自動車用サンバイザーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Automotive Sun Visor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755255

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

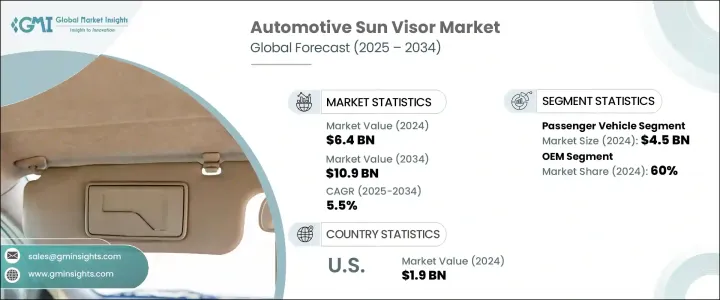

自動車用サンバイザーの世界市場規模は、2024年に64億米ドルとなり、CAGR 5.5%で成長し、2034年には109億米ドルに達すると予測されています。

この成長の原動力となっているのは、世界の自動車生産台数の増加であり、車内の快適性や交通安全の向上に対する消費者の期待の高まりがこの拡大を後押ししています。自動車メーカーが生産台数を拡大するにつれ、特に新興経済諸国では、サンバイザーのような内装部品の主な需要が増加し続けています。消費者は、基本的な遮光だけでなく、統合照明、タッチコントロール、まぶしさ低減技術などの機能を組み込んだ高度なサンバイザーシステムを求めています。こうしたアップグレードは、快適性と視認性を優先し、スタイリッシュでありながら機能的なインテリアを求める消費者の高まりに応えるものです。さらに、規制機関や安全基準によって、メーカーは商用車と乗用車の両方にバイザーの強化機能を標準装備するよう求められています。

交通安全に対するニーズの高まりも、需要を押し上げる上で重要な役割を果たしています。サンバイザーはドライバーの視認性を向上させ、まぶしさに関連した事故を防ぐのに役立ち、交通事故を減らすための世界の取り組みと一致しています。電気自動車は、その近代的な内装から高度でカスタマイズ可能なバイザーシステムが求められることが多いため、市場の成長にさらに貢献しています。EVメーカーは、先進的なキャビンデザインにシームレスに溶け込む高品質で技術強化されたバイザーを好み、このセグメント全体の技術革新に拍車をかけています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 64億米ドル |

| 予測金額 | 109億米ドル |

| CAGR | 5.5% |

2024年の乗用車の市場規模は45億米ドルで、生産台数の多さと日常的な使用により、セグメント全体をリードしています。これらの自動車は、各地域で個人の移動の中心となっており、サンバイザーのような快適性を高める内装部品への一貫した需要を促進しています。自動車メーカーが美観と安全性の向上に投資を続ける中、サンバイザーには照明付きミラー、拡張フラップ、運転体験を向上させるスマート機能などが装備されています。エントリーモデルからハイエンドセダンまで、幅広い車種が提供されているため、さまざまなニーズや好みに合わせた多様なバイザーソリューションが確保されています。

OEM部門は2024年に60%のシェアを占め、サンバイザーの自動車への組み込み方法において支配的な役割を維持しています。これらのメーカーは、厳しい性能と安全基準を満たすために、生産段階でバイザーを調達しています。オーダーメイドの工場装着部品を提供する能力により、コスト効率が高くシームレスなバイザーソリューションを提供する上で競争力を発揮しています。自動車メーカーとティア1サプライヤーの協力関係も強化され、ブランドアイデンティティと消費者の期待を反映した、照明付きバニティミラーや先進素材などの付加機能を備えた革新的な製品が可能となっています。

北米の自動車用サンバイザー2024年の市場規模は19億米ドルで、2034年までのCAGRは5.8%で成長する見込みです。アメリカ市場は、強力な安全規制と技術的に統合された車両内装に対する需要の増加から引き続き利益を得ています。メーカーは、実用性と美観を融合させた多機能サンバイザーにシフトしています。高級車や電気自動車の販売急増により、進化するプレミアムドライブ環境のコンセプトをサポートするハイエンドサンバイザーのデザインが求められています。現代的な素材、デジタル・インターフェース、洗練されたスタイリングを統合することで、サンバイザーは車室内の体験に不可欠な要素へと変貌を遂げます。

自動車用サンバイザー市場を形成する主要企業には、Visteon, Tachi-S, Grupo Antolin, Continental, Setrag, IAC, Shiroki, Kasai Kogyo, Howa Textile, and Adient. などがあります。これらの企業は、進化する消費者の需要に応えるため、戦略的な製品革新に投資しています。その多くは、耐久性を維持しながら車両全体の重量を軽減する、軽量でモジュール化された設計の開発に注力しています。アンチグレアフィルムやスマートミラーソリューションなど、先進材料の統合は性能向上のために利用されています。また、自動車メーカーとの協力関係を強化し、ブランディングや人間工学に沿ったOEM専用設計を提供する企業も増えています。競争力と市場リーチを強化するために、特にコスト効率の高い地域での製造拠点の拡大と製品ポートフォリオの多様化が引き続き中心的な戦略となっています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向s

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 従来型

- 照明付き

- デュアルパネル

- LCD/デジタル

- カスタム/組み込み

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- ファブリック

- ビニール

- プラスチック

- その他

第7章 市場推計・予測:車種別、2021年~2034年

- 主要動向

- 乗用車

- SUV

- ハッチバック

- セダン

- 商用車

- 小型商用車(LCV)

