|

市場調査レポート

商品コード

1755338

電動三輪車市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年)Electric Three-Wheeler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 電動三輪車市場:市場機会、成長促進要因、産業動向分析、将来予測(2025~2034年) |

|

出版日: 2025年05月30日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

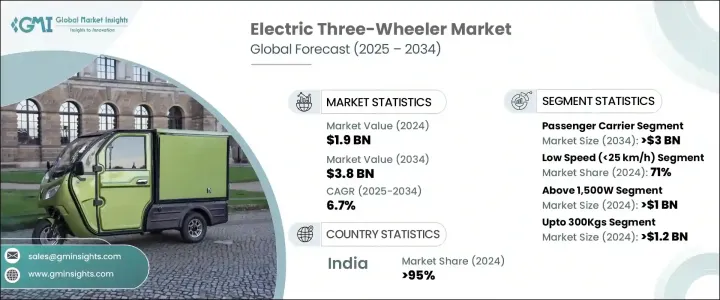

世界の電動三輪車(E3W)市場は、2024年には19億米ドルとなり、CAGR 6.7%で成長し、2034年には38億米ドルに達すると推定されています。

この急成長の背景には、燃料価格の上昇、EV導入インセンティブの拡大、手頃な都市交通への注目の高まりがあります。電動三輪車は、人口密度の高い都市環境における短距離およびラストマイル接続に理想的なソリューションを提供します。EV充電インフラの拡大とバッテリー技術の進歩により、EVの航続距離と性能も向上しています。各地域の持続可能な輸送に対する支援政策や投資と相まって、この市場は、コスト効率の高いクリーンなモビリティ・ソリューションを求める個人ユーザーと商用フリート・オペレーターの両方から大きな支持を得ています。

電動三輪車は、内燃機関の代替品に比べ、運用面で説得力のある利点を提供します。最小限のメンテナンスで済み、燃料費も大幅に削減できるため、総所有コストは魅力的です。このため、日常的な商業用途には特に適しています。アフリカ、アジア、欧州などの地域の多くの政府は、補助金、免税、料金免除などの制度を通じて、EV購入にインセンティブを与えています。こうした措置は、電気モビリティを促進する各国独自のプログラムとともに、価格ギャップを埋め、電気車両へのシフトを加速するのに役立っています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測期間 | 2025~2034年 |

| 当初の市場規模 | 19億米ドル |

| 市場規模予測 | 38億米ドル |

| CAGR | 6.7% |

旅客輸送車セグメントは2024年に13億米ドルを生み出し、2034年までに30億米ドルを生み出すと予想されています。都市部や半都市部では、公共交通機関の代替手段として電動三輪車が広く利用されていることが、この成長を後押ししています。従来の公共交通機関へのアクセスが限られている人々にとって、これらの車両は信頼性が高く低コストの通勤ソリューションを提供します。ライドヘイリングや共有モビリティ・プラットフォームとの統合により、利用率はさらに高まっています。その他の特典として、所有コストの低さ、短期間での回収、運転のしやすさなどがあり、起業家やフリートベースの輸送事業者が電動モデルを大規模に採用する動機となっています。

速度25km/h以下の電動三輪車セグメントは、2024年に71%のシェアを獲得しました。こうした低速車両は、特に短距離・低速移動が主流である新興諸国において、廃棄物処理、地域配送、施設輸送といった特殊な公共事業にますます導入されるようになっています。ライセンシング規制が緩く、コストが低く、環境に優しい運転が可能なため、人気が高まっています。農村部の電化とクリーンモビリティを目的とした政府の支援は、地域輸送用途での小型EVの使用をさらに後押ししています。

アジア太平洋の電動三輪車2024年の市場シェアは95%でした。インドでは、旅客輸送と貨物輸送の両方で三輪自動車への依存度が高く、特にTier IIとTier IIIの都市で採用が進んでいます。国や州レベルの政策、スクラップ制度、啓蒙キャンペーンなど、同国のEVエコシステムの支援により、都心部でも農村部でも電動モビリティへの移行が加速しています。電動三輪車の需要は、マイクロモビリティとラストワンマイル・ロジスティクスで旺盛であり、このセクターの適応性と費用対効果を反映しています。

電動三輪車市場に参入している主要企業には、Hotage India、Mahindra Last Mile Mobility、Dilli Electric Auto、YC Electric、Energy Electric Vehicles、Piaggio Vehicles、Unique International、Saera Electric Auto、Bajaj Auto、Mini Metro EVなどがあります。電動三輪車市場での地位を強化するため、各社は貨物用と旅客用の両方に合わせたモデルで製品ポートフォリオを拡大することに注力しています。多くのプレーヤーは、バッテリー効率の向上、航続距離の延長、充電時間の短縮のための研究開発に投資しています。バッテリー・サプライヤー、フリート・オペレーター、充電インフラ・プロバイダーとの戦略的パートナーシップは、事業規模の拡大に役立っています。メーカーはまた、価格に敏感な市場のニーズに応えるため、現地生産とリーン生産によるコスト最適化を優先しています。ブランディングの努力、ディーラーの拡大、アフターサービスの改善により、市場への浸透がさらに進んでいます。

