|

市場調査レポート

商品コード

1755214

エレクトロクロミック材料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Electrochromic Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| エレクトロクロミック材料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月20日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

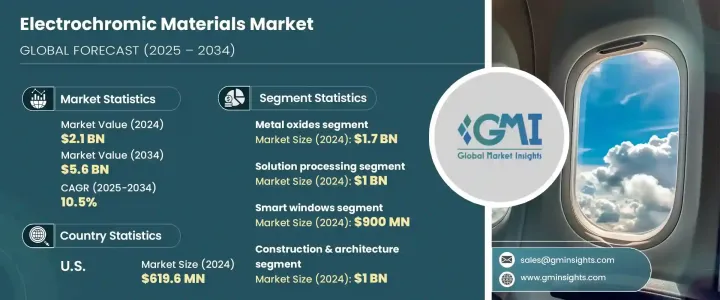

エレクトロクロミック材料の世界市場は、2024年には21億米ドルと評価され、住宅と商業ビルの両方で人気を集めているスマート窓の需要増加に牽引され、CAGR 10.5%で成長し、2034年には56億米ドルに達すると予測されています。

これらの窓は、光と熱を制御することでエネルギー消費を削減するのに役立ち、エネルギー効率基準を満たすことを目的としたグリーンビルディングプロジェクトの重要な構成要素となっています。

さらに、エレクトロクロミック材料は、自動車産業、特に自動調光ミラー、アダプティブ・サンルーフ、サイド・ウィンドウへの応用が拡大しています。これらの技術革新は、ユーザーの快適性を向上させ、まぶしさを軽減するだけでなく、自動車のブランド力を高める。導電性ポリマーやハイブリッド複合材料を含む材料科学の進歩は、エレクトロクロミック材料の性能とコスト効率を向上させ、その採用を後押ししています。省エネルギーが重要視されるにつれ、特に持続可能性の基準が厳しい地域では、これらの材料に対する需要が大幅に急増しています。エネルギー効率を高めるその能力は、用途における重要な構成要素となり、エネルギー消費の削減を目指す産業にとって不可欠なソリューションとして位置づけられています。グリーン認証取得を目指す建設プロジェクトから、燃費改善に焦点を当てた自動車用途に至るまで、これらの材料は環境的・経済的目標を達成する上で重要な役割を果たしています。汎用性の高さ、規制圧力の高まり、持続可能なソリューションを求める消費者の需要が、これらの材料の普及を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 21億米ドル |

| 予測金額 | 56億米ドル |

| CAGR | 10.5% |

2024年、ソリューション処理分野は10億米ドルを占め、2034年までCAGR 9.6%で成長すると予測されます。この成長は、スマート・ウィンドウやディスプレイのような用途にますます使用されるようになっているソリューション処理方法の費用対効果と拡張性に起因しています。これらの方法は汎用性があるため、幅広い基板に適合し、建築や自動車分野の成長をさらに後押ししています。

2024年に9億米ドルと評価されるスマート窓分野も、エネルギー効率の高い製品に対する需要の高まりによって急拡大すると予測されています。これらの窓は、建物のエネルギー消費を抑え、快適性を高めるのに役立ちます。スマートミラーとサンルーフは、その快適性と安全性から人気を集めています。

米国エレクトロクロミック材料2024年の市場規模は6億1,960万米ドルで、スマートビルや自動車における省エネルギー技術の需要増加を背景に、2034年までCAGR 10%で成長すると予測されます。米国市場は、持続可能性とエネルギー効率に優れた技術に焦点を当てた強力な政府規制と、技術革新と技術進歩を推進する業界大手企業の積極的な関与から恩恵を受けています。

