|

市場調査レポート

商品コード

1750572

造影剤の市場機会、成長促進要因、産業動向分析、2025~2034年予測Contrast Media Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 造影剤の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月15日

発行: Global Market Insights Inc.

ページ情報: 英文 141 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

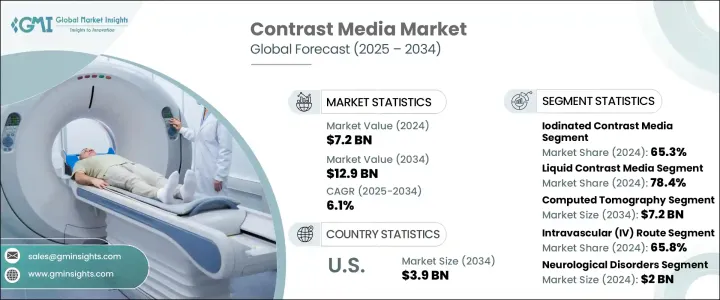

世界の造影剤市場は、2024年に72億米ドルと評価され、幅広い慢性的な健康状態を診断・管理するための医療用画像診断の需要の高まりにより、CAGR 6.1%で成長し、2034年には129億米ドルに達すると予測されています。

正確かつ早期診断の必要性が高まるにつれ、MRI、CT、X線、超音波などの画像診断技術も増加し、これらの技術は鮮明さと細部を改善するために造影剤に大きく依存しています。病院や診断センターでは、人口の増加や慢性疾患の罹患率の増加により、入院患者数、外来患者数が増加しており、これまで以上に多くの放射線検査を行っています。

造影画像は、組織、血管、臓器の微妙な異常を識別するのに有用です。これは早期発見がより効果的な治療計画につながる上で特に重要です。高度な画像処理プラットフォームの開発と人工知能の統合もまた、状況を形成しています。最新のAI駆動型放射線科プラットフォームは、正確な投与量管理とワークフローの最適化を可能にし、患者の安全性を維持しながらより良い診断結果をサポートします。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 72億米ドル |

| 予測金額 | 129億米ドル |

| CAGR | 6.1% |

2024年、ヨード造影剤が65.3%のシェアで市場を牽引しています。ヨード造影剤は、CTやX線検査に広く使用されています。その汎用性により、血管造影や尿路造影を含む複数の診断法での使用が可能です。ヨウ素の濃度はコントラストと鮮明度を高め、鮮明で正確な画像診断に不可欠です。視認性が向上することで、診断や治療計画がより確かなものとなります。ヨードベースの薬剤の特性は、標準的な画像診断で使用されるエネルギーレベルとよく一致しているため、臨床のあらゆる場面で好ましい選択肢となっています。

液体造影剤セグメントは2024年に78.4%のシェアを占めました。液体薬剤が広く使用されている主な理由は、簡単な投与方法、迅速な吸収、内部構造の効果的な可視化といった実用的な利点にあります。これらの薬剤は、速さ、正確さ、画像の鮮明さが最も重要なCTスキャンのような需要の高い診断手順で日常的に使用されています。様々な画像診断システムに適合し、血流を素早く循環させることができるため、迅速で正確な診断データを必要とする臨床医にとって、最適な選択肢となっています。救急、外来を問わず、液体造影剤の信頼性と効率性は、現代の診断ワークフローにおいて、好ましい媒体としての地位を確固たるものにしています。

米国の造影剤市場は2024年に23億米ドルに達し、2034年には39億米ドルに達すると予測されています。この増加傾向は、慢性疾患の罹患率の上昇、特にがん、心血管疾患、神経変性疾患などの疾患が定期的かつ高精度の画像診断を必要とする高齢化社会における罹患率の上昇が後押ししています。スクリーニングとモニタリングの両方でMRIとCT技術の使用が増加していることが、造影剤に対する安定した需要を後押ししています。さらに、AI主導の画像プラットフォームを含む画像技術の革新は、造影剤をより効果的にし、最適な投与とより良い画像取得を保証します。

