|

市場調査レポート

商品コード

1750590

パーキンソン病治療薬市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Parkinson's Disease Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| パーキンソン病治療薬市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年05月12日

発行: Global Market Insights Inc.

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

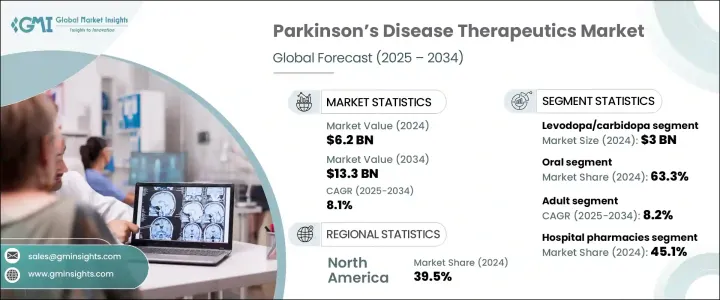

世界のパーキンソン病治療薬市場は、2024年には62億米ドルと評価され、2034年にはCAGR 8.1%で成長し、133億米ドルに達すると推定されます。

平均寿命が延びるにつれて、パーキンソン病のような加齢に伴う神経変性疾患の有病率は急速に拡大しています。北米、欧州、アジア太平洋地域の一部の国々では高齢者人口が顕著に増加しており、より効果的な治療法への需要が高まっています。ヘルスケアシステムは、治療法の革新を優先し、パーキンソン病患者に合わせた専門的治療へのアクセスを拡大することで対応しています。

医薬品の進歩が続く中、市場は大きな変革期を迎えています。従来の治療法が依然として広く使用されている一方で、より的を絞った症状コントロールを提供する代替治療への注目が高まっています。異なる神経経路を標的とする薬剤クラス別が、疾患の進行をより効果的に管理するために研究されています。革新的なデリバリー・プラットフォームも影響を及ぼしています。これには、患者のアドヒアランスを向上させるユーザーフレンドリーなシステム、特に長期的なケアが必要な患者向けのシステムなどがあります。経皮システム、吸入ルート、輸液療法は、合併症が少なく、安定的に制御された薬物送達が可能なため、人気が高いです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 62億米ドル |

| 予測金額 | 133億米ドル |

| CAGR | 8.1% |

レボドパ/カルビドパは、2024年に30億米ドルを生み出しました。レボドパ/カルビドパ製剤が優位を保ち続けているのは、さまざまな運動症状に対応できることによる。徐放性・持続性製剤の改良により合併症が減少し、一貫した症状管理が可能になりました。この薬剤は広く使用されており、価格も手ごろで、臨床効果も確立されているため、高所得国や新興国におけるパーキンソン病治療の要となっています。

2024年の経口薬のシェアは63.3%。その使いやすさ、費用対効果、入手のしやすさから、生涯治療を受ける患者にとって好ましい治療法となっています。最も処方されているパーキンソン病治療薬、特に運動症状の緩和のための治療薬の多くは経口剤で開発されています。このことは、服薬アドヒアランスを向上させるだけでなく、病院での投与の必要性を制限し、経口薬を治療の主流にしています。

米国パーキンソン病治療薬2024年の市場規模は23億米ドル。強固なヘルスケアシステム、先進的な薬事規制、最先端治療への早期アクセスなどが、パーキンソン病治療における米国のリーダーシップに貢献しています。また、強力な患者支援ネットワークと共同研究開発努力の恩恵もあり、創薬が促進され、新規治療法の商業化が加速しています。

この業界では、Teva Pharmaceutical, Newron Pharmaceuticals, UCB, Sumitomo Dainippon Pharma, F. Hoffmann-La Roche, Kyowa Kirin, Orion Pharma, Boehringer Ingelheim, Supernus Pharmaceuticals, AbbVie, Amneal Pharmaceuticals, Novartis, Desitin Arzneimittel, Acorda Therapeutics (Merz Therapeutics), Acadia Pharmaceuticalsなどが有力なプレーヤーです。パーキンソン病治療薬市場での地位を強化するため、各社はより優れた安全性と有効性を持つ次世代治療薬を開発するための戦略的研究開発投資を重視しています。また、承認取得を早め、早期に市場に参入するために、薬事指定を追求しています。学術機関やバイオテクノロジー企業との提携により、イノベーション・パイプラインの多様化が可能になります。世界な販売網、特に新興国における販売網を拡大することで、より多くの医薬品を確保することができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 人口の高齢化によりパーキンソン病の世界の有病率が上昇

- ドラッグデリバリー技術と新規製剤の進歩

- バイオ医薬品企業による研究開発投資の増加

- 非営利団体や支援団体からの強力な支援

- 業界の潜在的リスク&課題

- 先進治療の高額な費用と低所得地域での限られた償還

- 治療法の不足と現在の薬の持続的な副作用

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 疫学の情勢

- 将来の市場動向

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:薬剤クラス別、2021年~2034年

- 主要動向

- レボドパ/カルビドパ

- ドーパミン作動薬

- アデノシンA2A拮抗薬

- COMT阻害剤

- MAO-B阻害剤

- グルタミン酸拮抗薬

- コリンエステラーゼ阻害剤

- その他の薬剤クラス

第6章 市場推計・予測:投与経路別、2021年~2034年

- 主要動向

- 経口

- 経皮

- 皮下

- その他の投与経路

第7章 市場推計・予測:患者別、2021年~2034年

- 主要動向

- 成人

- 小児

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 病院薬局

- 小売薬局

- オンライン薬局

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- AbbVie

- Acadia Pharmaceuticals

- Acorda Therapeutics(Merz Therapeutics)

