|

市場調査レポート

商品コード

1750623

スパイダーリフトの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Spider Lift Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| スパイダーリフトの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月09日

発行: Global Market Insights Inc.

ページ情報: 英文 190 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

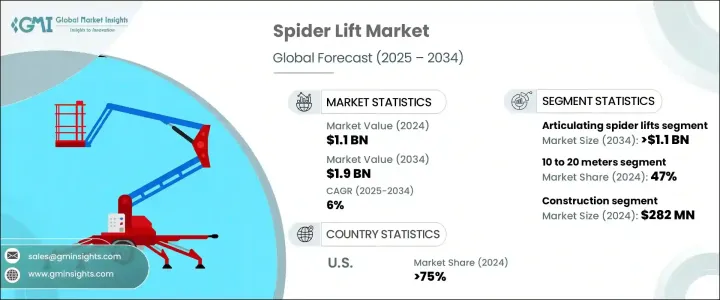

スパイダーリフトの世界市場は、2024年には11億米ドルと評価され、IoT統合、テレマティクス、自動化などの急速な技術進歩により、CAGR 6%で成長し、2034年には19億米ドルに達すると推定されています。

これらの技術革新により、リアルタイムの追跡、予知保全、操作の簡素化が可能になり、効率と安全性が向上します。環境規制がますます厳しくなり、都市部や屋内用途での低排出ガス機器の必要性が高まっていることに影響され、ハイブリッドと電気設計の機運が高まっています。

建設プロジェクトがより高いアクセス高さを必要とする中、より長いリーチのスパイダーリフトは、産業が複雑な環境において昇降と安定性の両方を提供するソリューションを求めるにつれ、需要が顕著に増加しています。これらのリフトは現在、特に高層ビルの保守点検、外装工事、ユーティリティの設置において、従来型アクセス機器では不十分な大規模プロジェクトで重要な役割を担っています。より長いリーチのスパイダーリフトは、狭い場所や届きにくい場所でも作動できるため、今日の現場には不可欠です。これらのニーズに応えるため、メーカーは安全性や操作性を損なうことなく、より大きなリーチを提供する頑丈で柔軟なリフトモデルの設計に注力しています。進化する規制状況に対応するため、各社は荷重感知技術、自動制御、高度テレマティクスのような機能を含む、インテリジェント安全性とモニタリングシステムを統合しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 11億米ドル |

| 予測金額 | 19億米ドル |

| CAGR | 6% |

関節式スパイダーリフト部門は51%のシェアを占め、2034年までに11億米ドルの価値を生み出すと予測されています。狭い空間を移動し、起伏のある地形に適応する能力は、困難な環境での関連性を高めています。メーカーが独自の用途ニーズを満たすためにモデルを改良し続けているため、メンテナンス、設置、都市ユーティリティプロジェクトで需要が急増しています。その柔軟なアームと正確な操縦性は、アクセスが制限された場所でのプロジェクトに特に適しており、その可搬性は現場での効率的な展開を可能にします。

プラットフォームの高さが10~20メートルのスパイダーリフトは、リーチと移動性のバランスの取れたニーズにより、2024年には47%のシェアを占めました。この高さ範囲は、造園、軽建設、公共施設のメンテナンスなどの作業に理想的な使い勝手を記載しています。滑り止めプラットフォーム、緊急降下システム、自動過負荷保護などの強化された安全機能が標準になりつつあり、密集した環境や交通量の多い環境でも、オペレーターがより自信を持って作業できるようになっています。職場の安全に関する規制が厳しくなるにつれ、これらの機能は必須要件になりつつあります。

米国のスパイダーリフト 2024年の市場規模は3億3,380万米ドルで、75%のシェアを占めます。急速な産業開拓、商業建設の急増、インフラのアップグレードへの投資の増加がその要因です。連邦政府や州レベルでの持続可能性の推進により、現場での排出がゼロで、敏感な場所や屋内でより静かに作動する電気式やハイブリッド式スパイダーリフトへのシフトが加速しています。北米では、都市がより厳しい排出基準や騒音規制を実施しているため、請負業者やレンタル会社はバッテリー駆動やハイブリッドユニットに目を向けています。

産業を形成する主要参入企業は、CTE SpA、Dinolift、Platform Basket、Cela、Shandong Toros Machinery Corporation、Oshkosh Corporation、Terex、Niftylift、Imer、Hubei Goman Heavy Industry Technologyなどです。主要企業は戦略的パートナーシップと製品革新を優先しています。多くの企業が研究開発に多額の投資を行い、先進的制御システムを備えた軽量でコンパクトなエコフレンドリーモデルを設計しています。地域の販売網やディーラーとの提携を通じた世界の拡大は、新興市場の開拓に役立っています。各社はまた、アフターセールスサービスを強化し、レンタル事業者や大規模フリート事業者に対応するため、柔軟なリース・ファイナンスオプションを提供しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 原料と部品サプライヤー

