神経血管内コイルの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Neuroendovascular Coil Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755294

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

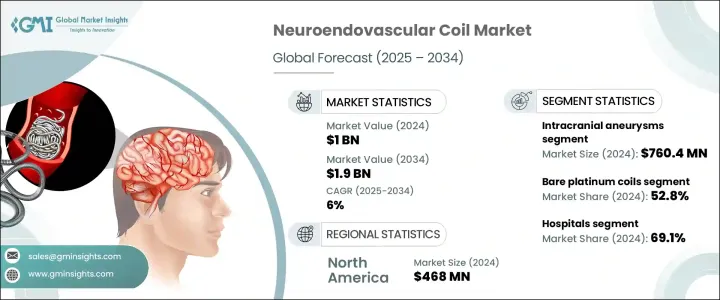

世界の神経血管内コイル市場は、2024年には10億米ドルと評価され、CAGR 6%で成長し、2034年には19億米ドルに達すると推定されています。

脳動脈瘤や虚血性脳卒中の有病率の増加は、高血圧、糖尿病、喫煙などの危険因子と相まって、神経血管内コイル需要を煽っています。高齢化も脳動脈瘤診断の増加に寄与しています。コイル材料、デザイン、送達システムの革新により、血管内治療がより安全、より正確、より効果的になっています。最近の技術の動向は、この治療法の急速な発展を反映して、いくつかの新しいコイリングシステムのFDA承認につながりました。

これらの新しいコイルは,より適合性が高く,着脱可能で,X線不透過性であるため,複雑な血管構造であっても動脈瘤の治療に適しています。血管内コイリングは従来型外科的アプローチに比べ、手技合併症のリスクが低いことが示されており、医師による採用が増加しています。低侵襲治療は、回復が早く、リスクが少なく、入院期間が短いため、医師と患者の両方からますます支持されています。米国心臓協会と米国脳卒中協会は、ほとんどのタイプの頭蓋内動脈瘤の初期治療に神経血管内コイリングを推奨しており、外科的クリッピング術に代わる重要な治療法となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 10億米ドル |

| 予測金額 | 19億米ドル |

| CAGR | 6% |

神経血管内コイル市場のベアプラチナコイルセグメントは、2024年に52.8%のシェアを占めます。ベアプラチナコイルは、頭蓋内動脈瘤の治療において臨床効果が実証されているため、広く使用されています。ベアプラチナコイルは一旦設置されると、経年変化しても長期間にわたって信頼性の高い動脈瘤閉塞効果を発揮します。このコイルの長年の臨床実績は合併症発生率を最小限に抑え、多くの症例に選択されています。その確立された信頼性は、先進国市場と市場の両方で需要を牽引し続けています。さらに、ベアプラチナコイルの価格帯は、コスト感覚が重要な要素であり、償還が必ずしも得られないヘルスケアシステムにおいて優位性を発揮します。

神経血管内コイル市場では病院が支配的なセグメントを占め、2024年のシェアは69.1%でした。世界中の病院では、動脈瘤コイリングなどの一刻を争う手技の需要増に対応するため、脳卒中や神経血管ケアのための専用ユニットを設置する動きが加速しています。こうした専門ユニットは、脳血管疾患の治療に不可欠な神経血管内治療用コイルの安定供給に大きく依存しています。神経学的ケアと脳卒中後の合併症予防に重点が置かれる中、先進的コイリング装置に対する需要は著しく高まっています。高所得国では、民間の保険業者や公的ヘルスケアシステムが、病院ベースの血管内治療に対して支援的な償還施策を提供しています。

米国の神経血管内コイル米国市場は2034年までに7億5,220万米ドルに達すると予想されています。米国には脳卒中センターと脳神経外科の広範なネットワークがあり、脳血管内治療が大量に行われています。このような強固なヘルスケアインフラが、神経血管内治療用コイルの普及を促進し、長期的な新技術の採用を支えています。こうしたヘルスケア施設の着実な成長と神経血管内治療技術の普及が、米国における市場拡大の主要因となっています。

世界の神経血管内コイル市場の主要企業は、Acandis、Allium Medical、Balt、Boston Scientific、Cardinal Health、Cook Medical、Kaneka、Medtronic、MicroPort、MicroVention、Penumbra、Rapid Medical、Shape Memory Medical、Stryker、Terumoなどです。神経血管内コイル市場での地位を固めるため、企業は複数の戦略に注力しています。特に安全性、精度、送達メカニズムの改善に重点を置いています。新しいコイル材料や設計を開発することで、メーカーは複雑な動脈瘤に対するより効果的な治療に対する需要の高まりに対応しています。各社はまた、特にヘルスケアインフラが急速に発展している地域において、病院や医療センターとの提携や協力を通じて地理的範囲を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 脳動脈瘤と脳卒中の発生率の増加