エレクトロクロミック材料世界市場の主要企業には、Gentex Corporation、AGC Inc.、Sage Electrochromics, Inc.(サンゴバン)、PPG Industries, Inc.、View, Inc.などが含まれます。エレクトロクロミック材料市場での地位を強化するため、企業は複数の戦略に注力しています。主なアプローチのひとつは、エネルギー効率の高いアプリケーションに対する需要の高まりに対応する革新的な高性能製品を生み出すための研究開発への継続的投資です。エレクトロクロミック材料の機能を向上させることで、企業は市場競争力を高めることを目指しています。多くの企業が、住宅、商業施設、自動車用途のスマートウィンドウ・ソリューションなど、製品ポートフォリオを拡大しています。さらに、建設会社、自動車メーカー、政府とのパートナーシップは、新たな市場機会を確保し、これらの技術を大規模プロジェクトに確実に組み込むために不可欠です。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 市場イントロダクション

- トランプ政権の関税の影響- 構造化された概要

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)注:上記の貿易統計は主要国についてのみ提供されます

- 主要輸出国

- 国1

- 国2

- 国3

- 主要輸入国

- 国1

- 国2

- 国3

- 主要輸出国

- 業界バリューチェーン分析

- 素材の概要

- エレクトロクロミズム:原理とメカニズム

- 酸化還元反応と色の変化のプロセス

- 光変調特性

- スイッチング速度と着色効率

- 耐久性とサイクリング安定性

- エネルギー効率特性

- 他のスマートマテリアルとの比較

- 市場力学

- 市場促進要因

- 省エネスマートウィンドウの需要増加

- 自動車用途での採用増加

- エレクトロクロミック材料における技術の進歩

- グリーンビルディング認証の重要性の高まり

- 市場抑制要因

- エレクトロクロミックデバイスの初期コストが高め

- 一部の材料タイプではスイッチング速度が制限される

- 市場機会

- 市場の課題

- 市場促進要因

- 業界への影響要因

- 成長可能性分析

- 業界の潜在的リスク&課題

- 規制の枠組みと基準

- エネルギー効率規制

- 建築基準法

- 自動車の安全基準

- 環境規制

- 性能試験基準

- 製造プロセス分析

- 材料合成方法

- 薄膜堆積技術

- デバイス製造プロセス

- 品質管理手順

- 原材料分析と調達戦略

- 価格分析

- 持続可能性と環境影響評価

- PESTEL分析

- ポーターのファイブフォース分析

第4章 競合情勢

- 市場シェア分析

- 戦略的枠組み

- 合併と買収

- ジョイントベンチャーとコラボレーション

- 新製品開発

- 拡大戦略

- 競合ベンチマーキング

- ベンダー情勢

- 競合ポジショニングマトリックス

- 戦略的ダッシュボード

- 特許分析とイノベーション評価

- 新規参入者のための市場参入戦略

- 調査開発集約度分析

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- 金属酸化物

- 酸化タングステン(WO3)

- 酸化ニッケル(NiO)

- 二酸化チタン(TiO2)

- 五酸化バナジウム(V2O5)

- 酸化モリブデン(MoO3)

- その他の金属酸化物

- 導電性ポリマー

- ポリアニリン(PANI)

- ポリピロール(PPy)

- ポリ(3,4-エチレンジオキシチオフェン)(PEDOT)

- その他の導電性ポリマー

- ビオロゲン

- プルシアンブルー類似体

- 液晶

- ハイブリッドおよび複合材料

- その他のエレクトロクロミック材料

第6章 市場推計・予測:技術別、2021年~2034年

- 主要動向

- ソリューション処理

- ゾルゲル法

- 電着

- スピンコーティング

- その他の溶液処理方法

- 蒸着

- 物理蒸着(PVD)

- 化学蒸着(CVD)

