|

市場調査レポート

商品コード

1755263

高圧ラミネートおよびプラスチック樹脂市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測High Pressure Laminates and Plastic Resins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 高圧ラミネートおよびプラスチック樹脂市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年05月29日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

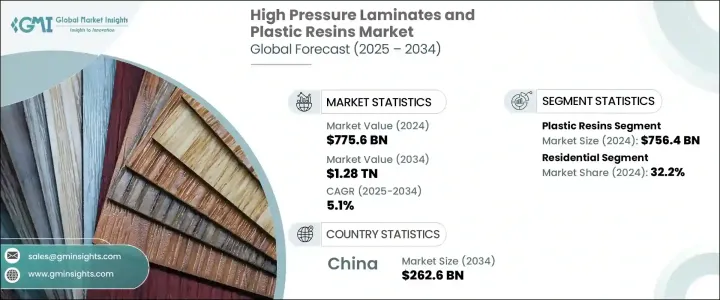

高圧ラミネートおよびプラスチック樹脂の世界市場規模は、2024年に7,756億米ドルとなり、CAGR 5.1%で成長し、2034年には1兆2,800億米ドルに達すると予測されています。

市場の勢いは、特に建設用付属品、消費者向けパッケージング、工業製品、モビリティソリューションなど、複数の部門にわたる広範な用途によって牽引されています。軽量でコスト効率に優れ、強度の高い素材に対する需要の高まりが、高圧ラミネート(HPL)とプラスチック樹脂の成長を後押しし続けており、市場シェアでは樹脂がリードしています。プラスチック樹脂は、その加工性、耐久性、汎用性から、広範な商品にとって不可欠な原材料であり続けているため、当面は世界マーケットプレースでの優位性を維持すると予想されます。

HPLは市場シェアこそ小さいもの、インテリアデザインや建築用途での採用が増加しているため、牽引力を増しています。弾力性とデザインの柔軟性で知られるHPL材料は、住宅や商業施設において頻繁に好まれています。デザインの動向は、視覚的な魅力だけでなく、最小限の手入れで済む表面へとシフトしており、ラミネートへの関心を高めています。機能と美観を兼ね備えた素材への需要が高まるにつれ、HPLはより強力なセグメントとなりつつあります。一方、プラスチック樹脂はコスト効率が高く、大量生産に適しているため、依然として大量に流通しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 7,756億米ドル |

| 予測金額 | 1兆2,800億米ドル |

| CAGR | 5.1% |

新興経済諸国と先進経済諸国を問わず、都市開発とインフラの近代化が進み、市場の成長がさらに加速しています。産業界は、構造的価値だけでなく、持続可能性も実現する先端材料を求めています。設計の嗜好は、低メンテナンス性、耐候性、軽量性など、ラミネートとプラスチック樹脂の両方がもたらす特性を備えた設計製品へと着実に移行しています。このように、進化するデザインと実用性の要件を満たす素材に対する一貫した需要は、規模は異なるもの、両分野の継続的な関連性を保証しています。

製品タイプ別に見ると、市場は高圧ラミネート(HPL)、連続圧ラミネート(CPL)、プラスチック樹脂に区分されます。なかでもプラスチック樹脂が大きな市場シェアを占め、2024年の売上高は7,564億米ドルを記録しました。この分野は予測期間を通じてCAGR 5.1%で拡大すると予想されます。プラスチック樹脂の主な利点は、経済的な生産価値、加工のしやすさ、幅広い材料の多様性を提供し、複数の産業で基礎部品として機能する能力にあります。包装から電子機器に至るまで、構造的および非構造的用途におけるその性能は、主導的地位を強化しています。

材料の革新がこの市場の将来を形成しています。先進的な樹脂化学とリサイクル可能なポリマーを通じて環境性能を向上させようとする努力は、メーカー各社の事業のあり方を変えつつあります。長期的な持続可能性目標をサポートする、高性能で環境に配慮した材料を製造する方向へのシフトが顕著になっています。リサイクル可能なプラスチックやバイオベースプラスチックの採用は徐々に増加しており、環境コンプライアンスや各分野のグリーン・イニシアティブと歩調を合わせています。

最終用途産業別に分析すると、市場は住宅、商業、ヘルスケア、輸送、工業、その他に分類されます。現在、商業分野が最も高い市場シェアを占めているが、これは主に公共インフラ、企業オフィス、小売チェーン、その他人通りの多い商業環境でプラスチック樹脂とHPLの両方が一貫して使用されているためです。2024年には、住宅分野が市場全体の約32.2%を占める。現代住宅におけるデザイン意識の高まりと、耐久性があり清掃が容易な表面へのニーズが、住宅用途におけるHPLの使用を引き続き刺激しています。一方、プラスチック樹脂は、住宅と商業施設の両方で、インテリア、装飾、安全用途など幅広い用途を支配しています。

中国は、この市場の世界の軌道を形成する上で極めて重要な役割を果たしています。2024年の中国市場の売上高は1,564億米ドルで、2034年には2,626億米ドルに達し、CAGR 5.3%で成長する見込みです。中国の広範な製造基盤は、エンドユーザー産業における国内消費の増加と相まって、世界の生産と需要の最前線に位置しています。都市開発、インフラの拡大、消費者のアップグレードの急増は、国内でのラミネートと樹脂の使用量増加に寄与しています。

