGR | 7.4% |

The electrical systems segment of the industrial low voltage digital substation market is expected to reach USD 530 million by 2034. This growth is driven by the rising demand for automation, robotics, and digitalization in power distribution networks. As these sectors evolve, there is a need for more precise and reliable equipment like transformers, circuit breakers, and busbars to effectively manage low voltage operations and ensure the safety of the system. These components are essential for maintaining smooth and efficient power distribution in increasingly complex and automated grids.

The bay segment, which held a 32.8% share in 2024, is crucial for operating digital substations. It plays an integral role in switching, protecting, and control at the feeder level, allowing for localized decision-making, enhancing overall system reliability, and ensuring fast fault isolation. This capability is vital for large-scale utility networks, where an uninterrupted power supply is paramount. Bay-level architecture contributes to the resilience of the system, making it an indispensable component in modern substations.

United States Industrial Low Voltage Digital Substation Market was valued at USD 167.5 million in 2024 fueled by supportive policy initiatives, as well as the increasing adoption of Environmental, Social, and Governance (ESG) principles, which encourage businesses to focus on energy efficiency and reducing emissions. These factors lead to a greater demand for digital substations that can help optimize energy consumption and support sustainability efforts.

Key players in the Global Industrial Low Voltage Digital Substation Market include Siemens, Schneider Electric, Hitachi Energy, Toshiba Energy Systems & Solutions Corporation, and WEG, among others. These companies focus on expanding their market presence through strategic partnerships, technological innovations, and product developments that cater to the increasing demand for efficient, automated solutions. By incorporating advanced digital solutions like IoT, machine learning, and AI-driven analytics, these players are enhancing the functionality of their products. In addition, many are investing in R&D to develop more reliable, cost-effective, and scalable solutions that meet the growing need for high-performance substations in renewable energy and large-scale industrial applications.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Component, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Substation automation system

- 5.3 Communication network

- 5.4 Electrical system

- 5.5 Monitoring & control system

- 5.6 Others

Chapter 6 Market Size and Forecast, By Architecture, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Process

- 6.3 Bay

- 6.4 Station

Chapter 7 Market Size and Forecast, By Installation, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 New

- 7.3 Refurbished

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Italy

- 8.3.5 Russia

- 8.3.6 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Turkey

- 8.5.4 South Africa

- 8.5.5 Egypt

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Cisco Systems, Inc.

- 9.3 Eaton Corporation

- 9.4 General Electric

- 9.5 Hitachi Energy

- 9.6 Hubbell

- 9.7 Larson & Toubro Limited

- 9.8 Locamation

- 9.9 Netcontrol Group

- 9.10 NR Electric Co. Ltd.

- 9.11 Ormazabal

- 9.12 Powell Industries

- 9.13 Schneider Electric

- 9.14 Siemens

- 9.15 Toshiba Energy Systems & Solutions Corporation

- 9.16 WEG

- 9.17 WAGO