|

市場調査レポート

商品コード

1755203

神経学機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Neurology Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 神経学機器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月19日

発行: Global Market Insights Inc.

ページ情報: 英文 165 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

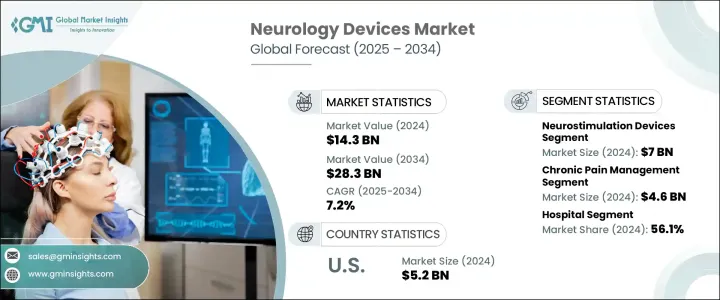

世界の神経学機器市場は、2024年に143億米ドルと評価され、技術革新、神経疾患の発生率の上昇、ヘルスケア支出の増加、医療サービスへのアクセスの改善などが相まって、CAGR 7.2%で成長し、2034年には283億米ドルに達すると推定されています。

AIを活用した遠隔モニタリングやブレイン・コンピュータ・インターフェイス・システムの開発により、患者の治療成績が大幅に向上しています。さらに、ポータブルEEGモニターや強化された刺激システムなど、新たに登場した低侵襲神経技術は、神経学的治療と診断に変革をもたらしつつあります。これらの進歩により、より正確で安全かつ効率的な治療介入が可能となり、神経学機器分野全体の拡大に寄与しています。神経学機器には、脳、脊椎、末梢神経などの神経系に影響を及ぼす状態を管理するために使用される埋め込み型器具、手術器具、診断技術が含まれます。

神経学機器には、脳、脊椎、末梢神経などの神経系に影響を及ぼす状態を管理するために使用される移植可能なツール、外科器具、診断技術が含まれます。これらの機器は、てんかん、パーキンソン病、アルツハイマー病、多発性硬化症、脳腫瘍、外傷性脳損傷などの神経疾患の検出、モニタリング、治療、リハビリテーションを支援するように設計されています。日常的な神経学的評価から複雑な神経外科的処置まで、さまざまな臨床場面で重要な役割を果たしています。EEGシステムや神経画像技術のような診断ツールは、神経疾患の早期かつ正確な特定に役立つ一方、神経刺激装置のような埋め込み型装置は、慢性疾患や進行性疾患に苦しむ患者に長期的な治療効果をもたらします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 143億米ドル |

| 予測金額 | 283億米ドル |

| CAGR | 7.2% |

主要カテゴリーのうち、神経刺激装置セグメントは2024年に70億米ドルを生み出しました。これらには、脊髄刺激装置や迷走神経刺激装置などのシステムが含まれ、運動障害、慢性疼痛、精神医学的問題、てんかんに対処するように設計されています。クローズドループシステム、MRI対応インプラント、小型化ソリューションなどの新しいモデルは、患者の転帰を改善し、治療用途を広げており、このセグメントの成長を強化しています。

最終用途別では、病院が包括的なインフラと複雑な神経学的症例への対応能力を背景に、2024年の市場を56.1%の圧倒的なシェアで牽引しました。病院は診断や治療処置の大半を行うため、神経画像診断システムや神経調節システムの導入において重要な拠点となっています。発作、脳卒中、外傷などの神経学的な緊急事態を管理する役割を担っているため、最先端の機器に対する需要は絶え間なく高まっています。

米国の神経学機器2024年の市場規模は52億米ドルで、神経疾患の有病率の増加、強固な臨床研究インフラ、政府からの多額の資金援助に支えられています。主要な連邦政府のイニシアティブと研究助成金は、神経補綴とブレイン・コンピュータ・インターフェイス・システムの進歩を支援し続けています。高齢者人口の増加と神経学の専門家不足も、高まるケア需要に対応するため、先進機器への依存度を高めています。

神経学機器業界情勢を積極的に形成している主要企業は、Synchron、B BRAUN、LivaNova、NeuroPace、ZYLOX TONBRIDGE、Abbott Laboratories、MicroTransponder、KARL STROZ、Medtronic、stryker、Bioness、nevro、Boston Scientific、Enterra Medical、Paradromicsなどです。主要企業は、神経学機器市場での地位を強化するために、研究主導型の製品イノベーションとAI統合システムの市場開拓に注力しています。これらの企業は、安全性と精度を高める低侵襲デバイスや患者固有のソリューションでポートフォリオを拡大しています。戦略的パートナーシップ、規制当局の承認、神経技術の研究開発への投資拡大も、こうした企業のアプローチの中心となっています。各企業は、イメージング・システムとの機器の互換性を改善し、より広範な臨床使用のためにコンパクトで携帯可能な形式を追求しています。さらに、大手企業は製造能力を拡大し、契約を確保し、地理的プレゼンスを高め、よりスマートな神経学的ケアの提供を目指すヘルスケアシステムと連携するために、世界な協力関係を結ぼうとしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 神経疾患の有病率の上昇

