|

市場調査レポート

商品コード

1755261

がん治療施設市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Cancer Treatment Facilities Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| がん治療施設市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年05月26日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

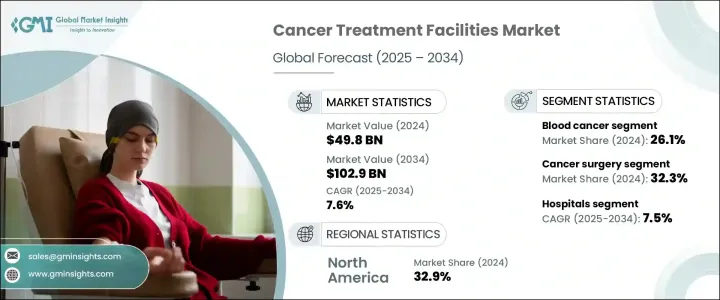

世界のがん治療施設市場は、2024年に498億米ドルと評価され、CAGR 7.6%で成長し、2034年には1,029億米ドルに達すると推定されています。

がん治療センターは、様々な種類のがんの診断、治療、継続的な管理に焦点を当てた専門ヘルスケア機関です。これらの治療センターは通常、化学療法、放射線療法、免疫療法、外科治療、アフターケアなどのサービスを提供しています。がん専門医、外科医、放射線科医、看護スタッフなどの専門家からなる集学的チームを雇用し、患者一人ひとりに合ったケアを提供しています。

世界のがん罹患率の上昇が、この市場の主な促進要因です。人口の高齢化はがんの診断件数の増加に大きく寄与しており、その結果、専門的ながん治療に対する需要が高まっています。こうしたニーズに応えるため、治療施設はインフラを強化し、精密腫瘍学や集学的治療モデルなどの先進技術を導入しています。こうした技術革新は、特にがんにかかりやすい高齢者層の増加に対応することを目的としています。さらに、医療ツーリズムはがん治療市場の拡大に寄与しており、特に手ごろな価格の治療オプションが、低コストで質の高い治療を求める外国人患者を惹きつけている地域で顕著です。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 498億米ドル |

| 予測金額 | 1,029億米ドル |

| CAGR | 7.6% |

血液がん分野は、2024年に26.1%の最大シェアを占めました。この成長の原動力は、継続的な臨床需要と、専門治療施設を含む血液がん治療に必要な広範なインフラです。さらに、化学療法、骨髄移植、免疫療法を含む、複雑で費用がかかり、しばしば集中的な治療プロトコールが、市場拡大に大きく寄与しています。さらに、長期にわたる経過観察、集学的医療チームの関与、高度な診断能力の必要性などが、他のがん種に特化した治療センターよりもこうした専門治療センターの重要性をさらに強調しています。

2024年には、病院部門が67.5%のシェアを占めて最大の市場シェアを占め、今後もCAGR 7.5%で成長すると予想されます。病院におけるがん治療施設の需要は、高度な検出ツールの利用可能性と、化学療法、放射線療法、ホルモン療法を含む幅広い治療選択肢によって牽引されています。患者は、総合的なサービスや集学的ケアチームへのアクセスを提供する病院を好みます。

米国のがん治療市場は2024年に149億米ドルと評価され、高齢化とがん患者の増加により継続的な成長が見込まれています。このため、ロボット手術、免疫療法、精密医療などの最先端治療を提供する総合がんセンターの開発が進んでいます。HCAヘルスケアなど業界の大手企業は、パートナーシップを結び、AI技術を取り入れることで、その勢力を拡大しています。政府のイニシアチブとバリューベースのケアモデルは、市場の成長をさらに促進します。

世界のがん治療施設市場の主要企業には、Alliance HealthCare Services、American Oncology Institute、Apollo Hospitals Enterprise、Cancer Treatment Centers of America、Compass Oncology、Curie Oncology、Fortis Healthcare、GenesisCare、HCA Healthcare、Healthcare Global Enterprises、IHH Healthcare Berhad、Narayana Hrudayalaya、OncoLife Hospitals、Ramsay Health Care、Tenet Healthcareなどがあります。市場ポジションを強化するため、がん治療施設セクターの企業はAI、ロボット手術、精密医療などの先端技術の統合に注力しています。また、他のヘルスケアプロバイダーや組織との戦略的提携を通じてサービスを拡大しています。価値に基づくケアモデルの採用が進むことで、コストを削減しながら患者の転帰を改善することができます。多くの組織が、診断から治療後のケアまで包括的なサービスを提供する統合がん医療センターを建設しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- がん罹患率の上昇

- 高齢化人口の増加

- 医療ツーリズムの増加

- 政府の取り組みと啓発プログラムの増加

- 業界の潜在的リスク&課題

- 熟練した腫瘍学従事者の不足

- 高度な治療と技術の高コスト

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

- 償還シナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:治療タイプ別、2021年~2034年

- 主要動向

- がん手術

- 化学療法

- 放射線治療

- 免疫療法

- 骨髄移植

- その他の治療の種類

第6章 市場推計・予測:がんタイプ別、2021年~2034年

- 主要動向

- 血液がん

- 乳がん

- 前立腺がん

- 消化器がん

- 大腸がん

- 肺がん

- その他のがん種

第7章 市場推計・予測:プロバイダ別、2021年~2034年

- 主要動向

- 病院

- がんセンター

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Alliance HealthCare Services

