AIおよび機械学習運用化ソフトウェア市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

AI and Machine Learning Operationalization Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755267

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

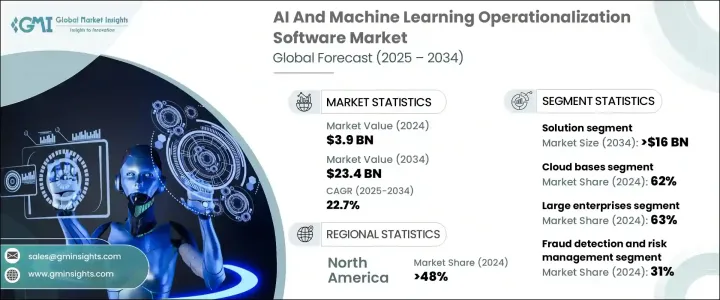

AIおよび機械学習運用化ソフトウェアの世界市場規模は、2024年に39億米ドルとなり、データ主導の意思決定に対する需要の高まりと、企業全体におけるスケーラブルで自動化されたモデル展開に対するニーズの高まりに後押しされ、CAGR 22.7%で成長し、2034年には234億米ドルに達すると推定されます。

特に製造、金融、ヘルスケア、eコマースなどの分野では、AIワークフローの合理化、業務上の摩擦の低減、法規制遵守の徹底、イノベーションの加速のために、企業はこれらのソリューションを急速に導入しています。

人工知能と機械学習アプリケーションが中核業務に不可欠になるにつれ、企業はモデルをリアルタイムで展開、監視、保守するための堅牢なプラットフォームを求めるようになっています。手作業によるモデル管理が非効率であることから、AIを大規模にライフサイクル全般にわたってサポートし、業務全体にわたって一貫した精度とスピードを確保するプラットフォームが市場を牽引しています。企業は、進化し続ける運用環境の中で一貫性、回復力、柔軟性を維持するプラットフォームを求めています。機械学習の複雑なワークフローを簡素化し、実験から本格的な実装へと効率的に移行できるツールへのシフトは明らかです。企業は今、技術的なハードルを抽象化し、データ取り込み、フィーチャーエンジニアリング、モデル検証、導入後のモニタリングなどのプロセスを合理化するプラットフォームを求めています。この移行により、大規模なデータサイエンスチームへの依存度が低下し、アナリストからITチームまで、部門横断的なユーザーがAIイニシアチブで協力できるようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 39億米ドル |

| 予測金額 | 234億米ドル |

| CAGR | 22.7% |

2024年のソリューション部門の売上高は23億米ドルで、2034年には160億米ドルに達します。この勢いは、データ準備からリアルタイムのモデルモニタリングまですべてを合理化するフルサイクルAIソフトウェアへの依存が高まっていることを裏付けています。企業は、特に社内のデータサイエンスの専門知識が限られている環境において、展開のタイムラインを加速し、価値をより迅速に推進するために、これらのソリューションに注目しています。自動化とスケーラビリティを提供するこれらのプラットフォームは、財務、オペレーション、マーケティング、カスタマーエクスペリエンスなどの事業部門にとって不可欠なものとなりつつあります。

クラウドベースの展開セグメントは、その適応性、費用対効果、既存のデジタル・エコシステムとのシームレスな統合が原動力となり、2024年には62%のシェアを占める。クラウドインフラストラクチャにより、企業はモデルのバージョン管理、ガバナンス、コラボレーションのようなAI機能を分散したチーム内で一元化・調整することができ、一貫したパフォーマンスと反復サイクルの高速化を実現できます。AIへのアクセスを民主化する役割を担うクラウドは、多様なビジネス環境におけるオペレーションの拡張に適した選択肢となっています。

北米AIおよび機械学習運用化ソフトウェア市場は、成熟したAI実装、強固なクラウド導入、AI研究開発への継続的な投資によって強化され、2024年には48%のシェアを占める。米国では、規制コンプライアンス、業務の透明性、競争上の俊敏性への関心が高まっており、企業は企業規模でのAIの運用に多額の投資を行うようになっています。

DataRobot、Google Cloud、IBM、H2O.ai、Microsoft、SAS Institute、Amazon Web Services(AWS)、Dataiku、Databricks、C3.ai。大手企業は、プラットフォームの統合、ユーザーインターフェースの改善、クラウドネイティブの機能に多額の投資を行っています。多くの企業は、モデルのトレーニング、デプロイメント、ガバナンス、モニタリングに至るフルライフサイクルのAIサポートを提供する統合環境の構築に注力しています。さらに、企業はクラウドプロバイダーやエンタープライズソフトウェアベンダーと戦略的提携を結び、サービス提供範囲の拡大と機能強化を図っています。自動化されたMLOps機能、ノーコード/ローコード環境、あらかじめ構築されたAIワークフローへの投資により、技術者以外のチームにも広く採用されるようになっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- 製造業者

- 部品サプライヤー

- テクノロジープロバイダー

- サービスプロバイダー

- 最終用途

- 利益率分析

- テクノロジーとイノベーションの情勢

- 主なニュースと取り組み

- 特許分析

- 規制情勢

- 影響要因

- 促進要因

- 業界全体でAI/MLの導入が増加

- スケーラブルで自動化されたMLワークフローの必要性

- クラウドネイティブAIソリューションの台頭

- AI投資からビジネス価値を生み出すプレッシャー

- 業界の潜在的リスク&課題

- モデルの透明性と説明可能性の欠如

- 既存のインフラストラクチャとの統合の複雑さ

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソフトウェア

- モデル開発およびトレーニングソフトウェア

- モデル展開ソフトウェア

- モデル監視および管理ソフトウェア

- データ管理ソフトウェア

- サービス

- 専門サービス

- マネージドサービス

第6章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- オンプレミス

- クラウドベース

第7章 市場推計・予測:組織規模別、2021年~2034年

- 主要動向

- 中小企業

- 大企業

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 予測分析

- 不正行為の検出とリスク管理

- 顧客体験管理

- 自然言語処理(NLP)とテキスト分析

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 銀行、金融サービス、保険(BFSI)

