|

|

市場調査レポート

商品コード

1750598

AIOps市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測AIOps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| AIOps市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年05月14日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

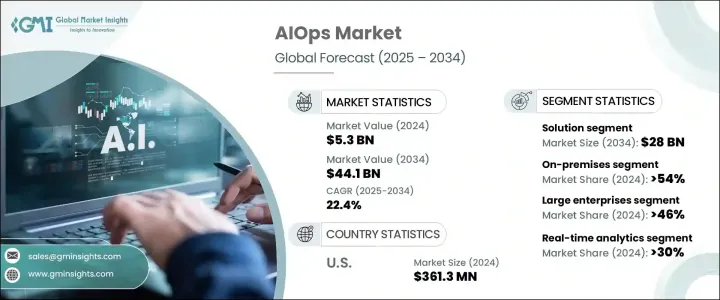

AIOpsの世界市場規模は、2024年に53億米ドルとなり、2034年にはCAGR 22.4%で成長し441億米ドルに達すると推定されています。

これは、企業のITエコシステムの複雑性の高まりと、インフラストラクチャのパフォーマンスを管理するための自動化に対する緊急の需要に後押しされています。企業はシステムのダウンタイムを減らし、インシデント解決を加速し、運用上のボトルネックをリアルタイムで可視化するために、AI主導のプラットフォームを採用しています。IT・通信、ヘルスケア、小売、銀行などのセクターでデジタルトランスフォーメーションが激化する中、AIOpsプラットフォームは、スケーラブルで俊敏なITフレームワークを管理するための中心的存在となっています。

このテクノロジーは、人工知能と機械学習およびビッグデータ機能を統合し、IT運用を継続的に監視、分析、改善します。ハイブリッド環境とマルチクラウド環境を展開する企業は、膨大な遠隔測定データとイベントデータを生成します。これにより、企業は混乱を予測し、依存関係を追跡し、分散システム全体のパフォーマンス監視を合理化することができます。イベントを相関させ、異常を検出し、根本原因をリアルタイムに突き止める能力により、AIOpsはアップタイムとオペレーションの継続性を維持するために不可欠なものとなりました。ITスタックの分散化が進むにつれ、予測的な洞察と自律的な対応を可能にするインテリジェントなプラットフォームへのニーズが急速に高まっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 53億米ドル |

| 予測金額 | 441億米ドル |

| CAGR | 22.4% |

ソリューション分野は2024年に60%のシェアを占め、2034年には280億米ドルに達すると予測されます。企業は、手作業を減らし、アプリケーション管理、インシデント解決、ログ分析などの自動化をサポートする拡張性の高いAIOpsプラットフォームを優先しています。これらのAIを搭載したツールは、ハイブリッド、オンプレミス、クラウドベースの環境に導入されることが増えており、一元的な観測可能性と運用の透明性を提供しています。複雑さと人的ミスを最小限に抑えながら、進化するインフラ需要に適応する俊敏なプラットフォームの展開が重視されています。ソリューション提供の優位性は、互換性、拡張性、およびハイレベルなパフォーマンス課題にリアルタイムで対処する能力によってもたらされます。

2024年のシェアは、オンプレミス型が54%で市場をリードしています。機密性の高いワークロードを扱う企業、特に防衛、ヘルスケア、金融などの分野では、データ保護、コンプライアンス遵守、レガシーシステムとの統合のため、自社内でのセットアップが好まれます。また、オンプレミスに設置することで、レイテンシーが低くなり、ITインフラを完全に制御できるようになります。このような利点から、規制が厳しく、ミッション・クリティカルな業務を行う企業にとって、ローカルの導入は引き続き好ましい選択肢となっています。

米国の市場情勢は、最先端のIT環境とAI技術の早期導入により、2024年に3億6,130万米ドルを創出。堅牢なデジタルインフラと、Datadog、Elastic、IBM、Cisco、Dynatraceのような技術大手による高いイノベーションレベルが組み合わされ、高度なAIOps展開に適したエコシステムが構築されています。アジャイルフレームワーク、DevOpsの採用、ハイブリッドIT環境の台頭は、米国企業全体のインテリジェントな自動化とリアルタイムの意思決定に対する需要を促進しています。

AIOps市場の主要企業が採用する主な戦略には、競争力を確保するための絶え間ないプラットフォームの革新、戦略的買収、AIモデルの改良が含まれます。BigPanda、Moogsoft、Digitate、Aisera、Broadcomなどの企業は、クラウドネイティブシステムやハイブリッドシステムとシームレスに統合する製品ポートフォリオの拡大に多額の投資を行っています。強力なパートナーエコシステムの構築、マルチドメイン可視性の強化、既存のITワークフローへのリアルタイムアナリティクスの組み込みは、これらの企業が企業採用を促進し、進化する情勢におけるリーダーシップを確固たるものにするのに役立ちます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- テクノロジープロバイダー