- スパッタリング

- その他の蒸着法

- 印刷技術

- インクジェット印刷

- スクリーン印刷

- その他の印刷方法

- その他の技術

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- スマートウィンドウ

- 建築用窓

- 天窓と屋根窓

- パーティションとプライバシーガラス

- その他のスマートウィンドウアプリケーション

- スマートミラー

- 自動車用ミラー

- 建築用ミラー

- その他のミラーアプリケーション

- ディスプレイ

- 電子ペーパーディスプレイ

- 情報ディスプレイ

- その他のディスプレイアプリケーション

- 自動車用途

- サンルーフ

- バックミラー

- サイドウィンドウ

- その他の自動車用途

- 航空宇宙用途

- ウェアラブルデバイス

- エネルギー貯蔵装置

- その他の用途

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- 建設・アーキテクチャ

- 住宅

- 商業ビル

- 公共施設

- その他の建物の種類

- 自動車・輸送

- 乗用車

- 商用車

- その他の交通手段

- 航空宇宙および防衛

- 電子機器とディスプレイ

- 海洋

- ヘルスケアと医療

- その他の最終用途産業

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Gentex Corporation

- View, Inc.

- ChromoGenics AB

- Sage Electrochromics, Inc.(Saint-Gobain)

- AGC Inc.

- Magna Glass and Window Company

- Guardian Industries Corp.

- PPG Industries, Inc.

- Kinestral Technologies, Inc.

- E Ink Holdings Inc.

- Gesimat GmbH

- EControl-Glas GmbH &Co. KG

- Merck KGaA

- 3M Company

- Nippon Sheet Glass Co., Ltd.

- Halio, Inc.

- Pleotint LLC

- Research Frontiers Inc.

- Heliotrope Technologies

- SAGE Electrochromics, Inc.

- Polytronix, Inc.

- Chromogenics AB

- Innovative Glass Corporation

- Gauzy Ltd.

- Smart Glass International Ltd.

- SPD Control Systems Corporation

- Diamond Glass

- InvisiShade

- Continental AG

The Global Electrochromic Materials Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 10.5% to reach USD 5.6 billion by 2034, driven by the increasing demand for smart windows, which are gaining popularity in both residential and commercial buildings. These windows help reduce energy consumption by controlling light and heat, making them a key component in green building projects aiming to meet energy efficiency standards.

Additionally, electrochromic materials are seeing increased applications in the automotive industry, particularly in self-dimming mirrors, adaptive sunroofs, and side windows. These innovations not only improve user comfort and reduce glare but also enhance vehicle branding. The advancement of material science, including conducting polymers and hybrid composites, has improved the performance and cost-efficiency of electrochromic materials, driving their adoption. As energy conservation gains importance, particularly in regions with stringent sustainability standards, the demand for these materials is experiencing a significant surge. Their ability to enhance energy efficiency makes them a key component in applications, positioning them as a vital solution for industries seeking to reduce energy consumption. From construction projects aiming for green certifications to automotive applications focused on improving fuel efficiency, these materials play a crucial role in meeting environmental and economic goals. Their versatility, growing regulatory pressure, and consumer demand for sustainable solutions, drive their widespread adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 10.5% |

In 2024, the solution processing segment accounted for USD 1 billion and is expected to grow at a CAGR of 9.6% through 2034. This growth is attributed to the cost-effectiveness and scalability of solution processing methods, which are increasingly used for applications like smart windows and displays. These methods offer versatility, making them compatible with a wide range of substrates, further boosting growth in the architectural and automotive sectors.

The smart windows segment, valued at USD 900 million in 2024, is also projected to expand rapidly, driven by the growing demand for energy-efficient products. These windows help reduce energy consumption in buildings and enhance comfort. Smart mirrors and sunroofs are gaining popularity for their comfort and safety benefits.

U.S. Electrochromic Materials Market was valued at USD 619.6 million in 2024 and is expected to grow at a 10% CAGR through 2034 driven by the increasing demand for energy-saving technologies in smart buildings and vehicles. The U.S. market benefits from strong governmental regulations focused on sustainability and energy-efficient technologies, and the active involvement of leading industry players driving innovation and technical advancements.