高圧ラミネートおよびプラスチック樹脂市場の競合情勢は、上位5社が世界シェアの30%以上を占めており、緩やかに統合されています。プラスチック樹脂の分野では、生産量の拡張性、世界な物流能力、多目的製品ラインを重視するメーカーの影響が大きいです。これらの企業は、持続可能な材料の革新、積極的な研究開発プログラム、迅速な生産モデルを通じて競争力を維持しています。ラミネートの分野では、強力なブランド・アイデンティティ、幅広い製品バリエーション、広範な販売網を持つ企業が引き続き高い業績を上げています。持続可能性、革新性、効率的な価格設定は、各社が消費者の信頼を築き、各地域で進化する法規制の要求に応えようと努力する中で、依然として中心的な戦略となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向s

- 地域別

- 製品タイプ別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 高圧ラミネート(HPL)

- 水平勾配

- 垂直勾配

- ポストフォームグレード

- 特殊用途グレード

- コンパクトグレード

- 常用加圧ラミネート(CPL)

- プラスチック樹脂

- フェノール樹脂

- メラミン樹脂

- エポキシ樹脂

- ポリエステル樹脂

- その他

第6章 市場推計・予測:原材料別、2021年~2034年

- 主要動向

- クラフト紙

- 装飾紙

- オーバーレイペーパー

- 熱硬化性樹脂

- フェノール樹脂

- メラミン樹脂

- 熱可塑性樹脂

- ポリエチレン(PE)

- ポリプロピレン(PP)

- ポリ塩化ビニル(PVC)

- ポリスチレン(PS)

- その他

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 家具とキャビネット

- 住宅家具

- 業務用家具

- キッチンキャビネット

- オフィス家具

- フローリング

- 住宅フローリング

- 商業用フローリング

- 壁パネルとパーティション

- カウンタートップとワークトップ

- キッチンカウンター

- 実験室のカウンタートップ

- 業務用ワークトップ

- ドア

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 住宅用

- 商業用

- オフィス

- 小売り

- ホスピタリティ

- 教育

- ヘルスケア

- 病院

- 研究所

- クリニック

- 輸送機関

- 自動車

- 海洋

- 航空

- 産業

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Abet Laminati S.p.A.

- Arkema Group

- Arpa Industriale S.p.A.

- BASF SE

- Century Plyboards(India)Ltd.

- Changzhou Zhenghang Decorative Materials Co., Ltd.

- Changzhou Zhongtian Fireproof Decorative Sheets Co., Ltd.

- Covestro AG

- Dow Chemical Company

- DuPont de Nemours, Inc.

- Fletcher Building Limited

- Formica Group(Fletcher Building)

- Greenlam Industries Ltd.

- Jiangsu TRSK New Material Co., Ltd.

- Kingboard Laminates Holdings Ltd.

- LyondellBasell Industries N.V.

- Merino Industries Ltd.

- SABIC

- Solera International

- Wilsonart International Inc.

The Global High Pressure Laminates and Plastic Resins Market was valued at USD 775.6 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 1.28 trillion by 2034. Market momentum is being driven by widespread application across multiple sectors, especially in construction accessories, consumer packaging, industrial goods, and mobility solutions. The growing demand for lightweight, cost-efficient, and high-strength materials continues to fuel growth in both high-pressure laminates (HPL) and plastic resins, with resins leading the way in terms of market share. As plastic resins remain essential raw materials for a wide spectrum of goods due to their processability, durability, and versatility, they are expected to maintain their dominance in the global marketplace for the foreseeable future.

HPL, although smaller in market share, is gaining traction due to its increasing adoption in interior design and architectural applications. Known for their resilience and design flexibility, HPL materials are frequently preferred in residential and commercial installations. Trends in design are shifting towards surfaces that offer not only visual appeal but also require minimal upkeep, boosting interest in laminates. As demand grows for materials that combine function with aesthetics, HPL is becoming a stronger segment. Meanwhile, plastic resins remain in high-volume circulation due to their cost-efficient nature and adaptability in mass manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $775.6 Billion |

| Forecast Value | $1.28 Trillion |

| CAGR | 5.1% |

Increased urban development and modernization of infrastructure across emerging and developed economies alike are further accelerating market growth. Industries seek advanced materials that deliver not just structural value but also sustainability. Design preferences are steadily moving toward engineered products that offer low maintenance, weather resistance, and lightweight performance-all attributes that both laminates and plastic resins bring to the table. This consistent demand for materials that fulfill evolving design and utility requirements ensures continued relevance for both segments, although at different scales.

By product type, the market is segmented into high pressure laminates (HPL), continuous-pressure laminates (CPL), and plastic resins. Among these, plastic resins accounted for a significant market share, with a recorded revenue of USD 756.4 billion in 2024. This segment is expected to expand at a CAGR of 5.1% throughout the forecast period. The key advantage of plastic resins lies in their ability to serve as foundational components across multiple industries, offering economic production value, ease of fabrication, and broad material diversity. Their performance in structural and non-structural applications-ranging from packaging to electronics-reinforces their leadership position.

