車両制御ユニットの市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Vehicle Control Unit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1755223

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

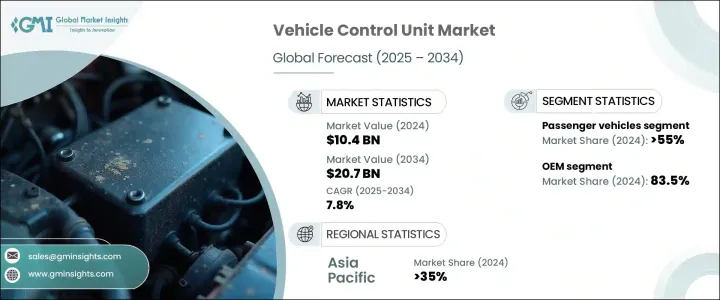

車両制御ユニットの世界市場規模は、2024年に104億米ドルとなり、CAGR 7.8%で成長し、2034年には207億米ドルに達すると予測されています。

市場成長の原動力は、電気自動車(EV)の普及が進んでいることです。EVは、バッテリーシステム、電気モーター、回生ブレーキ、充電操作などの複雑な機能を効率的に管理するVCUを必要とします。従来の内燃自動車とは異なり、EVは複数の相互接続システムに依存しており、リアルタイムの調整が必要です。VCUはこのプロセスの中心的存在であり、エネルギー管理、安全性、車両インテリジェンスを向上させる。持続可能性に関する規制が強化され、インセンティブが高まるにつれて、自動車メーカーはEVの生産を加速させており、その結果、より高度でスケーラブルなVCUソリューションに対するニーズが世界的に高まっています。

また、ソフトウェア定義の車両アーキテクチャへの移行により、市場も拡大しています。自動車メーカーはVCUを統合することで、OTA(Over-the-Air)アップデート、リアルタイム診断、車両集中監視を可能にしています。これらのシステムは、モジュール式の機能アップグレードと適応的な性能管理を可能にします。さらに、商用車と乗用車の両方でADASと自律走行技術の需要が高まっており、高性能VCUのニーズがさらに高まっています。幅広いセンサーからの入力を処理することで、VCUは車線支援、緊急ブレーキ、アダプティブ・クルーズ・コントロールなどのインテリジェントな運転機能を促進し、最新の車両設計に不可欠なものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 104億米ドル |

| 予測金額 | 207億米ドル |

| CAGR | 7.8% |

2024年、乗用車セグメントは50億米ドルを生み出し、特に米国、中国、欧州などの主要市場で55%のシェアを占める。高度化するデジタル機能を搭載した新型車が組立ラインから出荷されるにつれて、統合型VCUの需要は急増し続けています。乗用車は電気自動車やハイブリッド・ドライブトレインへの移行を主導しており、複数のデジタル・サブシステムを包括的に調整する必要があります。VCUはこの統合をシームレスにし、インフォテインメント、安全、運転支援システムをサポートしながら最適な車両性能を確保します。

2024年にはOEMセグメントが市場をリードし、83.5%のシェアを獲得しました。車両制御ユニットは製造過程で車両システムに組み込まれるため、OEMが主要なインテグレーターとなります。これらのユニットは、異なる車両プラットフォームやブランドのアーキテクチャに合わせてカスタマイズする必要があります。OEMとティア1サプライヤーの開発協力により、VCUは規制遵守と統合効率を念頭に開発されます。集中型コンピューティングやソフトウェアファーストの車両設計を好む傾向が強まる中、OEMはOTA機能やクラウドベースのサービス、リアルタイムのシステムアップグレードなどの高度な機能をサポートするVCUを導入しており、その市場規模はさらに拡大しています。

アジア太平洋の車両制御ユニット市場は2024年に35%のシェアを占める。世界有数の自動車生産拠点である中国は、強力な国内生産能力、低コスト製造、積極的な政府支援といったメリットを享受しています。電気自動車やインテリジェント車に対するインセンティブ・プログラムや国産VCU技術の進歩により、中国はVCU採用の最前線に位置しています。スマートモビリティとエネルギー効率の高い自動車を推進する同国は、新しい自動車プラットフォームへのVCUの展開を加速させています。