同市場の有力企業には、TAEJOON Pharmaceutical、GE HealthCare Technologies、Livealth Biopharma、Bracco、Unijules Life Sciences、Guerbet、Trivitron Healthcare、nanoPET Pharma、Senochemia Pharmazeutika、Bayer、Jodas Expoim、J.B. Chemicals &Pharmaceuticals、Fresenius、Lantheus、iMAX Diagnostic Imagingなどがあります。市場での存在感を高めるため、主要企業は安全性を向上させた次世代造影剤の研究開発に投資しています。また、画像診断機器メーカーと戦略的提携を結び、世界的な販売網を拡大しています。いくつかの企業は、精密撮像をサポートし、造影剤投与量を削減するためのAI統合プラットフォームを模索しています。さらに、ターゲットを絞ったマーケティング、規制当局の承認、新興市場での拡大は、競争上の優位性を確保し、地域間の収益成長を後押しします。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 造影剤の規制承認の増加

- 放射線検査の増加

- 慢性疾患の発生率の急増

- 低侵襲手術の増加

- 業界の潜在的リスク・課題

- 厳しい規制と頻繁な製品リコールの存在

- 造影剤に関連するアレルギー反応と副作用

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 国別の対応

- 業界への影響

- 供給側の影響(製造コスト)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(消費者へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(製造コスト)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 技術的情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021 ~2034年

- 主要動向

- ヨード造影剤

- ガドリニウム造影剤

- マイクロバブル造影剤

- バリウム造影剤

第6章 市場推計・予測:形態別、2021 ~2034年

- 主要動向

- 液体

- 粉末

- その他

第7章 市場推計・予測:モダリティ別、2021 ~2034年

- 主要動向

- X線

- コンピュータ断層撮影(CT)

- 磁気共鳴画像法(MRI)

- 超音波

第8章 市場推計・予測:投与経路別、2021 ~2034年

- 主要動向

- 血管内経路

- 経口投与

- 直腸経路

- その他

第9章 市場推計・予測:適応症別、2021 ~2034年

- 主要動向

- 神経疾患

- がん

- 心血管疾患

- 胃腸障害

- 筋骨格系障害

- 腎臓疾患

第10章 市場推計・予測:用途別、2021 ~2034年

- 主要動向

- 放射線科

- インターベンショナルラジオロジー

- インターベンショナルカーディオロジー

第11章 市場推計・予測:最終用途別、2021 ~2034年

- 主要動向

- 病院、診療所、ASC

- 画像診断センター

第12章 市場推計・予測:地域別、2021 ~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第13章 企業プロファイル

- Bayer

- Bracco

- GE HealthCare Technologies

- Guerbet

- Fresenius

- iMAX Diagnostic Imaging

- J.B. Chemicals &Pharmaceuticals

- Jodas Expoim

- Lantheus

- Livealth Biopharma

- nanoPET Pharma

- Senochemia Pharmazeutika

- TAEJOON Pharmaceutical

- Trivitron Healthcare

- Unijules Life Sciences

The Global Contrast Media Market was valued at USD 7.2 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 12.9 billion by 2034, driven by the increased reliance on medical imaging to diagnose and manage a wide range of chronic health conditions. As the need for accurate and early diagnosis continues to rise, so do imaging techniques such as MRI, CT, X-ray, and ultrasound-all of which depend heavily on contrast agents to improve clarity and detail. Hospitals and diagnostic centers are performing more radiological procedures than ever, with inpatient and outpatient volumes increasing due to a growing population and the higher incidence of chronic illness.

Contrast-enhanced imaging is useful in identifying subtle abnormalities in tissues, blood vessels, and organs. This is especially critical in early detection leads to more effective treatment plans. The development of advanced imaging platforms and the integration of artificial intelligence are also shaping the landscape. Modern AI-driven radiology platforms enable precise dosage management and optimized workflow, supporting better diagnostic outcomes while maintaining patient safety.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.2 Billion |

| Forecast Value | $12.9 Billion |

| CAGR | 6.1% |

In 2024, iodinated contrast agents led the market with a 65.3% share. Their strong uptake is supported by widespread application in CT and X-ray procedures. Their versatility allows use across several diagnostic methods, including angiography and urography. The density of iodine enhances contrast and definition, crucial for clear and precise imaging results. This improved visibility allows for more confident diagnosis and treatment planning. The properties of iodine-based agents align well with the energy levels used in standard diagnostic imaging, making them the preferred choice across clinical settings.

