アルミニウム製漁船の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Aluminium Fishing Boat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755236

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

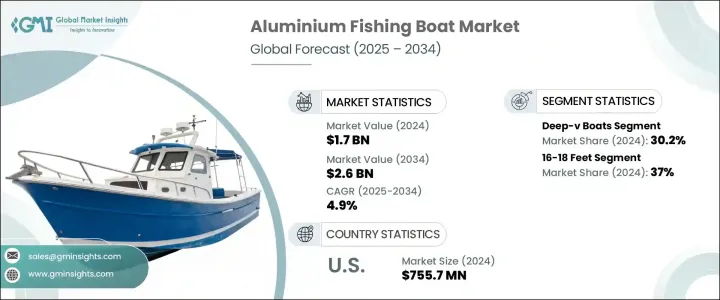

世界のアルミニウム製漁船市場は、2024年に17億米ドルと評価され、CAGR4.9%で成長し、2034年までには26億米ドルに達すると推定されています。

市場成長の主な原動力は、レクリエーションフィッシングの人気の高まりと、内陸および淡水釣り場の拡大です。特に自然をベースとした観光が勢いを増すにつれて、アウトドア活動に従事する人が増えています。アルミ製ボートは、軽量設計、燃費効率、長持ちする耐久性により、好まれる選択肢になりつつあります。

アングリングツーリズムを推進し、淡水釣りのインフラを強化する政府のイニシアティブにより、こうしたボートはニッチなツールから主流のレクリエーション資産へと移行しつつあり、先進国市場と新興国市場の両方で需要増につながっています。レクリエーション用ボートの急増、特に若年層や家族連れの増加も、市場を再構築しています。消費者は、湖、川、貯水池など、さまざまな淡水環境で柔軟性と使いやすさを提供するボートを求めるようになっています。メーカー各社は、多様な消費者ニーズに対応するため、カスタマイズ可能な機能や人間工学に基づいたデザインの改良を導入することで、この需要に応えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 17億米ドル |

| 予測金額 | 26億米ドル |

| CAGR | 4.9% |

2024年には、ディープVボートのセグメントが30.2%のシェアで市場をリードし、2025年から2034年にはCAGR5.5%で成長を続けると予測されます。ディープV型アルミボートは、安定性、多用途性、高性能のため、特にレクリエーションアングラーの間で支持されています。これらのボートは、不安定な水域でも優れた性能を発揮し、コントロール性とスピードが向上するため、内陸の湖や大きな河川、さらには沿岸の近海地域にも理想的です。また、スポーツアングラー、フィッシングガイド、長期旅行を求める愛好家、さまざまな釣り条件に対応する多目的ボートを必要とする愛好家にも人気があります。

2024年には、16フィートから18フィートのボートセグメントが37%のシェアを占め、2025年から2034年までCAGR6%で成長すると予測されています。これらのボートは、スペースと操縦性の実用的なバランスを提供し、レクリエーションアングラーや小規模な漁業のための最良の選択肢となっています。その大きさから、淡水域でも内陸水域でも、曳航、保管、航行が容易です。また、手頃な価格と多様性で人気があり、さまざまなフィッシングアクティビティをサポートし、ロッドホルダーやライブウェルなど、数多くの構成を提供しています。

米国のアルミニウム製漁船市場は75.3%のシェアを占め、2024年には7億5,570万米ドルを創出しました。ミネソタ州、ウィスコンシン州、ミシガン州など、釣り文化の盛んな州はアルミボートの主要市場です。地元メーカーは、船体設計、モーターとの統合、顧客中心のイノベーションの面で高い基準を設定し、この分野でのリーダーシップを確固たるものにしています。アウトドアレクリエーションを支援し、漁業免許を取得できるよう政府が支援するプログラムは、市場の成長をさらに後押ししています。

世界のアルミニウム製漁船市場の主要企業は、G3 Boats、Alumacraft Boat、Legend Boats、MirroCraft、SeaArk Boats、Brunswick、Princecraft Boats、Smoker Craft、White River Marine Group、Xpress Boatsなどです。市場ポジションを強化するため、アルミニウム製漁船セクターの企業は、製品の革新とサービス提供の拡大に注力しています。メーカー各社は、耐久性、性能、燃費効率を向上させるため、先進素材や技術を取り入れたボートの設計を継続的に改善しています。

また、パーソナライズされたレクリエーションボート体験の需要の高まりに応えるため、人間工学に基づいた座席やカスタマイズ可能な構成など、顧客中心の機能を優先しています。さらに、主要企業は大手小売業者と提携し、流通網を拡大して新市場に参入しています。各社はまた、持続可能な製造プロセスを模索し、環境に優しい素材を使用し、環境意識の高い消費者にアピールする手法を採用しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 一次調査と検証

