|

市場調査レポート

商品コード

1755285

モバイルロボットの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Mobile Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| モバイルロボットの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月19日

発行: Global Market Insights Inc.

ページ情報: 英文 192 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

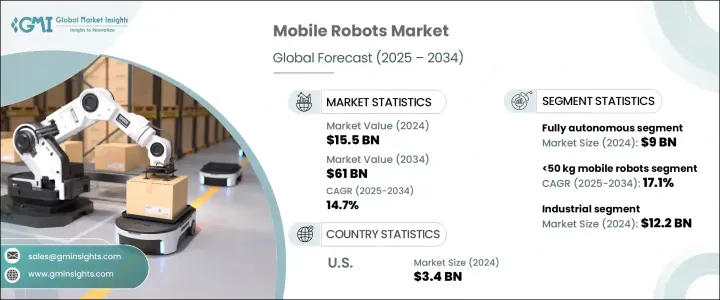

モバイルロボットの世界市場規模は、2024年には155億米ドルとなり、2034年にはCAGR 14.7%で成長し610億米ドルに達すると推定されています。

この不足は、反復作業、注文処理、マテリアルハンドリングの処理にロボットソリューションを採用する企業を後押ししています。トランプ政権時のロボット部品への関税賦課により、米国企業の製造コストの高騰を招き、中小企業(SME)における自律走行型モバイルロボット(AMR)や無人搬送車(AGV)の採用が遅れました。

その結果、メーカー各社はサプライチェーンを多様化し、生産を他地域にシフトし、生産活動を回復させました。長期的には、こうした戦略は、貿易リスクを軽減するための地域ハブを確立することで、サプライチェーンの強靭性を強化するのに役立ちました。モバイルロボットの採用は、新興経済諸国における最低賃金の上昇によってさらに後押しされ、ロボットソリューションの投資対効果を正当化しています。eコマースのような季節的に需要が急増する産業は、スケーラビリティのためにモバイルロボットに依存しており、特に労働力格差が懸念されている日本やドイツのような高齢化社会で見られる動向です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 155億米ドル |

| 予測金額 | 610億米ドル |

| CAGR | 14.7% |

完全自律型移動ロボットセグメントの2024年の市場規模は90億米ドルで、依然として支配的なセグメントです。AIと機械学習を活用したこれらのロボットは、人間の入力なしにリアルタイムで意思決定ができるため、倉庫や病院のようなダイナミック環境に最適です。先進的センサとSLAM(Simultaneous Localization and Mapping)技術を使って複雑な空間をナビゲートします。消灯倉庫として知られる完全自動化施設の台頭は、特にアジア太平洋と北米でAMRの採用を加速させました。しかし、人間のような器用さが要求される用途では課題が残っており、コンピュータビジョンや適応グリッパーなどの先端技術への投資が促進されています。

可搬重量50~500kgの市場セグメンテーションの2024年の市場規模は74億米ドルでした。これらのロボットは、倉庫でのマテリアルハンドリング、製造現場での重量部品の運搬、病院での大型機器の移動などに不可欠です。これらのロボットは、中距離の可搬重量を処理する汎用性があるため、小規模な作業に使用される軽量ロボットと、より産業的な規模の作業用に設計された重量ロボットをつなぐ重要な役割を担っています。オートメーションが産業セグメントで拡大し続ける中、このモバイルロボットのカテゴリーは、業務の合理化と効率化においてますます重要な役割を果たしています。

米国のモバイルロボット市場は、労働力不足、最低賃金の上昇、ロジスティクス、ヘルスケア、小売などのセグメントにおける自動化技術への関心の高まりが相まって、2024年には34億米ドルに達しました。人件費の高騰と業務効率化のニーズの高まりにより、産業はモバイルロボットを利用してサプライチェーンやマテリアルハンドリングプロセスを最適化しています。米国市場は、ロボット工学の技術革新を促進する政府の取り組みや施策からも恩恵を受けており、企業の生産性向上や人手への依存度の低減に役立っています。

世界のモバイルロボット産業における主要企業には、KUKA AG、ABB、Hikrobot Co.Ltd.、Teradyne Inc.、Geek+などがあります。市場ポジションを強化するため、モバイルロボット産業の企業はいくつかの戦略に注力しています。1つの重要なアプローチは、AI、機械学習、先進的センサなどの最先端技術をロボットソリューションに統合することで、製品ポートフォリオを拡大することです。また、貿易リスクを軽減し、国際的なサプライチェーンへの依存を減らすために、製造業務の現地化を進める企業も増えています。さらに、ロジスティクス、eコマース、製造の各産業リーダーと提携し、特定の産業のニーズに合わせてロボットをカスタマイズする企業も多いです。研究開発への投資も不可欠な戦略であり、企業は自律的なナビゲーション、器用さ、人間とロボットの相互作用における革新によって、常に時代の先端を行くことができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 産業への影響

- 供給側の影響

- 価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側への影響

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な産業対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 施策関与

- 展望と今後の検討事項

- 貿易への影響

- 産業への影響要因

- 促進要因

- 労働力不足と労働コストの上昇

- eコマースの成長と倉庫の自動化

- AIとセンサ技術の進歩

- 規制支援とインダストリー4.0の取り組み

- 産業の潜在的リスク・課題

- 初期投資コストが高め

- 熟練したオペレーターの不足

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:自動化レベル別、2021~2034年

- 主要動向

- 完全自律型

- 半自律型

- 手動型(遠隔操作車両)

第6章 市場推定・予測:積載量別、2021~2034年

- 主要動向

- 50 kg以下

- 50~500 kg

- 500~1,000 kg

- 1,000 kg以上

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 住宅/家庭用

- 商業施設

- 産業

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- ABB

- KUKA AG

- Boston Dynamics

- OMRON Corporation

- Yaskawa America, Inc.

