|

市場調査レポート

商品コード

1755226

ハイパーオートメーションの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Hyper Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ハイパーオートメーションの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月19日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

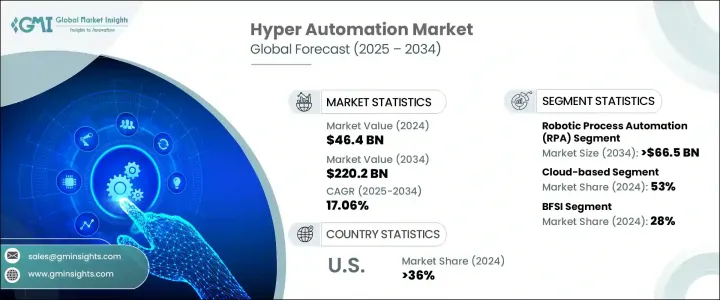

ハイパーオートメーションの世界市場規模は、2024年に464億米ドルとなり、CAGR 17.06%で成長し、2034年には2,202億米ドルに達すると予測されています。

企業は効率性を高め、リソースの消費を最小限に抑える努力をしており、ハイパーオートメーションは重要なソリューションとして台頭しています。AI、機械学習、ロボティック・プロセス・オートメーション(RPA)を活用することで、反復的で労働集約的なタスクを自動化し、ボトルネックの解消、エラーの削減、ワークフローの精度向上を支援します。これにより、企業は市場の変化に迅速に対応し、より効率的に業務を進め、生産性を向上させ、よりスマートなオペレーションを推進することができます。

各業界がデジタルトランスフォーメーションを進める中、ハイパーオートメーションは、プロセスの自動化とリアルタイムの意思決定を可能にし、従来の手作業からより柔軟なデジタルワークフローへの移行を促進することで、重要な役割を果たしています。カスタマーサービスでもサプライチェーンマネジメントでも、ハイパーオートメーションは業務を加速させます。拡張性に優れているため、システムの大幅な見直しをすることなくビジネスを成長させることができ、技術の進歩や進化する顧客の期待に対応することを目指す企業にとって不可欠なツールとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 464億米ドル |

| 予測金額 | 2,202億米ドル |

| CAGR | 17.06% |

2024年、ロボティック・プロセス・オートメーション(RPA)分野の売上高は156億米ドルを超え、2034年には665億米ドルを超えると予測されています。RPAは、データ入力や請求書処理などのありふれた作業を自動化することで、ハイパーオートメーションを強化し、ヒューマンエラーのリスクを排除した効率的な組織運営を可能にします。RPAツールは既存のワークフローにシームレスに統合されるため、技術インフラを全面的に見直すことなく自動化のメリットを享受できます。このため、RPAは、業務効率が重要な銀行や物流など、反復作業が多い業界にとって魅力的なソリューションとなっています。

クラウドベースのセグメントは2024年に53%のシェアを占めています。クラウドベースのハイパーオートメーションソリューションは、柔軟性とアクセスのしやすさを提供するため、迅速な展開とリモート機能を求める企業に最適です。このようなシステムにより、大規模なインフラ投資が不要となり、企業はハードウェアコストを削減しながら自動化戦略を拡大することができます。さらに、自動更新により、チームはリアルタイムで共同作業を行うことができ、業務の俊敏性と応答性が向上します。

北米のハイパーオートメーション市場は、強固なデジタルインフラと新興技術に対する政府の強力な支援に後押しされ、2024年には36%のシェアを占める。さまざまな業界の企業が、AI、機械学習、ロボティック・プロセス・オートメーションを統合し、業務の柔軟性を高め、コストを削減しています。このシフトにより、企業は市場のダイナミクスや進化する顧客の需要に迅速に対応できるようになります。教育機関、テクノロジー企業、業界リーダー間のコラボレーションは継続的なイノベーションを促進し、高度なスキルを持つ労働力の利用可能性は実装を加速させる。