- American Oncology Institute

- Apollo Hospitals Enterprise

- Cancer Treatment Centers of America

- Compass Oncology

- Curie Oncology

- Fortis Healthcare

- GenesisCare

- HCA Healthcare

- Healthcare Global Enterprises

- IHH Healthcare Berhad

- Narayana Hrudayalaya

- OncoLife Hospitals

- Ramsay Health Care

- Tenet Healthcare

The Global Cancer Treatment Facilities Market was valued at USD 49.8 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 102.9 billion by 2034. Cancer treatment centers are specialized healthcare institutions focused on the diagnosis, treatment, and ongoing management of various cancer types. These centers typically offer services such as chemotherapy, radiation therapy, immunotherapy, surgical treatments, and aftercare. They employ multidisciplinary teams of professionals, including oncologists, surgeons, radiologists, and nursing staff, to ensure tailored care for each patient.

The rising global prevalence of cancer is the main driver for this market. Aging populations significantly contribute to the growing number of cancer diagnoses, which in turn is increasing the demand for specialized cancer care. To meet these needs, treatment facilities are enhancing their infrastructure and adopting advanced technologies, such as precision oncology and multidisciplinary treatment models. These innovations aim to cater to the growing elderly demographic, which is particularly vulnerable to cancer. Additionally, medical tourism is contributing to the expansion of the cancer treatment market, particularly in regions where affordable treatment options attract international patients seeking high-quality care at lower costs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $49.8 Billion |

| Forecast Value | $102.9 Billion |

| CAGR | 7.6% |

The blood cancer segment held the largest share of 26.1% in 2024. This growth is driven by the ongoing clinical demand and the extensive infrastructure required to treat hematological cancers, including specialized treatment facilities. Moreover, the complex, costly, and often intensive treatment protocols, which involve chemotherapy, bone marrow transplants, and immunotherapy, are major contributors to the market's expansion. Moreover, the requirement for long-term follow-up care, the involvement of multidisciplinary medical teams, and the need for advanced diagnostic capabilities further emphasize the importance of these specialized treatment centers over those focused on other cancer types.

In 2024, the hospitals segment held the largest market share, accounting for 67.5% share, and is expected to continue growing at a CAGR of 7.5%. The demand for cancer treatment facilities in hospitals is driven by the availability of advanced detection tools and a wide range of treatment options, including chemotherapy, radiation, and hormone therapy. Patients prefer hospitals for their comprehensive services and access to multidisciplinary care teams.

U.S. Cancer Treatment Market was valued at USD 14.9 billion in 2024 and is expected to see continued growth due to an aging population and an increase in cancer cases. This has led to the development of integrated cancer centers that provide cutting-edge treatments like robotic surgery, immunotherapy, and precision medicine. Major industry players, such as HCA Healthcare, are expanding their reach through partnerships and incorporating AI technologies. Government initiatives and value-based care models further drive market growth.

Key players in the Global Cancer Treatment Facilities Market include Alliance HealthCare Services, American Oncology Institute, Apollo Hospitals Enterprise, Cancer Treatment Centers of America, Compass Oncology, Curie Oncology, Fortis Healthcare, GenesisCare, HCA Healthcare, Healthcare Global Enterprises, IHH Healthcare Berhad, Narayana Hrudayalaya, OncoLife Hospitals, Ramsay Health Care, Tenet Healthcare. To strengthen their market position, companies in the cancer treatment facilities sector are focusing on the integration of advanced technologies such as AI, robotic surgery, and precision medicine. They are also expanding their services through strategic partnerships with other healthcare providers and organizations. The increasing adoption of value-based care models helps improve patient outcomes while reducing costs. Many organizations are building integrated cancer care centers to offer comprehensive services, from diagnosis to post-treatment care.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer

- 3.2.1.2 Growing geriatric population

- 3.2.1.3 Rise in medical tourism

- 3.2.1.4 Increase in government initiatives and awareness programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled oncology personnel

- 3.2.2.2 High cost of advanced treatments and technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Reimbursement Scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cancer surgery

- 5.3 Chemotherapy

- 5.4 Radiation therapy

- 5.5 Immunotherapy

- 5.6 Bone marrow transplantation

- 5.7 Other treatment types

Chapter 6 Market Estimates and Forecast, By Cancer Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Blood cancer

- 6.3 Breast cancer

- 6.4 Prostate cancer

- 6.5 Gastrointestinal cancer

- 6.6 Colorectal cancer

- 6.7 Lung cancer

- 6.8 Other cancer types

Chapter 7 Market Estimates and Forecast, By Provider, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Cancer centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alliance HealthCare Services

- 9.2 American Oncology Institute

- 9.3 Apollo Hospitals Enterprise

- 9.4 Cancer Treatment Centers of America

- 9.5 Compass Oncology

- 9.6 Curie Oncology

- 9.7 Fortis Healthcare

- 9.8 GenesisCare

- 9.9 HCA Healthcare

- 9.10 Healthcare Global Enterprises

- 9.11 IHH Healthcare Berhad

- 9.12 Narayana Hrudayalaya

- 9.13 OncoLife Hospitals

- 9.14 Ramsay Health Care

- 9.15 Tenet Healthcare