|

市場調査レポート

商品コード

1750525

商業EaaS(Energy as a Service)市場機会、成長促進要因、産業動向分析、2025年~2034年予測Commercial Energy as a Service (EaaS) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 商業EaaS(Energy as a Service)市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月02日

発行: Global Market Insights Inc.

ページ情報: 英文 123 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

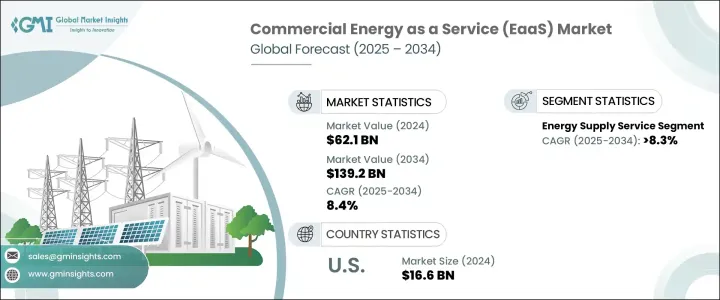

商業EaaS(Energy as a Service)の世界市場の2024年の市場規模は621億米ドルで、エネルギーコストの増加、商業ビルにおけるエネルギー負荷の変動性、持続可能なエネルギーソリューションへの需要などを背景に、CAGR 8.4%で成長し、2034年には1,392億米ドルに達すると推定されます。

企業はサービスベースのエネルギー調達に移行しており、初期資本支出を抑え、エネルギー管理を強化できるため、さまざまな商業業界でEaaSの採用が広がっています。さらに、再生可能エネルギー発電、エネルギー効率の向上、長期的な節約を含む大規模なパートナーシップが、市場の拡大を加速させています。

企業が持続可能性をますます優先するようになるにつれ、効率的で環境に優しいエネルギー・ソリューションの採用が進み、市場の成長を後押ししています。こうしたサービスモデルは、エネルギー・インフラへの先行投資を不要とする費用対効果の高い選択肢を提供するため、企業は経済的負担を負うことなく再生可能エネルギーや先進技術を利用できます。さらに、グリッド規模のバッテリー蓄電システムの導入が増加していることから、特に商業スペースにおいてEaaSの需要が高まると予想されます。暖房、冷房、輸送などさまざまな分野の電化が進んでいることも、EaaSの利用をさらに促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 621億米ドル |

| 予測金額 | 1,392億米ドル |

| CAGR | 8.4% |

エネルギー効率・最適化サービス分野は、2025年から2034年にかけてCAGR 8.7%の高成長が見込まれます。企業が二酸化炭素排出量の削減とエネルギー使用の最適化を目指す中、こうしたサービスは施設管理戦略に不可欠なものとなりつつあります。エネルギー監視ソフトウェア、インテリジェントセンサー、リアルタイムエネルギーダッシュボード、予測分析などのイノベーションにより、HVACシステム、照明、電気インフラの正確な制御とパフォーマンスの最適化が可能になります。

運用・保守(O&M)サービス分野は、現代のエネルギー・インフラの複雑化とデジタル化の進展に支えられ、2034年までに632億米ドルを創出する見通しです。商業ビルは現在、スマートメーター、オンサイト再生可能エネルギー、蓄電池、統合エネルギー管理システムを組み込んでおり、そのすべてに継続的な技術サポートとピーク性能を確保するための予知保全が付いています。IoTを活用した診断とAIベースの故障検出により、リアクティブからプロアクティブなサービスモデルへの移行が、ダウンタイムの削減と資産寿命の延長に貢献しています。

北米の商業EaaS(Energy as a Service)市場は、カーボンニュートラルへの積極的な推進と老朽化した商業インフラの近代化ニーズの高まりに支えられ、2024年には31%のシェアを占める。米国では、再生可能エネルギー発電、エネルギー貯蔵、需要側管理を統合したEaaSソリューションの採用が増加しており、有利な規制政策とクリーンエネルギー税制優遇措置に支えられています。商業消費者が余剰エネルギー容量や柔軟な負荷を収益化できる仮想発電所(VPP)の出現は、EaaSの価値提案をさらに強化し、人気を集めています。