Material innovation is shaping the future of this market. Efforts to improve environmental performance through advanced resin chemistry and recyclable polymers are reshaping how manufacturers operate. There is a noticeable shift toward producing high-performance, eco-conscious materials that support long-term sustainability goals. The adoption of recyclable and bio-based plastics is gradually rising, aligning with environmental compliance and green initiatives across sectors.

When analyzed by end-use industry, the market is classified into residential, commercial, healthcare, transportation, industrial, and others. The commercial segment currently commands the highest market share, largely due to the consistent use of both plastic resins and HPLs in public infrastructure, corporate offices, retail chains, and other high-traffic commercial environments. In 2024, the residential sector accounted for approximately 32.2% of the overall market. Increasing design consciousness and the need for durable, easy-to-clean surfaces in modern homes continue to stimulate HPL usage in residential applications. Plastic resins, on the other hand, dominate a wide array of uses across interiors, decor, and safety applications in both residential and commercial properties.

China plays a pivotal role in shaping the global trajectory of this market. In 2024, the Chinese market generated revenue of USD 156.4 billion and is on track to reach USD 262.6 billion by 2034, growing at a CAGR of 5.3%. China's extensive manufacturing base, combined with rising domestic consumption in end-user industries, places it at the forefront of global production and demand. The surge in urban development, infrastructure expansion, and consumer upgrades contributes to increased usage of both laminates and resins within the country.

The competitive landscape of the high-pressure laminates and plastic resins market is moderately consolidated, with the top five companies controlling over 30% of the global share. The plastic resins space is highly influenced by producers focused on volume scalability, global logistics capabilities, and multipurpose product lines. These players maintain their competitive edge through innovations in sustainable materials, aggressive R&D programs, and responsive production models. On the laminates side, companies with a strong brand identity, wide product variety, and expansive distribution continue to outperform. Sustainability, innovation, and efficient pricing remain core strategies as companies work to build consumer trust and meet evolving regulatory demands across regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Raw material

- 2.2.4 Application

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.1.1 High pressure laminates (HPL)

- 5.1.2 Horizontal grade

- 5.1.3 Vertical grade

- 5.1.4 Postforming grade

- 5.1.5 Special purpose grade

- 5.1.6 Compact grade

- 5.2 Continuous pressure laminates (CPL)

- 5.3 Plastic resins

- 5.3.1 Phenolic resins

- 5.3.2 Melamine resins

- 5.3.3 Epoxy resins

- 5.3.4 Polyester resins

- 5.3.5 Others

Chapter 6 Market Estimates and Forecast, By Raw Material, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Kraft paper

- 6.3 Decorative paper

- 6.4 Overlay papers

- 6.5 Thermosetting resins

- 6.5.1 Phenolic resins

- 6.5.2 Melamine resins

- 6.6 Thermoplastic resins

- 6.6.1 Polyethylene (PE)

- 6.6.2 Polypropylene (PP)

- 6.6.3 Polyvinyl chloride (PVC)

- 6.6.4 Polystyrene (PS)

- 6.6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Furniture & cabinetry

- 7.2.1 Residential furniture

- 7.2.2 Commercial furniture

- 7.2.3 Kitchen cabinets

- 7.2.4 Office furniture

- 7.3 Flooring

- 7.3.1 Residential flooring

- 7.3.2 Commercial flooring

- 7.4 Wall panels & partitions

- 7.5 Countertops & worktops

- 7.5.1 Kitchen countertops

- 7.5.2 Laboratory countertops

- 7.5.3 Commercial worktops

- 7.6 Doors

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Offices

- 8.3.2 Retail

- 8.3.3 Hospitality

- 8.3.4 Education

- 8.4 Healthcare

- 8.4.1 Hospitals

- 8.4.2 Laboratories

- 8.4.3 Clinics

- 8.5 Transportation

- 8.5.1 Automotive

- 8.5.2 Marine

- 8.5.3 Aviation

- 8.6 Industrial

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abet Laminati S.p.A.

- 10.2 Arkema Group

- 10.3 Arpa Industriale S.p.A.

- 10.4 BASF SE

- 10.5 Century Plyboards (India) Ltd.

- 10.6 Changzhou Zhenghang Decorative Materials Co., Ltd.

- 10.7 Changzhou Zhongtian Fireproof Decorative Sheets Co., Ltd.

- 10.8 Covestro AG

- 10.9 Dow Chemical Company

- 10.10 DuPont de Nemours, Inc.

- 10.11 Fletcher Building Limited

- 10.12 Formica Group (Fletcher Building)

- 10.13 Greenlam Industries Ltd.

- 10.14 Jiangsu TRSK New Material Co., Ltd.

- 10.15 Kingboard Laminates Holdings Ltd.

- 10.16 LyondellBasell Industries N.V.

- 10.17 Merino Industries Ltd.

- 10.18 SABIC

- 10.19 Solera International

- 10.20 Wilsonart International Inc.