電気自動車用DCコンタクタの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Electric Vehicle DC Contactor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 129 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750522

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

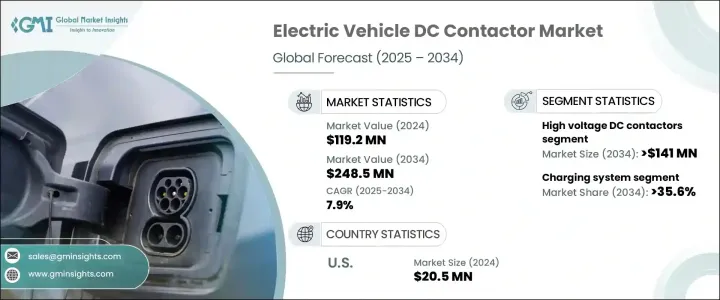

電気自動車用DCコンタクタの世界市場は、2024年には1億1,920万米ドルとなり、CAGR 7.9%で成長し、2034年には2億4,850万米ドルに達すると予測されています。

これは、世界中で電気自動車の導入が増加していることに加え、DCコンタクタ技術の継続的な進歩が市場拡大の原動力となっています。安全性、エネルギー効率、持続可能性に関する厳しい規制要件を満たしながら、車両性能を高めることに重点を置いた技術革新により、より小型で効率的かつ耐久性のあるコンタクタへの需要が高まっています。

最新の電動パワートレインと補助システムは、優れた性能を提供する高度なDCコンタクタに依存しています。これらのコンタクタは、接点の磨耗を最小限に抑えるように設計されているため、動作寿命が長く、安全性と信頼性を高める改良型アーク抑制機能を備えています。このような技術革新は、パワートレインと補助システムに高い効率性と耐久性が不可欠な電気自動車(EV)にとって非常に重要です。DCコンタクタが進化を続けることで、自動車メーカーは厳しい安全基準、エネルギー効率基準、環境基準を満たすことができ、持続可能な輸送を目指す上で不可欠な存在となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1億1,920万米ドル |

| 予測金額 | 2億4,850万米ドル |

| CAGR | 7.9% |

高電圧DCコンタクタ市場セグメントは、電動モビリティへの世界のシフトの激化に伴い、2034年までに1億4,100万米ドルに達すると予想されます。高電圧DCコンタクタは、バッテリーとその他の高電圧コンポーネント間の電気の流れを管理することで、電気自動車の安全性と信頼性を確保する上で重要な役割を果たします。高電圧・大電流コンタクタ技術の進歩により、充電速度の高速化と熱管理の改善が可能になりました。

これと並行して、電気自動車用DCコンタクタ市場のHVAC(暖房、換気、空調)アプリケーション分野では、2034年までのCAGRが7.3%と予測されています。電気自動車のエネルギー効率が高まるにつれ、信頼性の高い熱管理システムの必要性が高まっています。HVACシステムは、エネルギー消費を最小限に抑えながら電気自動車内の快適性を維持するための重要なコンポーネントです。DCコンタクタは、これらのシステムに関連する頻繁なスイッチングや変化する電流負荷を管理する上で不可欠であり、特に小型で高効率な車両設計の動向が強まるにつれて、その重要性が増しています。

米国の電気自動車用DCコンタクタ市場規模は2,050万米ドルで、電気自動車の普及台数の増加と、クリーンな輸送に対する政府の継続的な支援に後押しされています。EVの導入とグリーン技術への投資を奨励する政策により、この上昇基調は今後も続くとみられます。米国政府は、メーカーや消費者に対する税制優遇措置や助成金などのイニシアチブをとっており、これがEV産業の成長、ひいては信頼性の高いDCコンタクタの需要に拍車をかけています。また、効率、安全性、費用対効果を向上させる技術革新により、DCコンタクタの設計と製造が大きく進歩しています。

世界の電気自動車用DCコンタクタ業界の主要企業には、ABB、イートン、富士電機、三菱電機、シュナイダーエレクトリック、シーメンス、センサータテクノロジーズ、TEコネクティビティなどがあります。これらの企業は、電気自動車業界の進化するニーズを満たす最先端技術の開発によって市場を形成しています。市場での存在感を高めるため、電気自動車用DCコンタクタ市場の企業は継続的なイノベーションに注力しています。製品の効率性、安全性、耐久性を高めるための研究開発に多額の投資を行い、高性能電気自動車向けの製品の信頼性を高めています。自動車メーカー、ユーティリティ企業、充電インフラ・プロバイダーとの戦略的パートナーシップは、市場浸透率を高める鍵です。さらに、各社は新興市場でのプレゼンスを拡大しつつ、電気自動車用部品の需要増に対応するため、費用対効果の高いソリューションの提供に注力しています。持続可能でスケーラブルなソリューションを優先することで、これらの企業は、急速に進化する電気自動車業界において長期的な成長を遂げるための好位置につけています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業の市場シェア

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:電圧別、2021-2034

- 主要動向

- 高電圧(>60V)

- 低電圧(≤60V)