- 低侵襲手術の採用増加

- 技術的進歩

- 資金と投資の増加

- 業界の潜在的リスク&課題

- 機器や手順の高コスト

- デバイスの故障や合併症のリスク

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- テクノロジーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 償還シナリオ

- ポーター分析

- PESTEL分析

- ギャップ分析

- 将来の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:デバイス別、2021年~2034年

- 主要動向

- 神経刺激装置

- 脊髄刺激装置

- 脳深部刺激装置

- 迷走神経刺激装置

- 仙骨神経刺激装置

- 胃電気刺激装置

- 脳神経外科用デバイス

- 定位放射線治療システム

- 神経内視鏡

- 超音波吸引器

- 動脈瘤クリップ

- 介入的神経学機器

- 動脈瘤コイル塞栓術

- 塞栓コイル

- 流量転換装置

- 液体塞栓試薬

- 神経血栓除去術

- 血栓除去器

- 吸引吸引装置

- スネア装置

- 神経血管カテーテル

- マイクロカテーテル

- マイクロガイドワイヤー

- 脳バルーン血管形成術およびステント

- 頸動脈ステント

- フィルターデバイス

- バルーン閉塞デバイス

- CSF管理デバイス

- 脳シャント

- 脳外ドレナージ

- 動脈瘤コイル塞栓術

- 脳コンピューターインターフェースデバイス

- 非侵襲性BCI

- 部分侵襲性BCI

- 完全侵襲性BCI

- その他のデバイス

第6章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 慢性疼痛管理

- パーキンソン病

- てんかん

- 脳卒中の管理と回復

- アルツハイマー病

- その他の用途

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- B BRAUN

- Bioness

- Boston Scietific

- enterra medical

- KARL STROZ

- LivaNova

- Medtronic

- MicroTransponder

- NeuroPace

- nevro

- Paradromics

- stryker

- synchron

- ZYLOX TONBRIDGE

The Global Neurology Devices Market was valued at USD 14.3 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 28.3 billion by 2034, fueled by a combination of technological innovation, rising rates of neurological conditions, increased healthcare spending, and improved access to medical services. Developments in AI-powered remote monitoring and brain-computer interface systems have significantly improved patient care outcomes. In addition, emerging minimally invasive neurotechnologies-such as portable EEG monitors and enhanced stimulation systems-are transforming neurological treatment and diagnosis. These advances have made it possible to deliver more precise, safer, and efficient therapeutic interventions, contributing to the overall expansion of the neurology devices sector. Neurology devices include implantable tools, surgical instruments, and diagnostic technologies used to manage conditions affecting the nervous system, such as the brain, spine, and peripheral nerves.

Neurology devices include implantable tools, surgical instruments, and diagnostic technologies used to manage conditions affecting the nervous system, such as the brain, spine, and peripheral nerves. These devices are designed to aid in the detection, monitoring, treatment, and rehabilitation of neurological disorders, including epilepsy, Parkinson's disease, Alzheimer's disease, multiple sclerosis, brain tumors, and traumatic brain injuries. They serve a critical role across a range of clinical settings, from routine neurological assessments to complex neurosurgical procedures. Diagnostic tools such as EEG systems and neuroimaging technologies help in the early and accurate identification of neurological conditions, while implantable devices like neurostimulators offer long-term therapeutic benefits for patients suffering from chronic and progressive diseases.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.3 Billion |

| Forecast Value | $28.3 Billion |

| CAGR | 7.2% |

Among the main categories, the neurostimulation devices segment generated USD 7 billion in 2024. These include systems like spinal cord stimulators and vagus nerve stimulators, designed to address movement disorders, chronic pain, psychiatric issues, and epilepsy. Newer models, such as closed-loop systems, MRI-compatible implants, and miniaturized solutions, have improved patient outcomes and broadened therapeutic applications, reinforcing growth in this segment.

By end use, hospitals led the market in 2024 with a dominant share of 56.1%, driven by their comprehensive infrastructure and ability to handle complex neurological cases. Hospitals conduct a majority of diagnostic and therapeutic procedures, making them key hubs for the adoption of neuroimaging and neuromodulation systems. Their role in managing emergency neurological events such as seizures, strokes, and traumatic injuries ensures constant demand for cutting-edge equipment.