- 技術プロバイダ

- 製造業者

- 販売代理店

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 産業への影響

- 供給側の影響(原料)

- 主要原料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原料)

- 戦略的な産業対応

- サプライチェーンの再構成

- 貿易への影響

- 価格設定と製品戦略

- 技術とイノベーションの情勢

- 自動化とロボット工学

- エコフレンドリー電力システム

- IoTとテレマティクスの統合

- 先進的制御システムと安全機構

- 特許分析

- 規制情勢

- ユースケース

- 主要ニュースと取り組み

- コスト内訳分析

- 初回購入

- メンテナンスと修理

- 運用コスト

- 輸送

- 減価償却

- 価格動向分析

- 製品

- 地域

- 規制情勢

- 影響要因

- 促進要因

- 建設インフラプロジェクトにおける高所作業車の需要増加

- 技術の進歩と安全機能の向上

- 労働者の安全規制に対する意識の高まり

- レンタル機器の需要増加

- 産業の潜在的リスク・課題

- 初期投資と維持費が高め

- 規制遵守と安全基準

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推定・予測:製品別、2021~2034年

- 主要動向

- 伸縮式スパイダーリフト

- 関節式スパイダーリフト

- クローラー式スパイダーリフト

- 電動またはハイブリッドスパイダーリフト

第6章 市場推定・予測:プラットフォームの高さ別、2021~2034年

- 主要動向

- 10メートル以下

- 10~20メートル

- 20~25メートル

- 25メートル以上

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 政府

- 通信・公益事業

- 工業と製造業

- 施設管理会社

- レンタル

- エンターテインメントとメディア制作

第8章 市場推定・予測:地域別、2021~2034年

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Airo

- Almac

- Cela

- CMC Lift

- CTE

- Dinolift

- Easy Lift

- Falcon Lift

- HINOWA

- Imer

- JLG Industries

- Niftylift

- Omme Lift

- Palazzani Industrie

- Platform Basket

- SHANDONG HIMOR MACHINERY

- Socageworld

- Teejan Equipment

- Terex Corporation

- Teupen

The Global Spider Lift Market was valued at USD 1.1 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 1.9 billion by 2034, driven by rapid technological advancements, including IoT integration, telematics, and automation. These innovations allow for better real-time tracking, predictive maintenance, and simplified operation, improving efficiency and safety. There is a growing momentum around hybrid and electric spider lift designs, influenced by increasingly stringent environmental regulations and the need for low-emission equipment in urban and indoor applications.

With construction projects requiring heights of greater access, longer-reach spider lifts are seeing a noticeable rise in demand as industries seek solutions that offer both elevation and stability in complex environments. These lifts are now a critical part of large-scale projects where conventional access equipment falls short, especially in high-rise maintenance, exterior building work, and utility installation. The ability of longer-reach spider lifts to operate in confined or difficult-to-reach areas makes them indispensable for today's modern job sites. In response to these needs, manufacturers focus on engineering robust and flexible lift models that offer greater reach without compromising safety or ease of operation. To meet the evolving regulatory landscape, companies are integrating intelligent safety and monitoring systems, including features like load-sensing technology, automated controls, and advanced telematics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $1.9 Billion |

| CAGR | 6% |

Articulating spider lifts segment held 51% share and is projected to generate USD 1.1 billion in value by 2034, favored by their compact design, lightweight build, and versatility across industries. Their ability to navigate narrow spaces and adapt to uneven terrain has increased their relevance in challenging environments. As manufacturers continue to refine models to meet unique application needs, demand has surged across maintenance, installation, and urban utility projects. Their flexible arms and precise maneuverability make them especially suitable for projects in areas with limited access, while their portability enables efficient deployment across sites.

Spider lifts with platform heights ranging from 10 to 20 meters held a 47% share in 2024, driven by the balanced need for reach and mobility. This height range offers ideal usability for tasks across landscaping, light construction, and public facility maintenance. Enhanced safety features such as anti-slip platforms, emergency descent systems, and automatic overload protection are becoming standard, helping operators work more confidently in dense or high-traffic environments. With stricter regulations around workplace safety, these features are becoming essential requirements.

