燃料電池の市場機会、成長促進要因、産業動向分析、予測、2025年~2034年

Fuel Cell Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 205 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750577

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

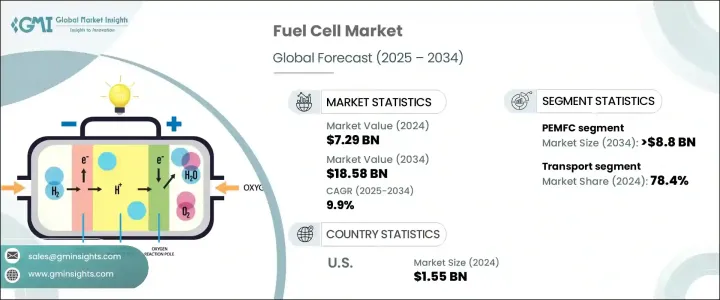

世界の燃料電池市場の2024年の市場規模は72億9,000万米ドルで、クリーンで信頼性が高く効率的な電源へのニーズが高まり続けていることから、CAGR 9.9%で成長し、2034年には185億8,000万米ドルに達すると推定されています。

この成長の原動力となっているのは、遠隔地や非電化地域での電力需要の増加と、排出量削減を目的とした環境規制の強化です。産業界が持続可能性とコスト効率の高い電力ソリューションに重点を移す中、燃料電池が有望な代替手段として浮上しています。これらのシステムは、高い運転効率、環境への影響の低さ、従来技術に比べ競争力のある価格設定により、特に魅力的です。

燃料電池は、無停電電源供給と低排出ソリューションが重要な製造部門で広く採用されています。公害を最小限に抑えながら電力を生産できる燃料電池は、政府や民間企業の注目を集めています。二酸化炭素排出量の削減とエネルギー効率の改善に焦点を当てた政策を展開する国が増える中、さまざまな用途での燃料電池の利用は着実に拡大しています。金融機関や政府機関は、この分野での技術進歩を推進するため、研究開発に多額の投資を行っています。技術革新が進むにつれて、燃料電池は商業用と住宅用の両方のエネルギーシステムでますます実用的になると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 72億9,000万米ドル |

| 予測金額 | 185億8,000万米ドル |

| CAGR | 9.9% |

官民両部門からの投資も市場の成長に寄与しています。世界中の組織が、燃料電池の性能、効率、価格を向上させる先進技術の開発への取り組みを強化しています。こうした取り組みにより、さまざまな業界の企業がエネルギー転換戦略の一環として燃料電池システムを採用するようになっています。こうした開発を受けて、次世代燃料電池システムの需要は急速に伸びています。

さまざまな種類の燃料電池の中でも、固体高分子形燃料電池(PEMFC)分野は2034年までに88億米ドルを超えると予想されています。これらの燃料電池は、動作温度が低く、起動時間が短いことで知られており、バックアップ電源ソリューションからポータブルエネルギーシステム、自動車用まで、さまざまな用途に最適です。これらの技術が進化し信頼性が高まるにつれ、データセンター、住宅、モバイルインフラなどの分野での利用が大幅に増加すると予想されます。

アプリケーションの観点から、市場は据置型、ポータブル、輸送分野に分類されます。2024年の市場は、輸送分野が全体の78.4%以上を占め、圧倒的なシェアを占めています。この分野では、電動バイク、無人航空機、商用車への燃料電池システムの採用が加速しています。運輸部門では、排出ガスの削減やより環境に優しい技術への移行にますます注目が集まっており、水素燃料電池システムの統合を後押ししています。水素の生産と流通のインフラが改善されるにつれて、海上ロジスティクスや商業船舶を含む様々な輸送用途へのこれらのシステムの展開が拡大すると予想されます。

米国が主導する北米の燃料電池市場も着実な成長を遂げています。米国市場だけでも、2022年に15億2,000万米ドル超、2023年に15億3,000万米ドルを記録し、2024年には15億5,000万米ドルに達しました。大陸全体では、市場は2034年までCAGR6%以上で成長すると予測されています。統合型メタン改質技術を利用したオンサイト水素生成ステーションの開発により、燃料供給インフラに費用対効果の高いソリューションが提供され、地域的な普及を後押ししています。こうした進歩により、公共部門と民間部門の両方において燃料電池の普及に有利な環境が整いつつあります。