- OEMメーカー

- 販売代理店

- 最終用途

- 利益率分析

- サプライヤーの情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 主なニュースと取り組み

- 規制情勢

- ユースケース

- 影響要因

- 促進要因

- クラウドインフラの普及

- IT運用におけるAIベースのサービスに対する需要の高まり

- 現代のITインフラストラクチャによって生成されるデータ量の増加

- 各国におけるAI導入に向けた政府の取り組み

- 業界の潜在的リスク&課題

- データセキュリティとプライバシーに関する懸念

- IT運用における変更の増加

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ソリューション

- サービス

第6章 市場推計・予測:展開モデル別、2021年~2034年

- 主要動向

- オンプレミス

- クラウド

第7章 市場推計・予測:企業規模別、2021年~2034年

- 主要動向

- 大企業

- 中小企業

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- インフラ管理

- リアルタイム分析

- ネットワークとセキュリティ管理

- アプリケーションパフォーマンス管理

- その他

第9章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- BFSI

- ITおよび通信

- ヘルスケア

- 小売り

- 政府

- 製造業

- メディア&エンターテイメント

- その他

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第11章 企業プロファイル

- Aisera

- Amelia(IPsoft)

- Bigpanda

- BMC Software

- Broadcom CA

- Cisco

- Datadog

- Devo

- Digital.ai

- Digitate

- Dynatrace

- Elastic

- Espressive

- Extrahop

- harness

- IBM

- Interlink Software

- kentik

- Logz.io

- Moogsoft

The Global AIOps Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 22.4% to reach USD 44.1 billion by 2034, fueled by the rising complexity of enterprise IT ecosystems and the urgent demand for automation in managing infrastructure performance. Businesses adopt AI-driven platforms to reduce system downtime, accelerate incident resolution, and gain real-time visibility into operational bottlenecks. As digital transformation intensifies across sectors like telecommunications, healthcare, retail, and banking, AIOps platforms become central to managing scalable and agile IT frameworks.

Technology integrates artificial intelligence with machine learning and big data capabilities to continuously monitor, analyze, and improve IT operations. Enterprises deploying hybrid and multi-cloud environments generate vast telemetry and event data, which AIOps solutions can process and interpret quickly. This empowers organizations to forecast disruptions, trace dependencies, and streamline performance monitoring across distributed systems. The ability to correlate events, detect anomalies, and pinpoint root causes in real time has made AIOps indispensable for maintaining uptime and operational continuity. As IT stacks become more decentralized, the need for intelligent platforms that enable predictive insights and autonomous responses is rapidly accelerating.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $44.1 Billion |

| CAGR | 22.4% |

The solutions segment held a 60% share in 2024 and is projected to reach USD 28 billion by 2034. Businesses prioritize scalable AIOps platforms that reduce manual intervention and support automation across application management, incident resolution, and log analysis. These AI-powered tools are increasingly deployed across hybrid, on-premises, and cloud-based environments, offering centralized observability and operational transparency. The emphasis is on deploying agile platforms that adapt to evolving infrastructure demands while minimizing complexity and human error. The dominance of solution offerings is driven by their compatibility, scalability, and ability to address high-level performance challenges in real time.

The on-premises deployment model led the market with a 54% share in 2024. Enterprises dealing with sensitive workloads, particularly in sectors like defense, healthcare, and finance, prefer in-house setups for data protection, compliance adherence, and integration with legacy systems. On-premises installations also allow lower latency and provide organizations with total control over IT infrastructure. These advantages continue to make local deployments a preferred choice for companies with strict regulatory obligations and mission-critical operations.

U.S. AIOps Market generated USD 361.3 million in 2024, due to its cutting-edge IT landscape and early adoption of AI technologies. Robust digital infrastructure, combined with high innovation levels from tech giants like Datadog, Elastic, IBM, Cisco, and Dynatrace, has created an ecosystem primed for advanced AIOps deployment. The rise of agile frameworks, DevOps adoption, and hybrid IT environments fuels demand for intelligent automation and real-time decision-making across U.S. enterprises.

Key strategies adopted by major players in the AIOps Market include constant platform innovation, strategic acquisitions, and AI model refinement to ensure a competitive edge. Companies like BigPanda, Moogsoft, Digitate, Aisera, and Broadcom are investing heavily in expanding product portfolios that integrate seamlessly with cloud-native and hybrid systems. Building strong partner ecosystems, enhancing multi-domain visibility, and embedding real-time analytics into existing IT workflows help these companies drive enterprise adoption and solidify their leadership in the evolving AIOps landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Technology providers

- 3.1.1.2 OEM Manufacturers

- 3.1.1.3 Distributors

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Trade impact

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (Cost to customers)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook & future considerations

- 3.2.1 Trade impact

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Use cases

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Proliferation of cloud infrastructure

- 3.8.1.2 Growing demand for AI-based services in IT operations

- 3.8.1.3 Increasing volume of data generated by modern IT infrastructures

- 3.8.1.4 Government initiatives for AI adoption in various countries

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Data security and privacy concerns

- 3.8.2.2 Increasing number of changes in IT operations

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.3 Service

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 SME

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Infrastructure management

- 8.3 Real-time analytics

- 8.4 Network & security management

- 8.5 Application performance management

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 BFSI

- 9.3 IT & telecom

- 9.4 Healthcare

- 9.5 Retail

- 9.6 Government

- 9.7 Manufacturing

- 9.8 Media & entertainment

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisera

- 11.2 Amelia (IPsoft)

- 11.3 Bigpanda

- 11.4 BMC Software

- 11.5 Broadcom CA

- 11.6 Cisco

- 11.7 Datadog

- 11.8 Devo

- 11.9 Digital.ai

- 11.10 Digitate

- 11.11 Dynatrace

- 11.12 Elastic

- 11.13 Espressive

- 11.14 Extrahop

- 11.15 harness

- 11.16 IBM

- 11.17 Interlink Software

- 11.18 kentik

- 11.19 Logz.io

- 11.20 Moogsoft