シュナイダーエレクトリック、シーメンス、ハネウェルのような企業は、統合されたカスタマイズ可能なエネルギーソリューションの提供に注力しています。先進技術とエネルギー効率の高い製品を開発することで、持続可能な商用エネルギー・サービスに対する需要の高まりに応えています。戦略的パートナーシップや協力関係も、市場での足跡を拡大する上で重要な役割を果たしています。業界各社は、包括的なEaaSを提供するため、スマートグリッド、蓄電池、再生可能エネルギー・ソリューションへの投資を増やしています。さらに、顧客サービスモデルを強化し、より良いエネルギーパフォーマンス管理のためにデータ主導型ソリューションを採用しており、市場での存在感を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 影響要因

- さまざまなフレーバーをご用意

- 消費者意識の高まり

- ソーシャルメディアの影響力の増大

- 業界の潜在的リスク&課題

- 規制の不確実性と制限

- 若者の電子タバコ使用の蔓延と国民の反発

- 成長可能性分析

- 消費者行動分析

- 人口動向

- 購入決定に影響を与える要因

- 消費者製品の採用

- 優先流通チャネル

- 希望価格帯

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- シガライク

- ベイプペン

- 使い捨てベイプ

- ポッドベイプ

- ボックスモッド

第6章 市場推計・予測:カテゴリー別、2021-2034

- 主要動向

- オープン

- 近い

第7章 市場推計・予測:フレーバー別、2021-2034

- 主要動向

- タバコ

- 植物学

- フルーツ

- 甘い

- 飲み物

- その他

第8章 市場推計・予測:価格別、2021-2034

- 主要動向

- 低

- 中

- 高

第9章 市場推計・予測:ユーザー別、2021-2034

- 主要動向

- 男性

- 女性

第10章 市場推計・予測:動作モード別、2021-2034

- 主要動向

- マニュアル

- 自動

第11章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- オンライン

- eコマース

- 企業ウェブサイト

- オフライン

- スーパーマーケット/ハイパーマーケット

- ベイプ専門店

- コンビニエンスストアとガソリンスタンド

- その他

第12章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第13章 企業プロファイル

- Blu

- Elf Bar

- GeekVape

- Innokin

- Lost Mary

- Lost Vape

- MC

- MOK

- PAX

- Pulze

- SMOK

- Suorin

- Vaporesso

- Vuse

The Global Commercial Energy as a Service Market was valued at USD 62.1 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 139.2 billion by 2034 driven by increasing energy costs, the variability of energy loads in commercial buildings, and the demand for sustainable energy solutions. Companies are shifting to service-based energy procurement, enabling them to lower their initial capital expenditure and enhance energy management, leading to broader adoption of EaaS across various commercial industries. Additionally, large-scale partnerships involving renewable energy generation, energy efficiency upgrades, and long-term savings are accelerating market expansion.

As businesses increasingly prioritize sustainability, they are adopting energy solutions that are both efficient and environmentally friendly, fueling market growth. These service models provide cost-effective options that eliminate the need for upfront investments in energy infrastructure, enabling businesses to access renewable energy and advanced technologies without bearing all the financial burden. Moreover, the rising implementation of grid-scale battery energy storage systems is expected to increase the demand for EaaS, particularly in commercial spaces. The growing electrification of various sectors such as heating, cooling, and transportation further complements the uptake of these services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $62.1 Billion |

| Forecast Value | $139.2 Billion |

| CAGR | 8.4% |

The energy efficiency and optimization services segment is anticipated to grow at a robust CAGR of 8.7% from 2025 to 2034, driven by the increasing pressure on commercial facilities to lower operational expenses while aligning with ambitious sustainability goals. As businesses aim to reduce their carbon footprint and optimize energy use, these services are becoming integral to facility management strategies. Innovations such as energy monitoring software, intelligent sensors, real-time energy dashboards, and predictive analytics enable precise control and performance optimization of HVAC systems, lighting, and electrical infrastructure.

The operations and maintenance (O&M) services segment is poised to generate USD 63.2 billion by 2034, underpinned by the rising complexity and digitalization of modern energy infrastructure. Commercial buildings now incorporate smart meters, on-site renewables, battery storage, and integrated energy management systems, all with ongoing technical support and predictive maintenance to ensure peak performance. The shift from reactive to proactive servicing models, powered by IoT-enabled diagnostics and AI-based fault detection, is helping reduce downtime and extend asset life.