世界の燃料電池市場は現在、イノベーションとコラボレーションを通じて市場での地位強化に継続的に取り組んでいる複数の主要企業の存在によって形成されています。Cummins, Ballard Power Systems, Fuji Electric, Toshiba Corporation, Plug Power-collectivelyの上位5社は、合計で世界市場シェアの約40%を占めています。これらの企業の戦略には、エネルギー企業、自動車メーカー、研究機関と提携を結び、製品ラインナップを充実させ、技術開発を加速させることが含まれます。このような協力関係により、燃料電池技術の利用範囲が拡大し、商業化への新たな道が開かれつつあります。

戦略的パートナーシップ、ジョイントベンチャー、政府および民間団体からの資金提供の増加により、研究開発のペースが加速しています。このような努力はイノベーションを促進するだけでなく、燃料電池ソリューションのスケーラビリティと市場対応力を向上させています。その結果、業界は大規模展開の実現に近づきつつあり、世界のエネルギー情勢に大きな影響を与えています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア

- 戦略的取り組み

- 戦略的ダッシュボード

- 企業ベンチマーク

- イノベーションとテクノロジーの情勢

第5章 燃料電池市場:製品別、2021年~2034年

- 主要動向

- PEMFC

- DMFC

- SOFC

- PAFC・AFC

- MCFC

第6章 燃料電池市場:アプリケーション別、2021年~2034年

- 主要動向

- 定置型

- 200kW未満

- 200kW~1MW

- 1MW以上

- ポータブル

- 輸送

- 船舶

- 鉄道

- FCEV

- その他

第7章 燃料電池市場:燃料別、2021年~2034年

- 主要動向

- 水素

- アンモニア

- メタノール

- 炭化水素

第8章 燃料電池市場:サイズ別、2021年~2034年

- 主要動向

- 小

- 大

第9章 燃料電池市場:最終用途別、2021年~2034年

- 主要動向

- 住宅

- 商業・工業

- データセンター

- 軍事・防衛

- ユーティリティ・政府

- 輸送

第10章 燃料電池市場:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オーストリア

- アジア太平洋地域

- 日本

- 韓国

- 中国

- インド

- フィリピン

- ベトナム

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ラテンアメリカ

- ブラジル

- ペルー

- メキシコ

第11章 企業プロファイル

- Cummins

- Ballard Power Systems

- Plug Power

- Nuvera Fuel Cells

- Nedstack Fuel Cell Technology

- Bloom Energy

- Panasonic Corporation

- Doosan Fuel Cell

- Aisin Corporation

- Ceres

- SFC Energy

- Toshiba Corporation

- Robert Bosch

- TW Horizon Fuel Cell Technologies

- AFC Energy

- FuelCell Energy

- Fuji Electric

- Hyundai Motor Company

目次

The Global Fuel Cell Market was valued at USD 7.29 billion in 2024 and is estimated to grow at a CAGR of 9.9% to reach USD 18.58 billion by 2034 as the need for clean, reliable, and efficient power sources continues to grow. This growth is being driven by an increasing demand for power in remote and off-grid locations, as well as by tightening environmental regulations aimed at reducing emissions. As industries shift their focus toward sustainability and cost-effective power solutions, fuel cells are emerging as a promising alternative. These systems are particularly attractive due to their high operational efficiency, lower environmental impact, and competitive pricing compared to conventional technologies.

Fuel cells are being widely adopted in the manufacturing sector, where uninterrupted power supply and low-emission solutions are critical. Their capability to produce electricity with minimal pollution has drawn the attention of governments and private players alike. With a growing number of countries rolling out policies focused on reducing carbon footprints and improving energy efficiency, the use of fuel cells across a range of applications is expanding steadily. Financial institutions and government bodies are pouring significant investments into research and development to drive technological advancements in this space. As innovation progresses, fuel cells are expected to become increasingly viable for both commercial and residential energy systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.29 Billion |

| Forecast Value | $18.58 Billion |

| CAGR | 9.9% |

Investments from both public and private sectors are also contributing to the growth of the market. Organizations across the globe are stepping up efforts to develop advanced technologies that improve the performance, efficiency, and affordability of fuel cells. These initiatives are encouraging companies across multiple industries to adopt fuel cell systems as part of their energy transition strategies. In response to these developments, the demand for next-generation fuel cell systems is growing rapidly.