第6章 市場規模・予測:用途別、2021-2034

- 主要動向

- バッテリー管理システム

- インバーター

- 暖房、換気、空調(HVAC)

- 充電システム

第7章 市場規模・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- イタリア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第8章 企業プロファイル

- ABB

- Carlo Gavazzi

- Eaton

- Fuji Electric

- Geya

- L&T

- Lovato Electric

- LS Electric

- Mitsubishi Electric

- Panasonic

- Rockwell Automation

- Schaltbau

- Schmersal

- Schneider Electric

- Sensata Technologies

- Siemens

- TE Connectivity

- Toshiba

目次

The Global Electric Vehicle DC Contactor Market was valued at USD 119.2 million in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 248.5 million by 2034, driven by the increasing adoption of electric vehicles across the globe, along with continuous advancements in DC contactor technologies, is driving the market's expansion. The demand for more compact, efficient, and durable contactors is growing, with innovations focused on enhancing vehicle performance while meeting stringent regulatory requirements for safety, energy efficiency, and sustainability.

Modern electric powertrains and auxiliary systems rely on advanced DC contactors that offer superior performance. These contactors are designed with minimal contact wear, ensuring longer operational lifespans, and are equipped with improved arc suppression features that enhance safety and reliability. Such innovations are critical for electric vehicles (EVs), where high efficiency and durability are essential for the powertrain and auxiliary systems. The continued evolution of DC contactors allows automakers to meet stringent safety, energy efficiency, and environmental standards, making them an integral part of the drive toward sustainable transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $119.2 Million |

| Forecast Value | $248.5 Million |

| CAGR | 7.9% |

The high-voltage DC contactors market segment is expected to reach USD 141 million by 2034, as the global shift toward electric mobility intensifies. High-voltage DC contactors play a critical role in ensuring the safety and reliability of electric vehicles by managing the flow of electricity between the battery and other high-voltage components. Advancements in high-voltage and high-current contactor technology have enabled faster charging speeds and improved thermal management.

In parallel, the HVAC (Heating, Ventilation, and Air Conditioning) application segment within the Electric Vehicle DC Contactor Market is projected CAGR of 7.3% through 2034. With electric vehicles becoming more energy-efficient, the need for reliable thermal management systems is escalating. The HVAC system is a key component for maintaining comfort within electric vehicles while minimizing energy consumption. DC contactors are essential in managing the frequent switching and varying current loads associated with these systems, especially as the trend toward compact and high-efficiency vehicle designs intensifies.

U.S. Electric Vehicle DC Contactor Market was valued at USD 20.5 million, fueled by the rise in electric vehicle adoption and the ongoing government support for clean transportation. This upward trajectory is set to continue as policies incentivize EV adoption and investments in green technologies. The U.S. government's initiatives, such as tax incentives and grants for manufacturers and consumers, have catalyzed the growth of the EV industry and, consequently, the demand for reliable DC contactors. In addition, the country is seeing significant advancements in the design and manufacturing of DC contactors, with innovations that improve efficiency, safety, and cost-effectiveness.

Leading players in the Global Electric Vehicle DC Contactor Industry include ABB, Eaton, Fuji Electric, Mitsubishi Electric, Schneider Electric, Siemens, Sensata Technologies, and TE Connectivity. These companies are shaping the market by developing cutting-edge technologies that meet the evolving needs of the electric vehicle industry. To strengthen their market presence, companies in the electric vehicle DC contactor market focus on continuous innovation. They invest heavily in research and development to enhance product efficiency, safety, and durability, making their products more reliable for high-performance electric vehicles. Strategic partnerships with automotive manufacturers, utility companies, and charging infrastructure providers are key to increasing market penetration. Additionally, companies are focusing on offering cost-effective solutions to meet the growing demand for electric vehicle components while expanding their presence in emerging markets. By prioritizing sustainable and scalable solutions, these companies are well-positioned for long-term growth in the rapidly evolving electric vehicle industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (Raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (Raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1.1 Price transmission to end markets

- 3.2.3.1.2 Market share dynamics

- 3.2.3.1.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future Considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiative

- 4.4 Company market share

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034, (USD Million)

- 5.1 Key trends

- 5.2 High voltage (>60V)

- 5.3 Low voltage (≤60V)

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034, (USD Million)

- 6.1 Key trends

- 6.2 Battery management systems

- 6.3 Inverters

- 6.4 Heating, Ventilation, and Air conditioning (HVAC)

- 6.5 Charging systems

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034, (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Carlo Gavazzi

- 8.3 Eaton

- 8.4 Fuji Electric

- 8.5 Geya

- 8.6 L&T

- 8.7 Lovato Electric

- 8.8 LS Electric

- 8.9 Mitsubishi Electric

- 8.10 Panasonic

- 8.11 Rockwell Automation

- 8.12 Schaltbau

- 8.13 Schmersal

- 8.14 Schneider Electric

- 8.15 Sensata Technologies

- 8.16 Siemens

- 8.17 TE Connectivity

- 8.18 Toshiba

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 129 Pages

- 納期

- 2~3営業日