North America Commercial Energy as a Service (EaaS) Market held a 31% share in 2024, supported by the aggressive push toward carbon neutrality and the rising need to modernize aging commercial infrastructure. The U.S. is seeing increased adoption of EaaS solutions that integrate renewable generation, energy storage, and demand-side management, supported by favorable regulatory policies and clean energy tax incentives. The emergence of virtual power plants (VPPs), which enable commercial consumers to monetize excess energy capacity or flexible load, is gaining traction and further enhancing the value proposition of EaaS.

Companies like Schneider Electric, Siemens, and Honeywell focus on offering integrated, customizable energy solutions. By developing advanced technologies and energy-efficient products, they meet the growing demand for sustainable commercial energy services. Strategic partnerships and collaborations also play a crucial role in expanding their market footprint. Players in the industry are increasingly investing in smart grids, battery storage, and renewable energy solutions to offer comprehensive EaaS offerings. Furthermore, they are enhancing their customer service models and adopting data-driven solutions for better energy performance management, which helps to strengthen their presence in the market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.5 Demand-side impact (selling price)

- 3.2.2.6 Price transmission to end markets

- 3.2.2.7 Market share dynamics

- 3.2.2.8 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Impact forces

- 3.3.1 Availability of a variety of flavors

- 3.3.2 Rising consumer awareness

- 3.3.3 Increase in social media influences

- 3.4 Industry pitfalls & challenges

- 3.4.1 Regulatory uncertainty & restrictions

- 3.4.2 Youth vaping epidemic & public backlash

- 3.5 Growth potential analysis

- 3.6 Consumer behavior analysis

- 3.6.1 Demographic trends

- 3.6.2 Factors affecting buying decisions

- 3.6.3 Consumer product adoption

- 3.6.4 Preferred distribution channel

- 3.6.5 Preferred price range

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn) (Thousand Units)

- 5.1 Key trends

- 5.2 Cigalikes

- 5.3 Vape Pens

- 5.4 Disposable vapes

- 5.5 Pod vapes

- 5.6 Box mods

Chapter 6 Market Estimates & Forecast, By Category, 2021 - 2034 ($Bn) (Thousand Units)

- 6.1 Key trends

- 6.2 Open

- 6.3 Close

Chapter 7 Market Estimates & Forecast, By Flavor, 2021 - 2034 ($Bn) (Thousand Units)

- 7.1 Key trends

- 7.2 Tobacco

- 7.3 Botanical

- 7.4 Fruit

- 7.5 Sweet

- 7.6 Beverage

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Price, 2021 - 2034 ($Bn) (Thousand Units)

- 8.1 Key trends

- 8.2 Low

- 8.3 Medium

- 8.4 High

Chapter 9 Market Estimates & Forecast, By User, 2021 - 2034 ($Bn) (Thousand Units)

- 9.1 Key trends

- 9.2 Men

- 9.3 Women

Chapter 10 Market Estimates & Forecast, By Mode of Operation, 2021 - 2034 ($Bn) (Thousand Units)

- 10.1 Key trends

- 10.2 Manual

- 10.3 Automatic

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn) (Thousand Units)

- 11.1 Key trends

- 11.2 Online

- 11.2.1 E-commerce

- 11.2.2 Company website

- 11.3 Offline

- 11.3.1 Supermarkets/hypermarket

- 11.3.2 Specialty vape shops

- 11.3.3 Convenience stores and gas stations

- 11.3.4 Others

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn) (Thousand Units)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 UK

- 12.3.2 Germany

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.6 MEA

- 12.6.1 UAE

- 12.6.2 South Africa

- 12.6.3 Saudi Arabia

Chapter 13 Company Profiles

- 13.1 Blu

- 13.2 Elf Bar

- 13.3 GeekVape

- 13.4 Innokin

- 13.5 Lost Mary

- 13.6 Lost Vape

- 13.7 MC

- 13.8 MOK

- 13.9 PAX

- 13.10 Pulze

- 13.11 SMOK

- 13.12 Suorin

- 13.13 Vaporesso

- 13.14 Vuse