外科用スネア市場機会と促進要因、業界動向分析、2025年~2034年予測

Surgical Snares Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750614

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

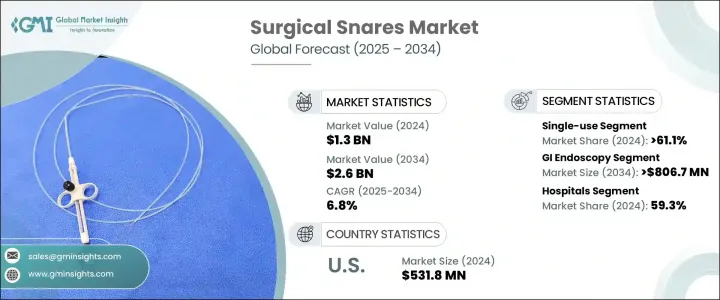

外科用スネアの世界市場は、2024年には13億米ドルと評価され、消化器疾患の増加、低侵襲処置への嗜好の高まり、内視鏡技術の進歩、世界のヘルスケア支出の増加により、CAGR 6.8%で成長し、2034年には26億米ドルに達すると予測されています。

急速な高齢化と最新のヘルスケアツールへのアクセスの向上が、外科用スネアの需要増加にさらに貢献しています。ヘルスケアシステムがより効率的で低リスクの手術ソリューションに重点を置く中、これらの器具は世界中の医療施設で内視鏡用途にますます不可欠になってきています。

外科用スネアは、軟質なワイヤループとして設計されており、異常組織や異物を除去するための様々な内視鏡治療で使用される重要なツールです。これらの器具は、大腸内視鏡検査や気管支内視鏡検査などの処置に広く利用されており、ポリープや異常組織、異物の安全な除去を可能にすることで、診断と治療の両方の機能をサポートしています。侵襲的な手術を行うことなく正確な切除を行うことができるため、回復時間を短縮し、患者の不快感を最小限に抑えることができ、外来患者や低侵襲治療の現場で高い価値を発揮しています。外科用スネアは、最新の内視鏡プラットフォームとシームレスに統合できるように設計されており、処置中の視認性、コントロール、精度の向上を可能にします。外科用スネアは、最新の内視鏡プラットフォームとシームレスに統合できるように設計されており、手術中の視認性、操作性、正確性を向上させることができます。ヘルスケアプロバイダが先進的内視鏡ツールを採用するようになるにつれ、外科用スネアは様々な臨床環境において、消化器疾患や肺疾患の管理に欠かせないものとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 13億米ドル |

| 予測金額 | 26億米ドル |

| CAGR | 6.8% |

2024年、使い捨てセグメントが61.1%のシェアで市場を牽引。使い捨てスネアは、汚染リスクの低減、手術効率の向上、費用対効果などの利点により、市場で強い支持を得ています。これらのすぐに使用できる滅菌済み器具は、滅菌インフラへの依存を減らし、医療器具の再利用に伴うリスクを排除します。さらに、規制機関や安全機関は、院内感染を最小限に抑えるため、使い捨て医療器具を重視しています。この嗜好の変化は、特に大量でリスクの高い手術環境において顕著です。

病院セグメントは、複雑な消化管症例を管理するための先進的外科手術能力に対するニーズの高まりによって、2024年には59.3%のシェアを占めました。病院は通常、より優れたインフラと最先端技術へのアクセスを提供するため、外科用スネアの主要な消費者となっています。特に、ポリープ切除や組織切除を伴う手技での使用率が高いです。さらに、病院での内視鏡処置に保険が適用されることも、これらの機器の幅広い普及を支えています。

米国の外科用スネア市場は2024年に5億3,180万米ドルに達しました。低侵襲技術の普及と効率的で高精度な手術器具への需要の高まりが背景にあります。同国のヘルスケアセグメントでは、回復時間、手術精度、患者の快適性が重視されており、外科用スネアは内視鏡検査や腹腔鏡検査に不可欠なものとなっています。先進的な手術センターが整備され、患者の意識も高まっていることから、これらの器具に対する需要は引き続き高まっています。

外科用スネア世界市場の主要企業には、Olympus、Cook、ConMed、Teleflex、Merit Medical Systems、Hill-Rom Holdings、Avalign Technologies、Medtronic、STERIS、EndoMed Systems、Boston Scientific Corporation、Aspen Surgical、GPC Medical、Medline、Sklar Surgical Instrumentsなどがあります。市場での地位を強化するため、各社は人間工学に基づいた設計や切削精度の向上に重点を置き、製品革新に投資しています。医療機関との戦略的提携は、メーカーが特定の手術ニーズに合わせてカスタマイズ型ソリューションを開発するのに役立っています。また、買収によってポートフォリオを拡大し、先端材料に投資して機器の安全性と性能を高めている企業も多いです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 産業考察

- エコシステム分析

- 産業への影響要因

- 促進要因

- 慢性疾患の有病率の増加

- 内視鏡検査の急増

- 大腸がん検診の認知度向上

- 低侵襲手術への関心の高まり

- 産業の潜在的リスク・課題

- スネアの使用に伴う臨床的合併症

- 促進要因

- 成長可能性分析

- 規制情勢

- 米国

- 欧州

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 産業への影響

- 供給側の影響(原料)

- 主要原料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原料)