世界のハイパーオートメーション業界の主要企業には、Google、Oracle、ServiceNow、UiPath、Honeywell International、Microsoft Corporation、SAP SE、Automation Anywhere、TCS、WorkFusionなどがあります。ハイパーオートメーション業界の企業は、市場での存在感を維持・成長させるため、いくつかの戦略的イニシアティブに注力しています。主な戦略の1つは、多様な顧客ニーズに対応するため、高度なAI、機械学習、RPA機能を取り入れた製品ポートフォリオの拡充です。各社はまた、製造、ヘルスケア、ロジスティクスなどの各分野の業界リーダーと戦略的パートナーシップを結び、自動化における特定の課題に対応するテーラーメイドのソリューションを構築しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- サプライヤーの情勢

- RPAプロバイダー

- AI/MLソリューションベンダー

- BPM &ワークフロープラットフォーム

- クラウドと統合イネーブラー

- ERPおよびエンタープライズオートメーションベンダー

- 利益率分析

- テクノロジーとイノベーションの情勢

- 主なニュースと取り組み

- 特許分析

- 規制情勢

- 影響要因

- 促進要因

- 業務効率の向上に対する需要

- 業界をまたぐ急速なデジタル変革

- コスト削減と拡張性の必要性の高まり

- ビジネスプロセスの複雑化

- 業界の潜在的リスク&課題

- ハイパーオートメーションを大規模に実装する

- ハイパーオートメーションイニシアチブの有効性を損なう

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:技術タイプ別、2021年~2034年

- ロボティックプロセスオートメーション(RPA)

- 人工知能(AI)と機械学習(ML)

- ビジネスプロセス管理(BPM)

- インテリジェントドキュメント処理(IDP)

- ローコード/ノーコードプラットフォーム

第6章 市場推計・予測:展開別、2021年~2034年

- クラウドベース

- オンプレミス

第7章 市場推計・予測:ソリューション別、2021年~2034年

- ソフトウェア

- 自動化ソフトウェア

- インテリジェントドキュメント処理(IDP)ソリューション

- クラウド自動化プラットフォーム

- 高度な分析とレポートツール

- サービス

- 専門サービス

- 展開と統合

- コンサルティング

- サポートとメンテナンス

- マネージドサービス

- 専門サービス

第8章 市場推計・予測:最終用途別、2021年~2034年

- BFSI(銀行、金融サービス、保険)

- ヘルスケア

- 製造業

- 小売り

- ITおよび通信

- 政府および公共部門

- 運輸・物流

- その他

第9章 市場推計・予測:組織規模別、2021年~2034年

- 大企業

- 中小企業

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第11章 企業プロファイル

- Allerin Tech

- Appian

- Automation Anywhere

- Catalytic

- Celonis

- Fortra

- Honeywell International

- Microsoft Corporation

- Mitsubishi Electric Corporation

- OneGlobe

- Oracle Corporation

- Redwood Software

- SAP SE

- ServiceNow

- SolveXia

- Tata Consultancy Services(TCS)

- UiPath

- Wipro Ltd

- WorkFusion

The Global Hyper Automation Market was valued at USD 46.4 billion in 2024 and is estimated to grow at a CAGR of 17.06% to reach USD 220.2 billion by 2034 as businesses strive to enhance efficiency and minimize resource consumption, hyper automation is emerging as a crucial solution. By leveraging AI, machine learning, and robotic process automation (RPA), it automates repetitive, labor-intensive tasks, helping organizations eliminate bottlenecks, reduce errors, and improve workflow precision. This allows companies to respond quickly to market changes and operate more efficiently, increasing productivity and driving smarter operations.

As industries undergo digital transformation, hyper automation plays a vital role by enabling the automation of processes and fostering real-time decision-making, facilitating a shift from traditional manual methods to more flexible, digital workflows. Whether in customer service or supply chain management, hyper automation accelerates operations. Its scalable nature enables businesses to grow without major system overhauls, making it an essential tool for companies aiming to keep pace with technological advancements and evolving customer expectations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $46.4 Billion |

| Forecast Value | $220.2 Billion |

| CAGR | 17.06% |

In 2024, the robotic process automation (RPA) segment generated over USD 15.6 billion in revenue and is expected to surpass USD 66.5 billion by 2034. RPA enhances hyper automation by automating mundane tasks, such as data entry and invoice processing, allowing organizations to run more efficiently without the risk of human error. RPA tools integrate seamlessly into existing workflows, offering organizations the benefits of automation without requiring a complete overhaul of their technological infrastructure. This makes RPA an attractive solution for industries burdened with repetitive tasks, such as banking and logistics, where operational efficiency is critical.