- コイル設計とデリバリーシステムにおける技術的進歩

- 高齢化人口の増加

- 画像誘導と血管内手術の採用増加

- 産業の潜在的リスク・課題

- 神経血管内手術とデバイスの高コスト

- 手術に伴う合併症と動脈瘤の再発のリスク

- 促進要因

- 成長可能性分析

- 技術

- 将来の市場動向

- 規制情勢

- 特許分析

- ポーター分析

- PESTEL分析

- 償還シナリオ

第4章 競合情勢

- イントロダクション

- 競争市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:タイプ別、2021~2034年

- 主要動向

- ベアプラチナコイル

- ハイドロゲルコーティングコイル

- その他

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 頭蓋内動脈瘤

- 動静脈奇形

- その他

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

- 学術研究機関

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Acandis

- Allium Medical

- Balt

- Boston Scientific

- Cardinal Health

- Cook Medical

- Kaneka

- Medtronic

- MicroPort

- MicroVention

- Penumbra

- Rapid Medical

- Shape Memory Medical

- Stryker

- Terumo

目次

The Global Neuroendovascular Coil Market was valued at USD 1 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 1.9 billion by 2034. The increasing prevalence of brain aneurysms and ischemic strokes, coupled with risk factors like hypertension, diabetes, and smoking, is fueling the demand for neuroendovascular coils. The aging population is also contributing to the rise in cerebral aneurysm diagnoses. Innovations in coil materials, designs, and delivery systems have made endovascular therapy safer, more accurate, and more effective. Recent advancements in technology have led to FDA approvals for several new coiling systems, which reflect the rapid development of this treatment method.

These new coils are more conformable, detachable, and radiopaque, making them suitable for treating aneurysms, even in complex vascular anatomies. Endovascular coiling has been shown to have a lower risk of procedural complications than traditional surgical approaches, contributing to its growing adoption by physicians. Minimally invasive treatments are increasingly favored by both doctors and patients because they involve quicker recovery times, fewer risks, and shorter hospital stays. The American Heart Association and American Stroke Association recommend neuroendovascular coiling for the initial treatment of most intracranial aneurysm types, making it an important alternative to surgical clipping.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1 Billion |

| Forecast Value | $1.9 Billion |

| CAGR | 6% |

The bare platinum coils segment in the neuroendovascular coil market held 52.8% share in 2024. These coils are widely used due to their proven clinical effectiveness in treating intracranial aneurysms. Once placed, bare platinum coils provide reliable aneurysm occlusion over time, even as they age. The long-standing clinical track record of these coils ensures minimal complication rates, making them the preferred choice for many cases. Their established reliability continues to drive demand in both developed and emerging markets. Additionally, the price point of bare platinum coils offers an advantage in healthcare systems where cost sensitivity is a significant factor, and reimbursement is not always available.

Hospitals represented the dominant segment in the neuroendovascular coil market, contributing a 69.1% share in 2024. Hospitals worldwide are increasingly setting up dedicated units for stroke and neurovascular care to meet the growing demand for time-sensitive procedures such as aneurysm coiling. These specialized units rely heavily on a steady supply of neuroendovascular coils, which are essential for treating cerebrovascular diseases. With the focus on neurological care and preventing complications after stroke, the demand for advanced coiling devices has risen significantly. In high-income nations, private insurance providers and public healthcare systems offer supportive reimbursement policies for hospital-based endovascular therapies.

U.S Neuroendovascular Coil Market is expected to reach 752.2 million by 2034. The country's extensive network of specialized stroke centers and neurosurgical departments facilitates a high volume of neuroendovascular procedures. This robust healthcare infrastructure promotes the widespread use of neuroendovascular coils and supports the adoption of new technologies over time. The steady growth of these healthcare facilities and the increasing uptake of neuroendovascular treatment technologies are key factors contributing to the market's expansion in the U.S.

Key players in the Global Neuroendovascular Coil Market include: Acandis, Allium Medical, Balt, Boston Scientific, Cardinal Health, Cook Medical, Kaneka, Medtronic, MicroPort, MicroVention, Penumbra, Rapid Medical, Shape Memory Medical, Stryker, Terumo. To solidify their position in the neuroendovascular coil market, companies are focusing on multiple strategies. These include heavy investments in research and development to introduce advanced coil technologies, with a particular focus on improving safety, precision, and delivery mechanisms. By developing new coil materials and designs, manufacturers are responding to the growing demand for more effective treatments for complex aneurysms. Companies are also expanding their geographic reach through partnerships and collaborations with hospitals and medical centers, particularly in regions where healthcare infrastructure is rapidly developing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of cerebral aneurysms and stroke

- 3.2.1.2 Technological advancements in coil design and delivery systems

- 3.2.1.3 Rising geriatric population

- 3.2.1.4 Growing adoption of image-guided and endovascular procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of neuroendovascular procedures and devices

- 3.2.2.2 Risk of procedure-related complications and recurrence of aneurysms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.7 Patent analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Reimbursement scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Bare platinum coils

- 5.3 Hydrogel-coated coils

- 5.4 Other types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Intracranial aneurysms

- 6.3 Arteriovenous malformation

- 6.4 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Academic and research institutes

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Acandis

- 9.2 Allium Medical

- 9.3 Balt

- 9.4 Boston Scientific

- 9.5 Cardinal Health

- 9.6 Cook Medical

- 9.7 Kaneka

- 9.8 Medtronic

- 9.9 MicroPort

- 9.10 MicroVention

- 9.11 Penumbra

- 9.12 Rapid Medical

- 9.13 Shape Memory Medical

- 9.14 Stryker

- 9.15 Terumo

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日