United States Spider Lift Market generated USD 333.8 million, accounting for a 75% share in 2024, driven by rapid industrial development, a surge in commercial construction, and increased investments in infrastructure upgrades. The push for sustainability across federal and state levels accelerates the shift toward electric and hybrid spider lifts, which produce zero on-site emissions and operate more quietly in sensitive or indoor areas. In North America, contractors and rental companies turn to battery-powered or hybrid units as cities enforce stricter emissions standards and noise restrictions.

Key players shaping the industry include CTE SpA, Dinolift, Platform Basket, Cela, Shandong Toros Machinery Corporation, Oshkosh Corporation, Terex, Niftylift, Imer, and Hubei Goman Heavy Industry Technology. Leading companies are prioritizing strategic partnerships and product innovation. Many invest heavily in R&D to design lightweight, compact, eco-friendly models with advanced control systems. Global expansion through regional distribution networks and dealer partnerships is helping them tap into emerging markets. Companies are also enhancing after-sales services and offering flexible leasing and financing options to cater to rental businesses and large fleet operators.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material and component suppliers

- 3.1.1.2 Technology providers

- 3.1.1.3 Manufactures

- 3.1.1.4 Distributors

- 3.1.1.5 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.1 Impact on trade

- 3.3 Pricing and product strategies

- 3.4 Technology & innovation landscape

- 3.4.1 Automation and robotics

- 3.4.2 Eco-Friendly power systems

- 3.4.3 Integration of IoT and telematics

- 3.4.4 Advanced control systems and safety mechanisms

- 3.5 Patent analysis

- 3.6 Regulatory landscape

- 3.7 Use cases

- 3.8 Key news & initiatives

- 3.9 Cost break-down analysis

- 3.9.1 Initial purchase

- 3.9.2 Maintenance & repairs

- 3.9.3 Operational costs

- 3.9.4 Transportation

- 3.9.5 Depreciation

- 3.10 Price trend analysis

- 3.10.1 Product

- 3.10.2 Region

- 3.11 Regulatory landscape

- 3.12 Impact on forces

- 3.12.1 Growth drivers

- 3.12.1.1 Rising demand for aerial work platforms in construction and infrastructure projects

- 3.12.1.2 Technological advancements and improved safety features

- 3.12.1.3 Growing awareness of worker safety regulations

- 3.12.1.4 Growing demand for rental equipment

- 3.12.2 Industry pitfalls & challenges

- 3.12.2.1 High initial investment and maintenance costs

- 3.12.2.2 Regulatory compliance and safety standards

- 3.12.1 Growth drivers

- 3.13 Growth potential analysis

- 3.14 Porter's analysis

- 3.15 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Telescopic spider lifts

- 5.3 Articulating spider lifts

- 5.4 Crawler-based spider lifts

- 5.5 Electric or hybrid spider lifts

Chapter 6 Market Estimates & Forecast, By Platform Height, 2021 - 2034 ($Mn Units)

- 6.1 Key trends

- 6.2 Below 10 meters

- 6.3 10 to 20 meters

- 6.4 20 to 25 meters

- 6.5 Above 25 meters

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Government

- 7.3 Telecommunications & utility

- 7.4 Industrial and manufacturing firms

- 7.5 Facility management companies

- 7.6 Rental

- 7.7 Entertainment & media production

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 8.1 North America

- 8.1.1 U.S.

- 8.1.2 Canada

- 8.2 Europe

- 8.2.1 UK

- 8.2.2 Germany

- 8.2.3 France

- 8.2.4 Italy

- 8.2.5 Spain

- 8.2.6 Russia

- 8.3 Asia Pacific

- 8.3.1 China

- 8.3.2 India

- 8.3.3 Japan

- 8.3.4 Australia

- 8.3.5 South Korea

- 8.3.6 Southeast Asia

- 8.4 Latin America

- 8.4.1 Brazil

- 8.4.2 Mexico

- 8.4.3 Argentina

- 8.5 MEA

- 8.5.1 South Africa

- 8.5.2 Saudi Arabia

- 8.5.3 UAE

Chapter 9 Company Profiles

- 9.1 Airo

- 9.2 Almac

- 9.3 Cela

- 9.4 CMC Lift

- 9.5 CTE

- 9.6 Dinolift

- 9.7 Easy Lift

- 9.8 Falcon Lift

- 9.9 HINOWA

- 9.10 Imer

- 9.11 JLG Industries

- 9.12 Niftylift

- 9.13 Omme Lift

- 9.14 Palazzani Industrie

- 9.15 Platform Basket

- 9.16 SHANDONG HIMOR MACHINERY

- 9.17 Socageworld

- 9.18 Teejan Equipment

- 9.19 Terex Corporation

- 9.20 Teupen