Among the various types of fuel cells, the Proton Exchange Membrane Fuel Cell (PEMFC) segment is expected to surpass USD 8.8 billion by 2034. These fuel cells are known for their low operating temperature and quick startup times, making them ideal for a variety of applications, from backup power solutions to portable energy systems and automotive uses. As these technologies evolve and become more reliable, their use in sectors such as data centers, residential buildings, and mobile infrastructure is anticipated to increase significantly.

In terms of application, the market is categorized into stationary, portable, and transport sectors. The transport segment dominated the market in 2024, accounting for more than 78.4% of the total share. This segment is witnessing accelerated adoption of fuel cell systems in electric bikes, unmanned aerial vehicles, and commercial fleets. The transportation sector's increasing focus on reducing emissions and transitioning to greener technologies is propelling the integration of hydrogen fuel cell systems. As infrastructure for hydrogen production and distribution improves, the deployment of these systems across various transport applications, including maritime logistics and commercial shipping, is expected to expand.

The North American fuel cell market, led by the United States, is also witnessing steady progress. The US market alone recorded a value of over USD 1.52 billion in 2022, USD 1.53 billion in 2023, and reached USD 1.55 billion in 2024. Across the continent, the market is forecasted to grow at a CAGR of over 6% through 2034. The development of on-site hydrogen generation stations using integrated methane reforming technologies has provided cost-effective solutions for fueling infrastructure, thus boosting regional adoption. These advancements are creating a more favorable environment for the widespread deployment of fuel cells in both public and private sectors.

The global fuel cell market is currently shaped by the presence of several key players who are continuously working to strengthen their market position through innovation and collaboration. The top five companies-Cummins, Ballard Power Systems, Fuji Electric, Toshiba Corporation, and Plug Power-collectively account for around 40% of the global market share. Their strategies include forming alliances with energy companies, automotive manufacturers, and research institutions to enhance product offerings and accelerate technology development. These collaborative efforts are expanding the reach of fuel cell technology and opening new avenues for commercialization.

Strategic partnerships, joint ventures, and increased funding from both government and private entities are accelerating the pace of research and development. These efforts are not only driving innovation but also improving the scalability and market readiness of fuel cell solutions. As a result, the industry is moving closer to achieving large-scale deployment, with significant implications for the global energy landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic initiatives

- 4.4 Strategic dashboard

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Fuel Cell Market, By Product, 2021 - 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 PEMFC

- 5.3 DMFC

- 5.4 SOFC

- 5.5 PAFC & AFC

- 5.6 MCFC

Chapter 6 Fuel Cell Market, By Application, 2021 - 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 Stationary

- 6.2.1 < 200 kW

- 6.2.2 200 kW - 1 MW

- 6.2.3 ≥ 1 MW

- 6.3 Portable

- 6.4 Transport

- 6.4.1 Marine

- 6.4.2 Railways

- 6.4.3 FCEVs

- 6.4.4 Others

Chapter 7 Fuel Cell Market, By Fuel, 2021 - 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 Hydrogen

- 7.3 Ammonia

- 7.4 Methanol

- 7.5 Hydrocarbons

Chapter 8 Fuel Cell Market, By Size, 2021 - 2034 (USD Million & MW)

- 8.1 Key trends

- 8.2 Small scale

- 8.3 Large scale

Chapter 9 Fuel Cell Market, By End Use, 2021 - 2034 (USD Million & MW)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial & industrial

- 9.4 Data centers

- 9.5 Military and defense

- 9.6 Utilities & government

- 9.7 Transportation

Chapter 10 Fuel Cell Market, By Region, 2021 - 2034 (USD Million & MW)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Austria

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 South Korea

- 10.4.3 China

- 10.4.4 India

- 10.4.5 Philippines

- 10.4.6 Vietnam

- 10.5 Middle East & Africa

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Peru

- 10.6.3 Mexico

Chapter 11 Company Profiles

- 11.1 Cummins

- 11.2 Ballard Power Systems

- 11.3 Plug Power

- 11.4 Nuvera Fuel Cells

- 11.5 Nedstack Fuel Cell Technology

- 11.6 Bloom Energy

- 11.7 Panasonic Corporation

- 11.8 Doosan Fuel Cell

- 11.9 Aisin Corporation

- 11.10 Ceres

- 11.11 SFC Energy

- 11.12 Toshiba Corporation

- 11.13 Robert Bosch

- 11.14 TW Horizon Fuel Cell Technologies

- 11.15 AFC Energy

- 11.16 FuelCell Energy

- 11.17 Fuji Electric

- 11.18 Hyundai Motor Company

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 205 Pages

- 納期

- 2~3営業日