The liquid contrast media segment held 78.4% share in 2024. Their widespread use is largely attributed to the practical advantages they offer-simple administration methods, rapid absorption, and effective visualization of internal structures. These agents are routinely used in high-demand diagnostic procedures like CT scans, where speed, precision, and image clarity are paramount. Their compatibility with various imaging systems and ability to quickly circulate through the bloodstream make them a go-to option for clinicians needing immediate and accurate diagnostic data. In both emergency and outpatient settings, the reliability and efficiency of liquid contrast media have solidified their position as the preferred medium in modern diagnostic workflows.

United States Contrast Media Market reached USD 2.3 billion in 2024 and is forecasted to reach USD 3.9 billion by 2034. This upward trajectory is propelled by a rise in chronic disease incidence, particularly within the aging population, where conditions like cancer, cardiovascular disease, and neurodegenerative disorders demand regular, high-precision imaging. Increasing use of MRI and CT technologies for both screening and monitoring drives steady demand for contrast-enhanced imaging agents. Additionally, innovation in imaging technologies, including AI-driven imaging platforms, makes contrast agents more effective, ensuring optimal dosing and better image acquisition.

Prominent companies in the market include TAEJOON Pharmaceutical, GE HealthCare Technologies, Livealth Biopharma, Bracco, Unijules Life Sciences, Guerbet, Trivitron Healthcare, nanoPET Pharma, Senochemia Pharmazeutika, Bayer, Jodas Expoim, J.B. Chemicals & Pharmaceuticals, Fresenius, Lantheus, and iMAX Diagnostic Imaging. To strengthen their market presence, key players are investing in R&D for next-gen contrast agents with improved safety profiles. They are also forming strategic alliances with imaging equipment manufacturers and expanding their global distribution networks. Several companies are exploring AI-integrated platforms to support precision imaging and reduce contrast dosage. Moreover, targeted marketing, regulatory approvals, and expansion in emerging markets help them secure a competitive advantage and boost revenue growth across geographies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing regulatory approvals of contrast media

- 3.2.1.2 Growth in radiological examinations

- 3.2.1.3 Surging incidence of chronic diseases

- 3.2.1.4 Increase in minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Presence of stringent regulations and frequent product recalls

- 3.2.2.2 Allergic reactions and side-effects associated with contrast media

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (cost of manufacturing)

- 3.5.2.1.1.1 Price volatility in key materials

- 3.5.2.1.1.2 Supply chain restructuring

- 3.5.2.1.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (cost to consumers)

- 3.5.2.2.1.1 Price transmission to end markets

- 3.5.2.2.1.2 Market share dynamics

- 3.5.2.2.1.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Iodinated contrast media

- 5.3 Gadolinium-based contrast media

- 5.4 Microbubble contrast media

- 5.5 Barium-based contrast media

Chapter 6 Market Estimates and Forecast, By Form, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Liquid

- 6.3 Powder

- 6.4 Other forms

Chapter 7 Market Estimates and Forecast, By Modality, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 X-ray

- 7.3 Computed tomography (CT)

- 7.4 Magnetic resonance imaging (MRI)

- 7.5 Ultrasound

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Intravascular route

- 8.3 Oral route

- 8.4 Rectal route

- 8.5 Other routes of administration

Chapter 9 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Neurological disorders

- 9.3 Cancer

- 9.4 Cardiovascular disease

- 9.5 Gastrointestinal disorders

- 9.6 Musculoskeletal disorders

- 9.7 Nephrological disorders

Chapter 10 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Radiology

- 10.3 Interventional radiology

- 10.4 Interventional cardiology

Chapter 11 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 Hospitals, clinics, and ASCs

- 11.3 Diagnostic imaging centers

Chapter 12 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 Saudi Arabia

- 12.6.2 South Africa

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Bayer

- 13.2 Bracco

- 13.3 GE HealthCare Technologies

- 13.4 Guerbet

- 13.5 Fresenius

- 13.6 iMAX Diagnostic Imaging

- 13.7 J.B. Chemicals & Pharmaceuticals

- 13.8 Jodas Expoim

- 13.9 Lantheus

- 13.10 Livealth Biopharma

- 13.11 nanoPET Pharma

- 13.12 Senochemia Pharmazeutika

- 13.13 TAEJOON Pharmaceutical

- 13.14 Trivitron Healthcare

- 13.15 Unijules Life Sciences