Key players in the Global Electrochromic Materials Market include Gentex Corporation, AGC Inc., Sage Electrochromics, Inc. (Saint-Gobain), PPG Industries, Inc., and View, Inc. To strengthen their position in the electrochromic materials market, companies are focusing on multiple strategies. One key approach is the continued investment in research and development to create innovative, high-performance products that cater to the growing demand for energy-efficient applications. By advancing the capabilities of electrochromic materials, companies aim to enhance their market competitiveness. Many are expanding their product portfolios to include smart window solutions for residential, commercial, and automotive applications. In addition, partnerships with construction firms, automotive manufacturers, and governments are vital for securing new market opportunities and ensuring the integration of these technologies into large-scale projects.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research methodology

- 1.2 Research scope & assumptions

- 1.3 List of data sources

- 1.4 Market estimation technique

- 1.5 Market segmentation & breakdown

- 1.6 Research limitations

Chapter 2 Executive Summary

- 2.1 Market snapshot

- 2.2 Segment highlights

- 2.3 Competitive landscape snapshot

- 2.4 Regional market outlook

- 2.5 Key market trends

- 2.6 Future market outlook

Chapter 3 Industry Insights

- 3.1 Market Introduction

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (hs code) Note: The above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.1.1 Country 1

- 3.3.1.2 Country 2

- 3.3.1.3 Country 3

- 3.3.2 Major importing countries

- 3.3.2.1 Country 1

- 3.3.2.2 Country 2

- 3.3.2.3 Country 3

- 3.3.1 Major exporting countries

- 3.4 Industry value chain analysis

- 3.5 Material overview

- 3.5.1 Electrochromism: principles & mechanisms

- 3.5.2 Redox reactions & color change processes

- 3.5.3 Optical modulation properties

- 3.5.4 Switching speed & coloration efficiency

- 3.5.5 Durability & cycling stability

- 3.5.6 Energy efficiency characteristics

- 3.5.7 Comparison with other smart materials

- 3.6 Market dynamics

- 3.6.1 Market drivers

- 3.6.1.1 Rising demand for energy-efficient smart windows

- 3.6.1.2 Increasing adoption in automotive applications

- 3.6.1.3 Technological advancements in electrochromic materials

- 3.6.1.4 Growing emphasis on green building certifications

- 3.6.2 Market restraints

- 3.6.2.1 High initial cost of electrochromic devices

- 3.6.2.2 Limited switching speed for some material types

- 3.6.3 Market opportunities

- 3.6.4 Market challenges

- 3.6.1 Market drivers

- 3.7 Industry impact forces

- 3.7.1 Growth potential analysis

- 3.7.2 Industry pitfalls & challenges

- 3.8 Regulatory framework & standards

- 3.9 Energy efficiency regulations

- 3.9.1 Building codes & standards

- 3.9.2 Automotive safety standards

- 3.9.3 Environmental regulations

- 3.9.4 Performance testing standards

- 3.10 Manufacturing process analysis

- 3.10.1 Material synthesis methods

- 3.10.2 Thin film deposition techniques

- 3.10.3 Device fabrication processes

- 3.10.4 Quality control procedures

- 3.11 Raw material analysis & procurement strategies

- 3.12 Pricing analysis

- 3.13 Sustainability & environmental impact assessment

- 3.14 Pestle analysis

- 3.15 Porter's five forces analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Market Share Analysis

- 4.2 Strategic Framework

- 4.2.1 Mergers & Acquisitions

- 4.2.2 Joint Ventures & Collaborations

- 4.2.3 New Product Developments

- 4.2.4 Expansion Strategies

- 4.3 Competitive Benchmarking

- 4.4 Vendor Landscape

- 4.5 Competitive Positioning Matrix

- 4.6 Strategic Dashboard

- 4.7 Patent Analysis & Innovation Assessment

- 4.8 Market Entry Strategies for New Players

- 4.9 Research & Development Intensity Analysis

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Metal oxides

- 5.2.1 Tungsten oxide (WO3)

