|

市場調査レポート

商品コード

1928891

繊維廃棄物リサイクル機械市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Textile Waste Recycling Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 繊維廃棄物リサイクル機械市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月07日

発行: Global Market Insights Inc.

ページ情報: 英文 272 Pages

納期: 2~3営業日

|

概要

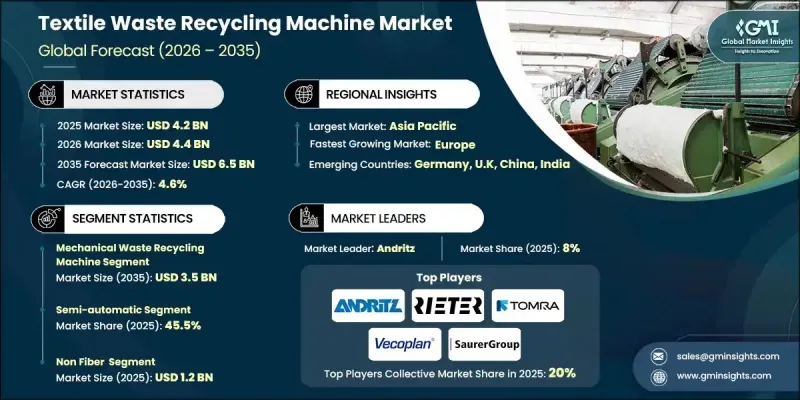

世界の繊維廃棄物リサイクル機械市場は、2025年に42億米ドルと評価され、2035年までにCAGR 4.6%で成長し、65億米ドルに達すると予測されています。

この成長は、繊維製品の消費と廃棄に関する環境意識の高まり、および持続可能な製造慣行に対する規制支援の強化によって牽引されています。産業では廃棄物の最小化と材料回収率の向上に注力する傾向が強まっており、廃棄された繊維製品を再利用可能な繊維形態に変換する機械の需要を加速させています。埋立依存度の低減と資源効率の向上を目指す官民セクターの取り組みも、市場拡大をさらに後押ししています。メーカーはこれに対応し、処理能力の向上、環境負荷の低減、循環型経済の目標に沿ったリサイクル技術の進歩に取り組んでいます。また、消費後および消費前の廃棄物を責任を持って管理するよう繊維生産者に求められる圧力の高まりも、業界にとって追い風となっています。アパレルおよび産業用繊維セクター全体で持続可能性が中核的な運営要件となる中、先進的なリサイクル機械への投資は増加を続けており、先進国と新興国双方における長期的な市場の安定性と着実な普及を支えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 42億米ドル |

| 予測金額 | 65億米ドル |

| CAGR | 4.6% |

機械式リサイクル機械セグメントは、2025年に23億米ドルの市場規模を生み出し、2035年までに35億米ドルに達すると予測されています。このセグメントは、コスト効率と低いエネルギー要件により、繊維廃棄物リサイクル機械市場の基幹を成し続けています。機械式システムは幅広い繊維廃棄物ストリームを処理できるため、実用的で拡張性のあるリサイクルソリューションを求める製造業者にとって好ましい選択肢となっています。

半自動機械セグメントは2025年に45.5%のシェアを占めました。このセグメントは、手頃な価格と操作性のバランスが取れていることから市場をリードしています。半自動システムでは、オペレーターが主要なリサイクル工程を管理しながら反復的な機能を自動化できるため、完全自動化設備に伴う高額な投資を必要とせずに労働集約度を低減できます。

米国繊維廃棄物リサイクル機械市場は2025年に90.5%のシェアを占めました。地域的な成長は、繊維廃棄物削減への政府の重点的な取り組み、国家リサイクル戦略の策定、リサイクルインフラの改善を促進する新たな立法措置によって支えられています。これらの取り組みが、大規模な繊維リサイクル機械への投資拡大を牽引しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 持続可能で環境に優しい素材への需要の高まり

- リサイクル技術の進歩

- 繊維廃棄物に関する政府規制と政策

- 業界の潜在的リスク&課題

- 初期投資額および機械コストの高さ

- 高い保守コストと運用コスト

- 機会

- 持続可能性政策と循環型経済の推進

- IoTと予知保全ソリューションの統合

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 機種別

- 地域別

- 規制情勢

- 規格およびコンプライアンス要件

- 地域別規制枠組み

- 認証基準

- 貿易統計(HSコード8445)

- 主要輸入国

- 主要輸出国

- ギャップ分析

- リスク評価と軽減策

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:機種別、2022-2035

- 機械式リサイクル装置

- 化学的リサイクル機械

- 熱リサイクル機械

第6章 市場推計・予測:素材タイプ別、2022-2035

- 綿

- ポリエステル

- ナイロン

- ウール

- その他

第7章 市場推計・予測:事業別、2022-2035

- マニュアル

- 半自動式

- 自動

第8章 市場推計・予測:容量別、2022-2035

- 1,000 kg/hまで

- 2,000 kg/hまで

- 3000 kg/hまで

- 3000 kg/h以上

第9章 市場推計・予測:用途別、2022-2035

- ファイバー間リサイクル

- 非繊維用途

- アパレル製造

- ホームテキスタイル

- テクニカルテキスタイル

第10章 市場推計・予測:調達方法別、2022-2035

- 消費前廃棄物

- 使用済み廃棄物

第11章 市場推計・予測:流通チャネル別、2022-2035

- 直接販売

- 間接

第12章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第13章 企業プロファイル

- Andritz

- Autefa Solutions

- Balkan Textile Machinery

- Dell'Orco &Villani

- HSN Machinery

- Loptex

- Margasa Projects and Textile Engineering

- Masias Machinery

- Multipro

- Rieter

- SN Surgicare and Healthcare Science

- Starlinger

- Saurer Group

- TOMRA Systems

- Vecoplan