目次

第1章 分析手法

- 市場の範囲と定義

- 分析デザイン

- 分析アプローチ

- データ収集方法

- データマイニングのソース

- 地域

- 国

- 基本的な推定・計算法

- 基準年計算

- 市場予測の主な動向

- 1次分析と検証

- 一次情報

- 予測モデル

- 分析の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 運用・保守コストの低さ

- 政府のインセンティブと補助金

- バッテリー技術の進歩とバッテリー価格の低下

- 厳しい排出基準と環境規制

- スマートテクノロジーの統合

- 業界の潜在的リスクと課題

- 限られた充電インフラ

- 初期購入コストが高め

- 市場機会

- 充電インフラの開発

- 軽商用車の代替

- ラストマイル配送の拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 国別

- 車両別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- 消費者行動分析

- 利用動向:旅客通勤vs.貨物輸送

- 購入決定要因(価格、ブランド、範囲)

- 保険とアフターマーケットの動向分析

- 商業用E3Wの保険採用

- バッテリー交換とローカライズされたアフターマーケットサービス

- メンテナンス費用の比較:電気自動車とICE三輪車

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニング・マトリックス

- 戦略的展望マトリックス

- 主な発展

- 企業合併・買収 (M&A)

- 事業提携・協力

- 新製品の発売

- 拡張計画と資金調達

- 製品ベンチマーク

- 範囲

- バッテリー寿命

- 構築と設計

- 接続性と技術機能

- アフターサービス

第5章 市場の推計・予測:車両別(2021~2034年)

- 主要動向

- 旅客輸送車

- 貨物輸送車

第6章 市場の推計・予測:バッテリー別(2021~2034年)

- 主要動向

- リチウムイオン

- 鉛蓄電池

第7章 市場の推計・予測:電力容量別(2021~2034年)

- 主要動向

- 1,000W以下

- 1,000W~1,500W

- 1,500W以上

第8章 市場の推計・予測:バッテリー容量別(2021~2034年)

- 主要動向

- 3kWh未満

- 3~6kWh

- 6kWh以上

第9章 市場の推計・予測:速度別(2021~2034年)

- 主要動向

- 低速(25 km/h未満)

- 高速(25 km/h以上)

第10章 市場の推計・予測:積載量別(2021~2034年)

- 主要動向

- 300kg未満

- 300kg以上

第11章 市場の推計・予測:地域別(2021~2034年)

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- 江蘇省

- 河南省

- 河北省

- 山東省

- 広東省

- 浙江省

- その他

- インド

- ウッタル・プラデーシュ州

- ビハール州

- アッサム

- ラジャスタン州

- その他

- その他

- 日本

- 韓国

- オーストラリア

- 東南アジア

- 中国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第12章 企業プロファイル

- Altigreen Propulsion Labs

- Atul Auto

- Avon EV

- Bajaj Auto

- Dilli Electric Auto

- Energy Electric Vehicles

- Euler Motors

- Greaves Electric Mobility

- Hotage India

- J.S. Auto

- Mahindra Last Mile Mobility

- Mini Metro EV

- Montra Electric

- Omega Seiki Mobility

- Piaggio Vehicles

- Saera Electric Auto

- TVS Motor Company

- Unique International

- VeeEss Eelectric

- YC Electric

The Global Electric Three-Wheeler Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 3.8 billion by 2034. This rapid growth is driven by rising fuel prices, expanding EV adoption incentives, and an increasing focus on affordable urban transportation. Electric three-wheelers offer an ideal solution for short-distance and last-mile connectivity in densely populated urban settings. The expansion of EV charging infrastructure and advances in battery technology are also improving the range and performance of these vehicles. Coupled with supportive policies and investment in sustainable transport across regions, the market is witnessing significant traction among both private users and commercial fleet operators seeking cost-efficient, clean mobility solutions.

Electric three-wheelers offer compelling operational advantages over internal combustion engine alternatives. With minimal maintenance needs and significantly lower fuel costs, they present an attractive total cost of ownership. This makes them especially viable for daily-use commercial applications. Many governments across regions like Africa, Asia, and Europe are incentivizing EV purchases through schemes offering subsidies, tax exemptions, and fee waivers. These measures, along with country-specific programs to promote electric mobility, are helping bridge the price gap and accelerate the shift to electric fleets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 6.7% |

The passenger carrier segment generated USD 1.3 billion in 2024 and is expected to generate USD 3 billion by 2034. The widespread use of electric three-wheelers as public transport alternatives in urban and semi-urban areas is fueling this growth. For populations with limited access to conventional public transit, these vehicles offer a reliable and low-cost commuting solution. Their integration with ride-hailing and shared mobility platforms is further increasing utilization rates. Additionally, benefits such as low ownership costs, quick returns, and ease of driving are motivating entrepreneurs and fleet-based transport providers to adopt electric models at scale.