- 5.2.2 Nickel oxide (NiO)

- 5.2.3 Titanium dioxide (TiO2)

- 5.2.4 Vanadium pentoxide (V2O5)

- 5.2.5 Molybdenum oxide (MoO3)

- 5.2.6 Other metal oxides

- 5.3 Conducting polymers

- 5.3.1 Polyaniline (PANI)

- 5.3.2 Polypyrrole (PPy)

- 5.3.3 Poly(3,4-ethylenedioxythiophene) (PEDOT)

- 5.3.4 Other conducting polymers

- 5.4 Viologens

- 5.5 Prussian blue analogs

- 5.6 Liquid crystals

- 5.7 Hybrid & composite materials

- 5.8 Other electrochromic materials

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solution processing

- 6.2.1 Sol-gel method

- 6.2.2 Electrodeposition

- 6.2.3 Spin coating

- 6.2.4 Other solution processing methods

- 6.3 Vapor deposition

- 6.3.1 Physical vapor deposition (PVD)

- 6.3.2 Chemical vapor deposition (CVD)

- 6.3.3 Sputtering

- 6.3.4 Other vapor deposition methods

- 6.4 Printing technologies

- 6.4.1 Inkjet printing

- 6.4.2 Screen printing

- 6.4.3 Other printing methods

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Smart windows

- 7.2.1 Architectural windows

- 7.2.2 Skylights & roof windows

- 7.2.3 Partitions & privacy glass

- 7.2.4 Other smart window applications

- 7.3 Smart mirrors

- 7.3.1 Automotive mirrors

- 7.3.2 Architectural mirrors

- 7.3.3 Other mirror applications

- 7.4 Displays

- 7.4.1 E-paper displays

- 7.4.2 Information displays

- 7.4.3 Other display applications

- 7.5 Automotive applications

- 7.5.1 Sunroofs

- 7.5.2 Rearview mirrors

- 7.5.3 Side windows

- 7.5.4 Other automotive applications

- 7.6 Aerospace applications

- 7.7 Wearable devices

- 7.8 Energy storage devices

- 7.9 Other applications

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Construction & architecture

- 8.2.1 Residential buildings

- 8.2.2 Commercial buildings

- 8.2.3 Institutional buildings

- 8.2.4 Other building types

- 8.3 Automotive & transportation

- 8.3.1 Passenger vehicles

- 8.3.2 Commercial vehicles

- 8.3.3 Other transportation

- 8.4 Aerospace & defense

- 8.5 Electronics & displays

- 8.6 Marine

- 8.7 Healthcare & medical

- 8.8 Other end-use industries

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Gentex Corporation

- 10.2 View, Inc.

- 10.3 ChromoGenics AB

- 10.4 Sage Electrochromics, Inc. (Saint-Gobain)

- 10.5 AGC Inc.

- 10.6 Magna Glass and Window Company

- 10.7 Guardian Industries Corp.

- 10.8 PPG Industries, Inc.

- 10.9 Kinestral Technologies, Inc.

- 10.10 E Ink Holdings Inc.

- 10.11 Gesimat GmbH

- 10.12 EControl-Glas GmbH & Co. KG

- 10.13 Merck KGaA

- 10.14 3M Company

- 10.15 Nippon Sheet Glass Co., Ltd.

- 10.16 Halio, Inc.

- 10.17 Pleotint LLC

- 10.18 Research Frontiers Inc.

- 10.19 Heliotrope Technologies

- 10.20 SAGE Electrochromics, Inc.

- 10.21 Polytronix, Inc.

- 10.22 Chromogenics AB

- 10.23 Innovative Glass Corporation

- 10.24 Gauzy Ltd.

- 10.25 Smart Glass International Ltd.

- 10.26 SPD Control Systems Corporation

- 10.27 Diamond Glass

- 10.28 InvisiShade

- 10.29 Continental AG