|

|

市場調査レポート

商品コード

1850617

ドライ真空ポンプ市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Dry Vacuum Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ドライ真空ポンプ市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2025年10月23日

発行: Global Market Insights Inc.

ページ情報: 英文 240 Pages

納期: 2~3営業日

|

概要

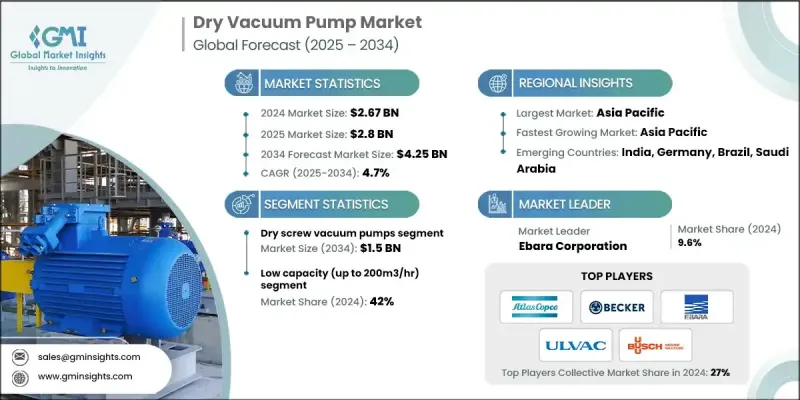

ドライ真空ポンプの世界市場は、2024年に26億7,000万米ドルと評価され、CAGR 4.7%で成長し、2034年には42億5,000万米ドルに達すると予測されています。

エレクトロニクス、航空宇宙、自動車などの産業製造の急増は、成形、コーティング、材料輸送などのプロセスにおけるドライ真空ポンプの需要を引き続き促進しています。製薬およびバイオテクノロジー産業は、滅菌、凍結乾燥、溶媒回収作業においてこれらのポンプが不可欠であることから、市場成長を後押ししています。食品および飲料分野も、真空包装や食品加工においてクリーンでオイルフリーのシステムに対する要求が高まっているため、採用を後押ししています。一方、化学メーカーは、メンテナンスが容易な設計とコンタミネーションのない操作性から、ドライ真空ソリューションを支持しています。自動化とデジタル化へのシフトが進むにつれて、メーカーは真空システムにスマート機能を統合し、リアルタイム監視、データ分析、予測メンテナンスを提供して稼働時間と効率を向上させる方向にあります。二段式システムは、より深い真空レベルを必要とするアプリケーションで人気を集めています。ドライ真空ポンプは、そのエネルギー効率、耐久性、環境に優しい操作性により、いくつかのアプリケーションでオイルベースのシステムに取って代わり、よりクリーンで信頼性の高い真空技術を求める業界全体で魅力的な選択肢となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 26億7,000万米ドル |

| 予測金額 | 42億5,000万米ドル |

| CAGR | 4.7% |

ドライスクリュー真空ポンプ分野は、半導体製造、冶金、化学生産での高い採用率に後押しされ、2034年までに15億米ドルの売上が見込まれています。ドライスクリュー真空ポンプは、コンタミのない高真空レベルと高速ポンピングを実現します。エネルギー効率の高い運転は、特に電力消費と運転経費の削減を目指す施設にとって重要な利点です。堅牢な設計と運転間隔の延長により、メンテナンスの必要性を減らし、稼働時間を向上させることができるため、大量の連続使用用途に理想的です。このセグメントの成長は、需要の高い環境において、持続可能で効率的な機器を好む傾向が強まっていることを反映しています。

低速(200m3/hrまで)セグメントは、精密でコンパクト、かつエネルギー効率の高いソリューションを必要とする用途のため、2024年には42%のシェアを占めました。このセグメントは、研究室、小規模製薬生産、分析機器、電子機器製造などで広く採用されています。ポンプの人気は、汚染防止と信頼性が重要な環境において、クリーンでオイルフリーの性能を提供できることに起因しています。コンパクトな設計、低メンテナンス、費用対効果の高い運転により、これらのポンプは限られたスペースでの設置や断続的な使用に適しています。

北米のドライ真空ポンプ市場は、2034年までに10億7,000万米ドルに達すると予測されています。製薬とバイオテクノロジーの状況は、凍結乾燥や無菌包装のようなプロセスが汚染のない環境を必要とする主要な推進力です。厳しい業界規制への対応と、この地域における生物製剤製造の拡大が、これらのシステムに対する需要を強化しています。高い生産基準、研究開発投資の増加、プロセスの完全性への強い関心は、北米の施設全体の成長を支える重要な要因です。

ドライ真空ポンプ業界を形成する主要メーカーは、Edwards Vacuum、Ebara Corporation、ULVAC、Becker Vacuum Pumps、Atlas Copco、Welch Vacuum、Agilent Technologies、Grundfos、Alfa Laval、Leybold GmbH、KNF Neuberger、Flowserve Corporation、Tuthill Corporation、DEKKER Vacuum Technologies、Graham Corporationなどです。ドライ真空ポンプをリードするメーカーは、その地位を強化するため、エネルギー効率の高い技術革新に注力し、進化する業界の需要に応えるべく製品ラインを拡大しています。その多くは、自動化機能を備えたスマートポンプシステムに投資し、ユーザーがリアルタイムの性能データや予知保全ツールにアクセスできるようにしています。また、各社は戦略的提携やパートナーシップを結び、特に高成長地域における販売網を強化しています。継続的な研究開発努力により、改良された真空レベル、より静かな運転、より長い耐用年数のポンプが開発されています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 機会

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- ポンプの種類別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- 貿易統計(HSコード841410)

- 主要輸入国

- 主要輸出国

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:ポンプタイプ別、2021-2034

- 主要動向

- ドライスクリュー真空ポンプ

- ドライスクロール真空ポンプ

- ドライダイヤフラムポンプ

- ドライクロー&フックポンプ

- その他

第6章 市場推計・予測:容量別、2021-2034

- 主要動向

- 低(最大200m3/時)

- 中(200~500 m3/時)

- 高(500 m3/時以上)

第7章 市場推計・予測:最終用途産業別、2021-2034

- 主要動向

- エレクトロニクスおよび半導体

- 医薬品

- 化学および石油化学

- 石油・ガス

- 飲食品

- その他

第8章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 直接販売

- 間接販売

第9章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Agilent Technologies

- Atlas Copco

- Becker Vacuum Pumps

- Busch Vacuum Solutions

- Ebara Corporation

- Flowserve Corporation

- Graham Corporation

- Ingersoll Rand Inc

- Kashiyama Industries

- Orion Machinery

- Osaka Vacuum

- Schmalz Group

- Shinko Seiki

- ULVAC

- Unozawa