Electric three-wheelers with a top speed of 25 km/h segment captured a 71% share in 2024. These low-speed vehicles are increasingly being deployed for specialized utility tasks such as waste management, local delivery, and institutional transport, particularly in developing countries where short-distance, low-speed travel is the norm. Their popularity is bolstered by lenient licensing norms, lower costs, and eco-friendly operation. Government support aimed at rural electrification and clean mobility is further encouraging the use of light-duty EVs for local transport applications.

Asia Pacific Electric Three-Wheeler Market held a 95% share in 2024. India's strong reliance on three-wheeled vehicles for both passenger and cargo transport-especially in Tier II and Tier III cities-continues to drive adoption. The country's supportive EV ecosystem, including national and state-level policies, scrappage schemes, and awareness campaigns, is accelerating the transition to electric mobility in both urban centers and rural corridors. Demand for electric three-wheelers is strong in micro-mobility and last-mile logistics, reflecting the sector's adaptability and cost-effectiveness.

Major companies operating in the Electric Three-Wheeler Market include Hotage India, Mahindra Last Mile Mobility, Dilli Electric Auto, YC Electric, Energy Electric Vehicles, Piaggio Vehicles, Unique International, Saera Electric Auto, Bajaj Auto, and Mini Metro EV. To strengthen their position in the electric three-wheeler market, companies are focusing on expanding their product portfolios with models tailored to both cargo and passenger applications. Many players are investing in R&D to improve battery efficiency, enhance range, and reduce charging time. Strategic partnerships with battery suppliers, fleet operators, and charging infrastructure providers are helping them scale operations. Manufacturers are also prioritizing cost optimization through localized production and lean manufacturing to meet the needs of price-sensitive markets. Branding efforts, dealer expansion, and after-sales service improvements are further enabling deeper market penetration.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Region

- 1.3.2 Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Battery

- 2.2.4 Power capacity

- 2.2.5 Battery capacity

- 2.2.6 Speed

- 2.2.7 Payload capacity

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Low operating and maintenance costs

- 3.2.1.2 Government incentives and subsidies

- 3.2.1.3 Advancements in battery technology and reducing battery prices

- 3.2.1.4 Stringent emission norms and environmental regulations

- 3.2.1.5 Integration of smart technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited charging infrastructure

- 3.2.2.2 High initial purchase cost

- 3.2.3 Market opportunities

- 3.2.3.1 Charging infrastructure development

- 3.2.3.2 Light commercial vehicle replacement

- 3.2.3.3 Last-mile delivery expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By country

- 3.8.2 By vehicle

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Consumer behavior analysis

- 3.13.1 Usage trends: passenger commute vs. goods transport

- 3.13.2 Purchase decision factors (price, brand, range)

- 3.14 Analysis of insurance and aftermarket trends

- 3.14.1. Insurance adoption for commercial E3 Ws

- 3.14.2 Battery replacement & localized aftermarket services

- 3.14.3 Comparative maintenance costs: Electric vs. ICE 3-wheelers

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Product benchmarking

- 4.7.1 Range

- 4.7.2 Battery life

- 4.7.3 Build and design

- 4.7.4 Connectivity & tech features

- 4.7.5 Aftermarket service

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger carrier

- 5.3 Load carrier

Chapter 6 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Lithium-ion

- 6.3 Lead acid

Chapter 7 Market Estimates & Forecast, By Power Capacity, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Below 1,000W

- 7.3 1,000W-1,500W

- 7.4 Above 1,500W

Chapter 8 Market Estimates & Forecast, By Battery Capacity, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Below 3kWh

- 8.3 3-6kWh

- 8.4 Above 6kWh

Chapter 9 Market Estimates & Forecast, By Speed, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Low speed (<25 km/h)

- 9.3 High speed (≥25 km/h)

Chapter 10 Market Estimates & Forecast, By Payload Capacity, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 Upto 300Kgs

- 10.3 Above 300Kgs

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.1.1 Jiangsu

- 11.4.1.2 Henan

- 11.4.1.3 Hebei

- 11.4.1.4 Shandong

- 11.4.1.5 Guangdong

- 11.4.1.6 Zhejiang

- 11.4.1.7 Others

- 11.4.2 India

- 11.4.2.1 Uttar Pradesh

- 11.4.2.2 Bihar

- 11.4.2.3 Assam

- 11.4.2.4 Rajasthan

- 11.4.2.5 Others

- 11.4.2.6 Others

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Southeast Asia

- 11.4.1 China

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Altigreen Propulsion Labs

- 12.2 Atul Auto

- 12.3 Avon EV

- 12.4 Bajaj Auto

- 12.5 Dilli Electric Auto

- 12.6 Energy Electric Vehicles

- 12.7 Euler Motors

- 12.8 Greaves Electric Mobility

- 12.9 Hotage India

- 12.10 J.S. Auto

- 12.11 Mahindra Last Mile Mobility

- 12.12 Mini Metro EV

- 12.13 Montra Electric

- 12.14 Omega Seiki Mobility

- 12.15 Piaggio Vehicles

- 12.16 Saera Electric Auto

- 12.17 TVS Motor Company

- 12.18 Unique International

- 12.19 VeeEss Eelectric

- 12.20 YC Electric