- Amneal Pharmaceuticals

- Boehringer Ingelheim

- Desitin Arzneimittel

- F. Hoffmann-La Roche

- Kyowa Kirin

- Newron Pharmaceuticals

- Novartis

- Orion Pharma

- Sumitomo Dainippon Pharma

- Supernus Pharmaceuticals

- Teva Pharmaceutical

- UCB

The Global Parkinson's Disease Therapeutics Market was valued at USD 6.2 billion in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 13.3 billion by 2034, driven by the increasing incidence of Parkinson's disease, particularly among aging populations worldwide. As life expectancy improves, the prevalence of age-related neurodegenerative conditions like Parkinson's is expanding rapidly. Countries across North America, Europe, and parts of the Asia-Pacific region are witnessing a notable rise in the elderly demographic, which is fueling demand for more effective treatments. Healthcare systems are responding by prioritizing therapeutic innovations and expanding access to specialized care tailored to patients with Parkinson's disease.

The market is experiencing significant transformation as pharmaceutical advancements continue to emerge. While traditional therapies remain widely used, there's increasing attention on alternative treatments that provide more targeted symptom control. Drug classes targeting different neural pathways are being explored to manage disease progression more effectively. Innovative delivery platforms are also making an impact. These include user-friendly systems that improve patient adherence, especially for individuals requiring long-term care. Transdermal systems, inhalation routes, and infusion therapies are popular due to their ability to deliver steady, controlled medication with fewer complications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.2 Billion |

| Forecast Value | $13.3 Billion |

| CAGR | 8.1% |

The Levodopa/carbidopa generated USD 3 billion in 2024. Its continued dominance is attributed to its ability to address varied motor symptoms. Enhanced formulations offering extended release and continuous delivery have helped reduce complications and provide consistent symptom management. This drug's widespread use, affordability, and established clinical efficacy make it a cornerstone in Parkinson's treatment across high-income and emerging economies.

Oral medications accounted for a 63.3% share in 2024. Their ease of use, cost-effectiveness, and availability make them the preferred route for patients undergoing lifelong treatment. Many of the most prescribed Parkinson's therapies, particularly those for motor symptom relief, are developed in oral formulations. This not only improves adherence but also limits the need for hospital-based administration, making oral drugs a dominant force in the therapeutic landscape.

U.S. Parkinson's Disease Therapeutics Market generated USD 2.3 billion in 2024. Its robust healthcare system, advanced regulatory pathways, and early access to cutting-edge treatments contribute to its leadership in Parkinson's care. The country also benefits from strong patient support networks and collaborative R&D efforts, which promote drug discovery and accelerate the commercialization of novel therapies.

Prominent players in this industry include Teva Pharmaceutical, Newron Pharmaceuticals, UCB, Sumitomo Dainippon Pharma, F. Hoffmann-La Roche, Kyowa Kirin, Orion Pharma, Boehringer Ingelheim, Supernus Pharmaceuticals, AbbVie, Amneal Pharmaceuticals, Novartis, Desitin Arzneimittel, Acorda Therapeutics (Merz Therapeutics), and Acadia Pharmaceuticals. To strengthen their position in the Parkinson's disease therapeutics market, companies emphasize strategic R&D investments to develop next-generation therapies with better safety and efficacy. They pursue regulatory designations to accelerate approvals and gain early market access. Collaborations with academic institutions and biotech firms allow for diversified innovation pipelines. Expanding global distribution networks, especially in emerging economies, ensures wider medications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global prevalence of Parkinson’s disease due to an aging population

- 3.2.1.2 Advancements in drug delivery technologies and novel formulations

- 3.2.1.3 Growing research and development investments by biopharmaceutical companies

- 3.2.1.4 Strong support from non-profits and advocacy organizations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced therapies and limited reimbursement in low income regions

- 3.2.2.2 Lack of curative treatments and persistent side effects of current medications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Epidemiology landscape

- 3.7 Future market trends

- 3.8 Pipeline analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Levodopa/carbidopa

- 5.3 Dopamine agonists

- 5.4 Adenosine A2A antagonists

- 5.5 COMT inhibitors

- 5.6 MAO-B inhibitors

- 5.7 Glutamate antagonists

- 5.8 Cholinesterase inhibitors

- 5.9 Other drug classes

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Transdermal

- 6.4 Subcutaneous

- 6.5 Other routes of administration

Chapter 7 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Adult

- 7.3 Pediatric

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AbbVie

- 10.2 Acadia Pharmaceuticals

- 10.3 Acorda Therapeutics (Merz Therapeutics)

- 10.4 Amneal Pharmaceuticals

- 10.5 Boehringer Ingelheim

- 10.6 Desitin Arzneimittel

- 10.7 F. Hoffmann-La Roche

- 10.8 Kyowa Kirin

- 10.9 Newron Pharmaceuticals

- 10.10 Novartis

- 10.11 Orion Pharma

- 10.12 Sumitomo Dainippon Pharma

- 10.13 Supernus Pharmaceuticals

- 10.14 Teva Pharmaceutical

- 10.15 UCB