- ヘルスケアとライフサイエンス

- 小売業とeコマース

- ITおよび通信

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Alteryx

- Amazon Web Services(AWS)

- Aporia

- C3.ai

- Cloudera

- Databricks

- Dataiku

- DataRobot

- Domino Data Lab

- Google Cloud

- H2O.ai

- IBM Watson

- Infosys Nia

- Microsoft Azure

- Oracle

- Palantir Technologies

- Qlik

- RapidMiner

- SAS Institute

- Seldon

目次

The Global AI and Machine Learning Operationalization Software Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 22.7% to reach USD 23.4 billion by 2034, propelled by increasing demand for data-driven decision-making and the growing need for scalable, automated model deployment across enterprises. Organizations are rapidly adopting these solutions to streamline AI workflows, reduce operational friction, ensure regulatory compliance, and accelerate innovation-especially within sectors like manufacturing, finance, healthcare, and e-commerce.

As artificial intelligence and machine learning applications become integral to core business operations, companies seek robust platforms to deploy, monitor, and maintain models in real-time. The inefficiency of manual model management is driving the market toward platforms that offer full lifecycle support for AI at scale, ensuring consistent accuracy and speed across operations. Enterprises seek platforms that maintain consistency, resilience, and flexibility across evolving operational landscapes. There's a clear shift toward tools that simplify the complexities of machine learning workflows, allowing organizations to move from experimentation to full-scale implementation efficiently. Businesses are now seeking platforms that abstract technical hurdles and streamline processes such as data ingestion, feature engineering, model validation, and post-deployment monitoring. This transition is reducing reliance on large data science teams and empowering cross-functional users-from analysts to IT teams-to collaborate on AI initiatives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $23.4 Billion |

| CAGR | 22.7% |

In 2024, the solutions segment generated USD 2.3 billion and will reach USD 16 billion by 2034. This momentum underscores the increasing reliance on full-cycle AI software that streamlines everything from data preparation to real-time model monitoring. Enterprises are turning to these solutions to accelerate deployment timelines and drive value faster, particularly in environments where in-house data science expertise is limited. By offering automation and scalability, these platforms are becoming essential for business units across finance, operations, marketing, and customer experience.

Cloud-based deployment segment held a 62% share in 2024, driven by its adaptability, cost-effectiveness, and seamless integration with existing digital ecosystems. Cloud infrastructure allows enterprises to centralize and coordinate AI functions-like model versioning, governance, and collaboration-within distributed teams, ensuring consistent performance and faster iteration cycles. Its role in democratizing AI access has made it the preferred choice for scaling operations across diverse business environments.

North America AI and Machine Learning Operationalization Software Market held a 48% share in 2024, bolstered by mature AI implementation, robust cloud adoption, and continuous investment in AI R&D. In the U.S., heightened focus on regulatory compliance, operational transparency, and competitive agility is prompting companies to invest heavily in operationalizing AI at enterprise scale.

DataRobot, Google Cloud, IBM, H2O.ai, Microsoft, SAS Institute, Amazon Web Services (AWS), Dataiku, Databricks, C3.ai. Leading firms invest heavily in platform integration, user interface improvements, and cloud-native functionality. Many focus on building unified environments that offer full-lifecycle AI support-spanning model training, deployment, governance, and monitoring. Additionally, companies are forming strategic alliances with cloud providers and enterprise software vendors to expand reach and enhance functionality. Investments in automated MLOps capabilities, no-code/low-code environments, and prebuilt AI workflows enable wider adoption across non-technical teams.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.3.1 Manufacturers

- 3.3.2 Component suppliers

- 3.3.3 Technology providers

- 3.3.4 Service providers

- 3.3.5 End use

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing adoption of ai/ml across industries

- 3.9.1.2 Need for scalable and automated ml workflows

- 3.9.1.3 Rise of cloud-native ai solutions

- 3.9.1.4 Pressure to generate business value from ai investments

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Lack of model transparency and explainability

- 3.9.2.2 Integration complexity with existing infrastructure

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.2.1 Model development and training software

- 5.2.2 Model deployment software

- 5.2.3 Model monitoring and management software

- 5.2.4 Data management software

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud based

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Small and medium enterprises (SMEs)

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Predictive analytics

- 8.3 Fraud detection and risk management

- 8.4 Customer experience management

- 8.5 Natural language processing (NLP) and text analytics

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Banking, financial services, and insurance (BFSI)

- 9.3 Healthcare and life sciences

- 9.4 Retail and e-commerce

- 9.5 IT and telecommunications

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Alteryx

- 11.2 Amazon Web Services (AWS)

- 11.3 Aporia

- 11.4 C3.ai

- 11.5 Cloudera

- 11.6 Databricks

- 11.7 Dataiku

- 11.8 DataRobot

- 11.9 Domino Data Lab

- 11.10 Google Cloud

- 11.11 H2O.ai

- 11.12 IBM Watson

- 11.13 Infosys Nia

- 11.14 Microsoft Azure

- 11.15 Oracle

- 11.16 Palantir Technologies

- 11.17 Qlik

- 11.18 RapidMiner

- 11.19 SAS Institute

- 11.20 Seldon

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日