世界の車両制御ユニット市場の主要企業には、ASI Robots、Continental AG、Robert Bosch、Infineon、Denso、ZF Friedrichshafen AG、STMicroelectronics、NXP Semiconductors、Dorleco、Delphi Technologiesなどがあります。これらの企業は、市場での競争力を確保するため、さまざまな戦略を駆使しています。中心的なアプローチには、車両の電動化とADASをサポートするモジュラーVCUプラットフォームの開発や、カスタマイズされた統合のための自動車メーカーとの提携が含まれます。主要企業は、AI主導のVCUソリューション、クラウド接続、OTAアップデートフレームワークに投資しています。さらに、進化する自動車の安全規制やソフトウェア規制に対応しつつ、世界の需要の高まりに対応するため、多くの企業がアジアや欧州での製造能力を拡大しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 影響要因

- 促進要因

- 電気自動車の成長

- ADAS(先進運転支援システム)と自動化の台頭

- 接続性とインフォテインメントの需要

- 厳しい排出ガスおよび安全規制

- 業界の潜在的リスク&課題

- 開発および実装コストが高め

- 増大するサイバーセキュリティリスク

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向s

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:推進力別、2021年~2034年

- 主要動向

- ICE

- 電気自動車(EV)

- 燃料電池電気自動車(FCEV)

第6章 市場推計・予測:車両別、2021年~2034年

- 主要動向

- 乗用車

- セダン

- SUV

- ハッチバック

- 商用車

- 小型商用車

- MCV

- HCV

- オフロード車両

第7章 市場推計・予測:機能別、2021年~2034年

- 主要動向

- パワートレイン制御

- バッテリー管理システム(BMS)の統合

- ADAS(先進運転支援システム)(ADAS)

- インフォテインメントとコネクティビティ

- 自動運転システム

- その他

第8章 市場推計・予測:容量別、2021年~2034年

- 主要動向

- 16ビット

- 32ビット

- 64ビット

第9章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- マイクロコントローラ/マイクロプロセッサ

- メモリユニット

- 入出力インターフェース

- 電源管理コンポーネント

- その他

- ソフトウェア

- オペレーティングシステム

- 制御アルゴリズム

- 診断システム

- ユーザーインターフェース

- その他

第10章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- OEM

- アフターマーケット

第11章 市場推計・予測:コミュニケーションタイプ別、2021年~2034年

- 主要動向

- CAN(コントローラエリアネットワーク)

- LIN(ローカル相互接続ネットワーク)

- FlexRay(フレキシブルデータレートネットワーク)

- イーサネット

第12章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第13章 企業プロファイル

- ASI Robots

- Continental

- Delphi Technologies

- Denso

- Dorleco

- Embitel

- Hitachi Astemo

- Huawei Technologies

- Infineon

- Nidec Corporation

- NXP Semiconductors

- Pues Corporation

- Renesas Electronics Corporation

- Robert Bosch

- Samino Inc

- STMicroelectronics

- Texas Instruments

- Valeo

- Vitesco Technologies

- ZF Friedrichshafen

目次

The Global Vehicle Control Unit Market was valued at USD 10.4 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 20.7 billion by 2034. The market growth is driven by the rising adoption of electric vehicles (EVs), which require VCUs to efficiently manage complex functions such as battery systems, electric motors, regenerative braking, and charging operations. Unlike traditional internal combustion vehicles, EVs rely on multiple interconnected systems that need real-time coordination. VCUs are central to this process, improving energy management, safety, and vehicle intelligence. As sustainability regulations tighten and incentives increase, automakers are accelerating EV production, which in turn is increasing the need for more advanced and scalable VCU solutions globally.

The market is also expanding due to the shift towards software-defined vehicle architectures. Automakers are integrating VCUs to enable over-the-air (OTA) updates, real-time diagnostics, and centralized vehicle monitoring. These systems allow for modular feature upgrades and adaptive performance management. Additionally, rising demand for ADAS and autonomous technologies in both commercial and passenger vehicles is further boosting the need for high-performance VCUs. By processing input from a wide range of sensors, VCUs facilitate intelligent driving functions such as lane assistance, emergency braking, and adaptive cruise control-making them vital in modern vehicle designs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.4 Billion |

| Forecast Value | $20.7 Billion |

| CAGR | 7.8% |

In 2024, the passenger vehicle segment generated USD 5 billion, claiming 55% share especially in leading markets such as the United States, China, and Europe. As newer vehicles roll off assembly lines with increasingly sophisticated digital features, the demand for integrated VCUs continues to surge. Passenger cars are leading the transition to electric and hybrid drivetrains, which require comprehensive coordination across multiple digital subsystems. VCUs make this integration seamless, ensuring optimal vehicle performance while supporting infotainment, safety, and driver-assist systems.