United States Neurology Devices Market was valued at USD 5.2 billion in 2024, supported by increasing neurological disease prevalence, robust clinical research infrastructure, and substantial government funding. Major federal initiatives and research grants continue to back advancements in neuroprosthetics and brain-computer interface systems. A growing elderly population and a shortage of specialized neurology professionals are also pushing greater reliance on advanced devices to meet the rising demand for care.

Key players actively shaping The Neurology Devices Industry landscape include Synchron, B BRAUN, LivaNova, NeuroPace, ZYLOX TONBRIDGE, Abbott Laboratories, MicroTransponder, KARL STROZ, Medtronic, stryker, Bioness, nevro, Boston Scientific, Enterra Medical, and Paradromics. To strengthen their position in the neurology devices market, leading companies are focusing on research-driven product innovation and the development of AI-integrated systems. These firms are expanding their portfolios with minimally invasive devices and patient-specific solutions that enhance safety and precision. Strategic partnerships, regulatory approvals, and increased investments in neurotechnology R&D are also central to their approach. Businesses are refining device compatibility with imaging systems and pursuing compact, portable formats for broader clinical use. Additionally, major players are scaling up manufacturing capabilities and entering into global collaborations to secure contracts, boost geographic presence, and align with healthcare systems aiming for smarter neurological care delivery.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of neurological disorders

- 3.2.1.2 Growing adoption of minimally invasive procedure

- 3.2.1.3 Technological advancements

- 3.2.1.4 Increased funding and investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and procedures

- 3.2.2.2 Risk of device failure and complications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Trump administration tariffs

- 3.6.1 Impact on trade

- 3.6.1.1 Trade volume disruptions

- 3.6.1.2 Retaliatory measures

- 3.6.2 Impact on the Industry

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.2.1.1 Price volatility in key materials

- 3.6.2.1.2 Supply chain restructuring

- 3.6.2.1.3 Production cost implications

- 3.6.2.2 Demand-side impact (selling price)

- 3.6.2.2.1 Price transmission to end markets

- 3.6.2.2.2 Market share dynamics

- 3.6.2.2.3 Consumer response patterns

- 3.6.2.1 Supply-side impact (raw materials)

- 3.6.3 Key companies impacted

- 3.6.4 Strategic industry responses

- 3.6.4.1 Supply chain reconfiguration

- 3.6.4.2 Pricing and product strategies

- 3.6.4.3 Policy engagement

- 3.6.5 Outlook and future considerations

- 3.6.1 Impact on trade

- 3.7 Reimbursement scenario

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Gap analysis

- 3.11 Future market trends

- 3.12 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Device, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Neurostimulation devices

- 5.2.1 Spinal cord stimulators

- 5.2.2 Deep brain stimulators

- 5.2.3 Vagus nerve stimulators

- 5.2.4 Sacral nerve stimulators

- 5.2.5 Gastric electrical stimulators

- 5.3 Neurosurgical devices

- 5.3.1 Stereotactic systems

- 5.3.2 Neuroendoscopes

- 5.3.3 Ultrasonic aspirators

- 5.3.4 Aneurysm clips

- 5.4 Interventional neurology devices

- 5.4.1 Aneurysm coiling and embolisation

- 5.4.1.1 Embolic coils

- 5.4.1.2 Flow diversion devices

- 5.4.1.3 Liquid embolic reagents

- 5.4.2 Neurothromobectomy

- 5.4.2.1 Clot retrievers

- 5.4.2.2 Suction aspiration devices

- 5.4.2.3 Snare devices

- 5.4.3 Neurovascular catheters

- 5.4.3.1 Micro catheters

- 5.4.3.2 Micro guidewires

- 5.4.4 Cerebral balloon angioplasty and stents

- 5.4.4.1 Carotid artery stents

- 5.4.4.2 Filter devices

- 5.4.4.3 Balloon occlusion devices

- 5.4.5 Csf management devices

- 5.4.5.1 Cerebral shunts

- 5.4.5.2 Cerebral external drainage

- 5.4.1 Aneurysm coiling and embolisation

- 5.5 Brain-computer interface devices

- 5.5.1 Non-invasive BCI

- 5.5.2 Partially invasive BCI

- 5.5.3 Fully invasive BCI

- 5.6 Other devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Chronic pain management

- 6.3 Parkinson’s disease

- 6.4 Epilepsy

- 6.5 Stroke management and recovery

- 6.6 Alzheimer

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 B BRAUN

- 9.3 Bioness

- 9.4 Boston Scietific

- 9.5 enterra medical

- 9.6 KARL STROZ

- 9.7 LivaNova

- 9.8 Medtronic

- 9.9 MicroTransponder

- 9.10 NeuroPace

- 9.11 nevro

- 9.12 Paradromics

- 9.13 stryker

- 9.14 synchron

- 9.15 ZYLOX TONBRIDGE