- 影響を受ける主要企業

- 戦略的な産業対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 施策関与

- 展望と今後の検討事項

- 貿易への影響

- 技術

- 価格分析、 2024

- 償還シナリオ

- 応用の可能性

- ギャップ分析

- ポーター分析

- PESTEL分析

- 将来の市場動向

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推定・予測:使用性別、2021~2034年

- 主要動向

- 使い捨て

- 再利用可能

第6章 市場推定・予測:用途別、2021~2034年

- 主要動向

- 消化管内視鏡検査

- 腹腔鏡検査

- 膀胱鏡検査

- 関節鏡検査

- 気管支鏡検査

- 婦人科内視鏡検査

- その他

第7章 市場推定・予測:最終用途別、2021~2034年

- 主要動向

- 病院

- 外来手術センター

- その他

第8章 市場推定・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- aspen surgical

- Avalign Technologies

- Boston Scientific Corporation

- ConMed

- Cook

- EndoMed Systems

- GPC Medical

- Hill-Rom Holdings

- Medline

- Medtronic

- Merit Medical Systems

- Olympus

- Sklar Surgical Instruments

- STERIS

- Teleflex

目次

The Global Surgical Snares Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 2.6 billion by 2034 due to an increase in gastrointestinal disorders, growing preference for minimally invasive procedures, advancements in endoscopic technologies, and rising global healthcare spending. A rapidly aging population and improved access to modern healthcare tools further contribute to the rising demand for surgical snares. With healthcare systems focusing on more efficient, lower-risk surgical solutions, these instruments are becoming increasingly vital in endoscopic applications across medical facilities worldwide.

Surgical snares, designed as flexible wire loops, are critical tools used during various endoscopic interventions to remove abnormal tissue or foreign bodies. These devices are widely utilized in procedures such as colonoscopy and bronchoscopy, supporting both diagnostic and therapeutic functions by enabling the safe removal of polyps, abnormal tissues, and foreign objects. Their ability to perform precise excisions without invasive surgery reduces recovery time and minimizes patient discomfort, making them highly valuable in outpatient and minimally invasive settings. Surgical snares are designed to seamlessly integrate with modern endoscopic platforms, allowing for improved visibility, control, and accuracy during procedures. This compatibility not only enhances procedural efficiency but also reduces complications and improves patient outcomes. As healthcare providers increasingly adopt advanced endoscopic tools, surgical snares have become indispensable in managing gastrointestinal and pulmonary conditions across various clinical environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 6.8% |

In 2024, the single-use segment led the market with a share of 61.1%. Disposable snares are gaining strong market traction due to benefits such as reduced contamination risk, improved surgical efficiency, and cost-effectiveness. These ready-to-use, pre-sterilized tools reduce reliance on sterilization infrastructure and eliminate risks associated with reusing medical instruments. Additionally, regulatory agencies and safety bodies emphasize disposable medical tools to minimize hospital-acquired infections. This shift in preference is especially significant in high-volume and high-risk surgical environments.

The hospital segment held a 59.3% share in 2024, driven by the growing need for advanced surgical capabilities to manage complex gastrointestinal cases. Hospitals typically offer better infrastructure and access to cutting-edge technologies, making them primary consumers of surgical snares. Their usage is particularly high in procedures involving polypectomy and tissue resection. Moreover, insurance coverage for hospital-based endoscopic procedures supports broader adoption of these devices.

United States Surgical Snares Market reached USD 531.8 million in 2024, driven by the widespread adoption of minimally invasive technologies and growing demand for efficient, high-precision surgical tools. The healthcare sector in the country emphasizes recovery time, surgical accuracy, and patient comfort, making surgical snares essential in endoscopy and laparoscopy. Availability of advanced surgical centers and increased patient awareness continue to push demand for these instruments.

Leading companies in the Global Surgical Snares Market include Olympus, Cook, ConMed, Teleflex, Merit Medical Systems, Hill-Rom Holdings, Avalign Technologies, Medtronic, STERIS, EndoMed Systems, Boston Scientific Corporation, Aspen Surgical, GPC Medical, Medline, and Sklar Surgical Instruments. To reinforce market position, companies are investing in product innovation, focusing on ergonomic designs and enhanced cutting precision. Strategic collaborations with healthcare institutions help manufacturers develop customized solutions tailored to specific surgical needs. Many are expanding their portfolios through acquisitions and investing in advanced materials to enhance device safety and performance.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic conditions

- 3.2.1.2 Surging number of endoscopies

- 3.2.1.3 Increasing awareness of colorectal cancer screening

- 3.2.1.4 Rising preference for minimally invasive surgeries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Clinical complications involved in the usage of snares

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Pricing analysis, 2024

- 3.8 Reimbursement scenario

- 3.9 Application potential

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Future market trends

- 3.14 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Single-use

- 5.3 Reusable

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 GI endoscopy

- 6.3 Laparoscopy

- 6.4 Cystoscopy

- 6.5 Arthroscopy

- 6.6 Bronchoscopy

- 6.7 Gynecology endoscopy

- 6.8 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 aspen surgical

- 9.2 Avalign Technologies

- 9.3 Boston Scientific Corporation

- 9.4 ConMed

- 9.5 Cook

- 9.6 EndoMed Systems

- 9.7 GPC Medical

- 9.8 Hill-Rom Holdings

- 9.9 Medline

- 9.10 Medtronic

- 9.11 Merit Medical Systems

- 9.12 Olympus

- 9.13 Sklar Surgical Instruments

- 9.14 STERIS

- 9.15 Teleflex

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 90 Pages

- 納期

- 2~3営業日