The OEM segment led the market in 2024, capturing 83.5% share. Vehicle control units are embedded into vehicle systems during the manufacturing process, making OEMs the primary integrators. These units must be customized to suit the architecture of different vehicle platforms and brands. Collaborations between OEMs and Tier 1 suppliers ensure that VCUs are developed with regulatory compliance and integration efficiency in mind. With a growing preference for centralized computing and software-first vehicle design, OEMs are deploying VCUs to support advanced functionalities like OTA capabilities, cloud-based services, and real-time system upgrades, which further expands their market footprint.

Asia Pacific Vehicle Control Unit Market held 35% share in 2024. As one of the top automotive manufacturing hubs globally, China benefits from strong domestic production capabilities, low-cost manufacturing, and proactive government support. Incentive programs for electric and intelligent vehicles, as well as advancements in homegrown VCU technologies, have positioned China at the forefront of VCU adoption. The country's push for smart mobility and energy-efficient vehicles is accelerating the rollout of VCUs across new vehicle platforms.

Key players in the Global Vehicle Control Unit Market include ASI Robots, Continental AG, Robert Bosch, Infineon, Denso, ZF Friedrichshafen AG, STMicroelectronics, NXP Semiconductors, Dorleco, and Delphi Technologies. These companies are leveraging a range of strategies to secure competitive positioning in the market. Core approaches include the development of modular VCU platforms that support vehicle electrification and ADAS, as well as partnerships with automakers for customized integration. Major players are investing in AI-driven VCU solutions, cloud connectivity, and OTA update frameworks. Additionally, many are expanding their manufacturing capabilities in Asia and Europe to meet rising global demand while complying with evolving automotive safety and software regulations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.5 Forecast model

- 1.6 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Vehicle

- 2.2.4 Functionality

- 2.2.5 Capacity

- 2.2.6 Component

- 2.2.7 Distribution Channel

- 2.2.8 Communication Type

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of electric vehicles

- 3.2.1.2 Rise of advanced driver assistance systems and automation

- 3.2.1.3 Connectivity and infotainment demand

- 3.2.1.4 Stringent emission and safety regulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High development and implementation costs

- 3.2.2.2 Growing cybersecurity risks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 ICE

- 5.3 Electric Vehicles (EVs)

- 5.4 Fuel Cell Electric Vehicles (FCEVs)

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger Vehicles

- 6.2.1 Sedan

- 6.2.2 SUV

- 6.2.3 Hatchback

- 6.3 Commercial Vehicles

- 6.3.1 LCV

- 6.3.2 MCV

- 6.3.3 HCV

- 6.4 Off-highway Vehicles

Chapter 7 Market Estimates & Forecast, By Functionality, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Powertrain control

- 7.3 Battery management system (BMS) integration

- 7.4 Advanced driver assistance systems (ADAS)

- 7.5 Infotainment and connectivity

- 7.6 Autonomous driving systems

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 16-bit

- 8.3 32-bit

- 8.4 64-bit

Chapter 9 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Hardware

- 9.2.1 Microcontrollers/microprocessors

- 9.2.2 Memory units

- 9.2.3 Input/output interfaces

- 9.2.4 Power management components

- 9.2.5 Others

- 9.3 Software

- 9.3.1 Operating systems

- 9.3.2 Control algorithms

- 9.3.3 Diagnostic systems

- 9.3.4 User interfaces

- 9.3.5 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Communication Type, 2021 - 2034 ($Bn)

- 11.1 Key trends

- 11.2 CAN (Controller Area Network)

- 11.3 LIN (Local Interconnect Network)

- 11.4 FlexRay (Flexible Data-Rate Network)

- 11.5 Ethernet

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Nordics

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Southeast Asia

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 UAE

- 12.6.2 South Africa

- 12.6.3 Saudi Arabia

Chapter 13 Company Profiles

- 13.1 ASI Robots

- 13.2 Continental

- 13.3 Delphi Technologies

- 13.4 Denso

- 13.5 Dorleco

- 13.6 Embitel

- 13.7 Hitachi Astemo

- 13.8 Huawei Technologies

- 13.9 Infineon

- 13.10 Nidec Corporation

- 13.11 NXP Semiconductors

- 13.12 Pues Corporation

- 13.13 Renesas Electronics Corporation

- 13.14 Robert Bosch

- 13.15 Samino Inc

- 13.16 STMicroelectronics

- 13.17 Texas Instruments

- 13.18 Valeo

- 13.19 Vitesco Technologies

- 13.20 ZF Friedrichshafen

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日