- Universal Robots A/S

- Seiko Epson Corporation

- FANUC America Corporation

- Teradyne Inc.

- Geek+

- Hikrobot Co., Ltd.

- Locus Robotics

- Ocado Group plc.

- Rockwell Automation, Inc.

- Vecna Robotics

- Agility Robotics

The Global Mobile Robots Market was valued at USD 15.5 billion in 2024 and is estimated to grow at a CAGR of 14.7% to reach USD 61 billion by 2034, driven by the global shortage of skilled labor, especially in manufacturing and logistics. This shortage encourages businesses to adopt robotic solutions for handling repetitive tasks, order fulfillment, and material handling. The imposition of tariffs on robotic components during the Trump administration led to a spike in manufacturing costs for U.S. companies, which slowed the adoption of autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) in small and medium-sized enterprises (SMEs).

As a result, manufacturers diversified their supply chains, shifted production to other regions, and restored manufacturing activities. In the long run, these strategies helped strengthen supply chain resilience by establishing regional hubs to mitigate trade risks. The adoption of mobile robots is further bolstered by rising minimum wages in developed economies, justifying the return on investment for robotic solutions. Industries like e-commerce, which experience seasonal demand surges, rely on mobile robots for scalability, a trend seen particularly in aging societies like Japan and Germany, where the labor gap is a growing concern.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.5 Billion |

| Forecast Value | $61 Billion |

| CAGR | 14.7% |

The fully autonomous mobile robot segment was valued at USD 9 billion in 2024 and remains a dominant segment. These robots, which leverage AI and machine learning, can make real-time decisions without human input, making them ideal for dynamic environments like warehouses and hospitals. They navigate complex spaces using advanced sensors and SLAM (Simultaneous Localization and Mapping) technology. The rise of fully automated facilities, known as lights-out warehouses, accelerated the adoption of AMRs, particularly in Asia-Pacific and North America. However, challenges remain in applications requiring human-like dexterity, driving investments in advanced technologies like computer vision and adaptive grippers.

The mobile robots market with a payload capacity of 50-500 kg segment was valued at USD 7.4 billion in 2024, reflecting their widespread application in various industries. These robots are essential for material handling in warehouses, facilitating the transport of heavy components in manufacturing environments, and moving large equipment in hospitals. The versatility of these robots in handling mid-range payloads makes them a critical link between lightweight robots used for smaller tasks and heavy-duty robots designed for more industrial-scale operations. As automation continues to expand in industrial sectors, this category of mobile robots is playing an increasingly vital role in streamlining operations and improving efficiency.

United States Mobile Robot Market reached USD 3.4 billion in 2024, driven by a combination of labor shortages, rising minimum wages, and growing interest in automation technologies across sectors such as logistics, healthcare, and retail. With high labor costs and an increasing need for operational efficiency, industries use mobile robots to optimize their supply chain and material handling processes. The U.S. market has also benefited from government initiatives and policies that foster innovation in robotics, helping companies improve productivity and reduce reliance on human labor.

Some leading players in the Global Mobile Robots Industry include KUKA AG, ABB, Hikrobot Co., Ltd., Teradyne Inc., and Geek+. To strengthen their market position, companies in the mobile robots industry are focusing on several strategies. One key approach is expanding their product portfolio by integrating cutting-edge technologies such as AI, machine learning, and advanced sensors into their robotic solutions. Companies are also increasingly localizing their manufacturing operations to mitigate trade risks and reduce reliance on international supply chains. Additionally, many partners with industry leaders in logistics, e-commerce, and manufacturing to tailor their robots to specific industry needs. Investment in R&D is another essential strategy, enabling companies to stay ahead of the curve with innovations in autonomous navigation, dexterity, and human-robot interaction.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Labor shortages and rising workforce costs

- 3.3.1.2 E-commerce growth and warehouse automation

- 3.3.1.3 Advancements in AI and sensor technologies

- 3.3.1.4 Regulatory support and industry 4.0 initiatives

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial investment costs

- 3.3.2.2 Lack of skilled operators

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Automation Level, 2021 - 2034 (USD Billion & Thousand Units)

- 5.1 Key trends

- 5.2 Fully autonomous

- 5.3 Semi-autonomous

- 5.4 Manual (remotely operated vehicle)

Chapter 6 Market Estimates & Forecast, By Payload Capacity, 2021 - 2034 (USD Billion & Thousand Units)

- 6.1 Key trends

- 6.2 <50 kg

- 6.3 50–500 kg

- 6.4 500–1000 kg

- 6.5 >1000 kg

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion & Thousand Units)

- 7.1 Key trends

- 7.2 Residential/domestic

- 7.3 Commercial places

- 7.4 Industrial

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion & Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 KUKA AG

- 9.3 Boston Dynamics

- 9.4 OMRON Corporation

- 9.5 Yaskawa America, Inc.

- 9.6 Universal Robots A/S

- 9.7 Seiko Epson Corporation

- 9.8 FANUC America Corporation

- 9.9 Teradyne Inc.

- 9.10 Geek+

- 9.11 Hikrobot Co., Ltd.

- 9.12 Locus Robotics

- 9.13 Ocado Group plc.

- 9.14 Rockwell Automation, Inc.

- 9.15 Vecna Robotics

- 9.16 Agility Robotics