The cloud-based segment held a 53% share in 2024. Cloud-based hyper automation solutions offer flexibility and ease of access, making them ideal for businesses looking for fast deployment and remote capabilities. These systems eliminate the need for heavy infrastructure investments and enable organizations to scale their automation strategies while reducing hardware costs. Additionally, automatic updates allow teams to collaborate in real time, improving operational agility and responsiveness.

North America Hyper Automation Market held 36% share in 2024 fueled by robust digital infrastructure and strong government support for emerging technologies. Companies across various industries are integrating AI, machine learning, and robotic process automation to enhance operational flexibility and reduce costs. This shift enables businesses to respond rapidly to market dynamics and evolving customer demands. Collaborations between educational institutions, technology firms, and industry leaders foster continuous innovation, while the availability of a highly skilled workforce accelerates implementation.

Key players in the Global Hyper Automation Industry include Google, Oracle, ServiceNow, UiPath, Honeywell International, Microsoft Corporation, SAP SE, Automation Anywhere, TCS, and WorkFusion. To maintain and grow their market presence, companies in the hyper automation industry are focused on several strategic initiatives. One of the primary strategies is the expansion of their product portfolios, incorporating advanced AI, machine learning, and RPA capabilities to meet diverse customer needs. Companies are also forming strategic partnerships with industry leaders across sectors like manufacturing, healthcare, and logistics to create tailored solutions that address specific challenges in automation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.3.1 RPA Providers

- 3.3.2 AI/ML Solution Vendors

- 3.3.3 BPM & Workflow Platforms

- 3.3.4 Cloud & Integration Enablers

- 3.3.5 ERP & Enterprise Automation Vendors

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Demand for enhanced operational efficiency

- 3.9.1.2 Rapid digital transformation across industries

- 3.9.1.3 Increasing need for cost reduction and scalability

- 3.9.1.4 Rising complexity of business processes

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Implementing hyper automation at scale

- 3.9.2.2 Undermining the effectiveness of hyper automation initiatives

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology Type, 2021 - 2034 (USD, Mn)

- 5.1 Robotic process automation (RPA)

- 5.2 Artificial intelligence (AI) and machine learning (ML)

- 5.3 Business process management (BPM)

- 5.4 Intelligent document processing (IDP)

- 5.5 Low-code/No-code platforms

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 (USD, Mn)

- 6.1 Cloud-based

- 6.2 On-premises

Chapter 7 Market Estimates & Forecast, By Solution, 2021 - 2034 (USD, Mn)

- 7.1 Software

- 7.1.1 Automation software

- 7.1.2 Intelligent document processing (IDP) solutions

- 7.1.3 Cloud automation platforms

- 7.1.4 Advanced analytics & reporting tools

- 7.2 Services

- 7.2.1 Professional services

- 7.2.1.1 Deployment & integration

- 7.2.1.2 Consulting

- 7.2.1.3 Support & maintenance

- 7.2.2 Managed services

- 7.2.1 Professional services

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Mn)

- 8.1 BFSI (Banking, Financial Services, and Insurance)

- 8.2 Healthcare

- 8.3 Manufacturing

- 8.4 Retail

- 8.5 IT and Telecom

- 8.6 Government and public sector

- 8.7 Transportation and logistics

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Organization Size, 2021 - 2034 (USD, Mn)

- 9.1 Large enterprises

- 9.2 SME (Small and Medium Enterprises)

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Allerin Tech

- 11.2 Appian

- 11.3 Automation Anywhere

- 11.4 Catalytic

- 11.5 Celonis

- 11.6 Fortra

- 11.7 Google

- 11.8 Honeywell International

- 11.9 Microsoft Corporation

- 11.10 Mitsubishi Electric Corporation

- 11.11 OneGlobe

- 11.12 Oracle Corporation

- 11.13 Redwood Software

- 11.14 SAP SE

- 11.15 ServiceNow

- 11.16 SolveXia

- 11.17 Tata Consultancy Services (TCS)

- 11.18 UiPath

- 11.19 Wipro Ltd

- 11.20 WorkFusion