- 中型商用車(MCV)

- 大型商用車(HCV)

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 太陽光からの保護

- ドライバーと乗客の快適性向上

- 化粧鏡の統合

- リアウィンドウとサイドウィンドウの用途

- その他

第9章 市場推計・予測:販売チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第11章 企業プロファイル

- AC Group

- Adient

- CIE Automotive

- Continental

- Faurecia

- Ficosa

- Grupo Antolin

- Howa Textile

- Kasai Kogyo

- Lear Corporation

- Magneti Marelli

- Motherson Sumi

- NHK Spring

- Setrag

- Shiroki

- Tachi-S

- Tokai Rika

- Toyota Boshoku

- Visteon

- Yanfeng

目次

The Global Automotive Sun Visor Market was valued at USD 6.4 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 10.9 billion by 2034. The growth is driven by the increasing vehicle production worldwide, along with rising consumer expectations for better in-cabin comfort and road safety, is driving this expansion. As automakers scale output-especially in fast-developing economies-the demand for key interior components like sun visors continues to rise. Consumers seek advanced sun visor systems beyond basic shading and incorporate features like integrated lighting, touch controls, and glare-reducing technology. These upgrades cater to the growing desire for stylish yet functional interiors that prioritize comfort and visibility. Additionally, regulatory bodies and safety standards are prompting manufacturers to include enhanced visor features as part of standard offerings in both commercial and passenger vehicles.

The growing need for road safety also plays a critical role in boosting demand. Sun visors improve driver visibility and help prevent glare-related incidents, aligning with global initiatives to reduce traffic accidents. Electric vehicles contribute further to the market's growth, as their modern interiors often call for sophisticated, customizable visor systems. EV manufacturers prefer high-quality, tech-enhanced visors that blend seamlessly into their advanced cabin designs fueling innovation across the segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.4 Billion |

| Forecast Value | $10.9 Billion |

| CAGR | 5.5% |

Passenger vehicles accounted for a market value of USD 4.5 billion in 2024, leading the overall segment due to their large production volumes and everyday usage. These vehicles are central to personal mobility across regions, which fuels consistent demand for comfort-enhancing interior parts like sun visors. As automakers continue investing in aesthetic and safety improvements, sun visors are equipped with illuminated mirrors, extension flaps, and smart functionality to elevate the driving experience. From entry-level models to high-end sedans, the broad spectrum of vehicle offerings ensures a diverse range of visor solutions tailored to varying needs and preferences.

OEMs segment represented a 60% share in 2024, maintaining a dominant role in how sun visors are integrated into vehicles. These manufacturers source visors during the production stage to meet strict performance and safety criteria. Their ability to provide tailored, factory-fitted components gives them a competitive edge in delivering cost-effective and seamless visor solutions. Collaborations between automakers and Tier 1 suppliers have also intensified, allowing for innovative products with added features like lighted vanity mirrors and advanced materials that reflect brand identity and consumer expectations.

North America Automotive Sun Visor Market held USD 1.9 billion in 2024 and is set to grow at a CAGR of 5.8% through 2034. The American market continues to benefit from strong safety regulations and increasing demand for tech-integrated vehicle interiors. Manufacturers are shifting toward multi-functional sun visors that blend utility with aesthetics. A surge in luxury and electric vehicle sales drives the need for high-end sun visor designs that support the evolving concept of premium driving environments. Integrating modern materials, digital interfaces, and sleek styling transforms sun visors into essential components of the vehicle's cabin experience.

Leading players shaping the Automotive Sun Visor Market include Visteon, Tachi-S, Grupo Antolin, Continental, Setrag, IAC, Shiroki, Kasai Kogyo, Howa Textile, and Adient. These companies are investing in strategic product innovations to meet evolving consumer demands. Many focus on developing lightweight and modular designs that reduce overall vehicle weight while maintaining durability. Advanced material integration, such as anti-glare films and smart mirror solutions, is being used to improve performance. Firms are also strengthening collaborations with automakers to deliver OEM-specific designs that align with branding and ergonomics. Expanding manufacturing footprints, particularly in cost-effective regions, and diversifying product portfolios remain central strategies to enhance competitiveness and market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Material

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Sales channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Conventional

- 5.3 Illuminated

- 5.4 Dual-panel

- 5.5 LCD/digital

- 5.6 Custom/built-in

Chapter 6 Market Estimates & Forecast, By Material Type, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Fabric

- 6.3 Vinyl

- 6.4 Plastic

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger Vehicle

- 7.2.1 SUV

- 7.2.2 Hatchbacks

- 7.2.3 Sedan

- 7.3 Commercial Vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Sun glare protection

- 8.3 Driver and passenger comfort enhancement

- 8.4 Vanity mirror integration

- 8.5 Rear and side window applications

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AC Group

- 11.2 Adient

- 11.3 CIE Automotive

- 11.4 Continental

- 11.5 Faurecia

- 11.6 Ficosa

- 11.7 Grupo Antolin

- 11.8 Howa Textile

- 11.9 Kasai Kogyo

- 11.10 Lear Corporation

- 11.11 Magneti Marelli

- 11.12 Motherson Sumi

- 11.13 NHK Spring

- 11.14 Setrag

- 11.15 Shiroki

- 11.16 Tachi-S

- 11.17 Tokai Rika

- 11.18 Toyota Boshoku

- 11.19 Visteon

- 11.20 Yanfeng

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日