- 一次情報

- 予測モデル

- 調査の前提条件と制限

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 成長促進要因

- レクリエーション釣りの人気の高まり

- 内水・淡水漁業区域の拡大

- ボート所有率の増加

- 海洋観光に対する政府の支援

- 業界の潜在的リスク・課題

- プレミアムビルドの初期コストが高め

- 季節的な需要への依存

- 市場機会

- 成長促進要因

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格分析

- 地域

- 推進

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:ボート別、2021年~2034年

- 主要動向

- ディープVボート

- ジョンボート

- ユーティリティボート

- バスボート

- ポンツーンボート

第6章 市場推計・予測:長さ別、2021年~2034年

- 主要動向

- 14フィート未満

- 14~16フィート

- 16~18フィート

- 18フィート以上

第7章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- ガソリン

- ディーゼル

- 電気モーター

- 天然ガス

- その他

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- レクリエーション釣り

- 商業漁業

- レンタルサービス

- 政府/救助活動

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- Alumacraft Boat

- Brunswick

- Crestliner Boats

- Duckworth Boats

- G3 Boats

- Hewescraft Boats

- Legend Boats

- Lowe Boats

- Lund Boats

- MirroCraft

- Polar Kraft Boats

- Princecraft Boats

- Quintrex

- SeaArk Boats

- Smoker Craft

- Stabicraft Marine

- Sylvan Marine

- Weldcraft Marine

- White River Marine Group

- Xpress Boats

目次

The Global Aluminium Fishing Boat Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 2.6 billion by 2034. The market growth is largely driven by the increasing popularity of recreational fishing, as well as the expansion of inland and freshwater fishing areas. More people are engaging in outdoor activities, particularly as nature-based tourism gains momentum. Aluminium boats are becoming the preferred option due to their lightweight design, fuel efficiency, and long-lasting durability.

With government initiatives promoting angling tourism and enhancing freshwater fishing infrastructure, these boats are now transitioning from niche tools to mainstream recreational assets, leading to increased demand in both developed and emerging markets. The surge in recreational boating, particularly among younger individuals and families, is also reshaping the market. Consumers are increasingly seeking boats that offer flexibility and ease of use in various freshwater environments such as lakes, rivers, and reservoirs. Manufacturers are responding to this demand by introducing customizable features and improved ergonomic designs to meet diverse consumer needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 4.9% |

In 2024, the deep-V boat segment led the market with a 30.2% share and is expected to continue growing at a CAGR of 5.5% during 2025-2034. Deep-V aluminium boats are favored for their stability, versatility, and high performance, particularly among recreational anglers. These boats perform well in choppy waters, offering enhanced control and speed, making them ideal for inland lakes, large rivers, and even nearshore coastal regions. They are also popular among sports anglers, fishing guides, and enthusiasts who seek long trips or need multi-purpose boats for varied fishing conditions.

In 2024, the 16-18 feet boat segment accounted for 37% share and is projected to grow at a CAGR of 6% from 2025 to 2034. These boats offer a practical balance of space and maneuverability, making them the top choice for recreational anglers and small fishing operations. Their size makes them easy to tow, store, and navigate in both freshwater and inland waters. They are also popular due to their affordability and versatility, supporting a range of fishing activities and offering numerous configurations such as rod holders and live wells.

United States Aluminium Fishing Boat Market held a 75.3% share and generated USD 755.7 million in 2024 driven by its well-established culture of recreational fishing, extensive freshwater networks, and a robust marine manufacturing infrastructure. States with a strong angling culture, like Minnesota, Wisconsin, and Michigan, are key markets for aluminium boats. Local manufacturers are setting high standards in terms of hull design, motor integration, and customer-centric innovations, solidifying their leadership in the sector. Government-backed programs supporting outdoor recreation and access to fishing licenses further bolster market growth.

Key players in the Global Aluminium Fishing Boat Market include G3 Boats, Alumacraft Boat, Legend Boats, MirroCraft, SeaArk Boats, Brunswick, Princecraft Boats, Smoker Craft, White River Marine Group, and Xpress Boats. To strengthen their market position, companies in the aluminium fishing boat sector are focusing on product innovation and expanding their service offerings. Manufacturers are continuously improving boat designs to incorporate advanced materials and technologies, enhancing durability, performance, and fuel efficiency.

They are also prioritizing customer-centric features, such as ergonomic seating and customizable configurations, to cater to the growing demand for personalized recreational boating experiences. In addition, key players are forging partnerships with major retailers and expanding their distribution networks to reach new markets. Companies are also exploring sustainable manufacturing processes, using eco-friendly materials, and adopting practices that appeal to environmentally conscious consumers.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Boat

- 2.2.3 Length

- 2.2.4 Propulsion

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising popularity of recreational fishing

- 3.2.1.2 Expansion of inland and freshwater fishing zones

- 3.2.1.3 Increasing boat ownership rates

- 3.2.1.4 Government support for marine tourism

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost for premium builds

- 3.2.2.2 Dependence on seasonal demand

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Pricing Analysis

- 3.8.1 Region

- 3.8.2 Propulsion

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Boat, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Deep-V boats

- 5.3 Jon boats

- 5.4 Utility boats

- 5.5 Bass boats

- 5.6 Pontoon boats

Chapter 6 Market Estimates & Forecast, By Length, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Less than 14 feet

- 6.3 14–16 feet

- 6.4 16–18 feet

- 6.5 More than 18 feet

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Gasoline

- 7.3 Diesel

- 7.4 Electric motors

- 7.5 Natural gas

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Recreational fishing

- 8.3 Commercial fishing

- 8.4 Rental services

- 8.5 Government/Rescue operations

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Alumacraft Boat

- 10.2 Brunswick

- 10.3 Crestliner Boats

- 10.4 Duckworth Boats

- 10.5 G3 Boats

- 10.6 Hewescraft Boats

- 10.7 Legend Boats

- 10.8 Lowe Boats

- 10.9 Lund Boats

- 10.10 MirroCraft

- 10.11 Polar Kraft Boats

- 10.12 Princecraft Boats

- 10.13 Quintrex

- 10.14 SeaArk Boats

- 10.15 Smoker Craft

- 10.16 Stabicraft Marine

- 10.17 Sylvan Marine

- 10.18 Weldcraft Marine

- 10.19 White River Marine Group

- 10.20 Xpress Boats

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日