電気自動車用接触器の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Electric Vehicle Contactor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 138 Pages

- 納期

- 2~3営業日

- 商品コード

- 1741045

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

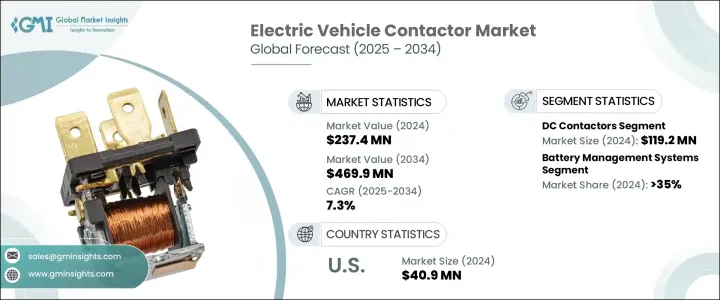

電気自動車用接触器の世界市場は、2024年には2億3,740万米ドルとなり、CAGR7.3%で成長し、2034年までには4億6,990万米ドルに達すると推定されています。

政府の奨励策や排ガス規制によって電気自動車の普及が加速し、これらの部品に対する需要が高まっています。EVメーカーは、高電圧回路を安全に管理するために堅牢なコンタクタを設置しており、車両がより厳しい環境基準に準拠できるようにしています。

コンタクターは、バッテリーと、充電ステーション、インバーター、バッテリー管理システムなど、電気自動車(EV)内の他の重要なシステムとの間の電力フローを調整する上で非常に重要です。その役割は、安全で効率的な電力管理を保証し、車両のさまざまなコンポーネントが最適に機能することを可能にします。二酸化炭素排出量削減への世界の取り組みが強化されるにつれ、電気ドライブトレインへのシフトが顕著になり、EVアプリケーションにおける信頼性の高い接触器の需要がさらに高まっています。これらのコンポーネントは、エネルギー貯蔵から配電までのシームレスな動作を保証し、世界の電気自動車の採用拡大に貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 2億3,740万米ドル |

| 予測金額 | 4億6,990万米ドル |

| CAGR | 7.3% |

DCコンタクター分野の2024年の市場規模は1億1,920万米ドルでした。これらのコンタクターは、高電圧電流を扱うように設計されており、バッテリーとパワーエレクトロニクス間のスムーズな電力フローを保証します。その設計は、極端な動作条件下でも高性能を維持することに重点を置いています。急速なスイッチングサイクルに耐え、高い耐久性を持ち、電圧損失を最小限に抑えるDCコンタクターは、安定した性能が不可欠な電気自動車に最適です。この信頼性により電気自動車の効率が向上するため、DCコンタクターは業界で不可欠な存在となっています。

バッテリー管理システム(BMS)は、電気自動車用接触器市場のもう一つの主要アプリケーションであり、2024年には35%のシェアを占めました。これらのシステムは、バッテリーの充電状態、温度、全体的な健康状態を監視・管理するもので、最適な性能を確保し、バッテリーの寿命を延ばし、過充電や過熱などの安全上の問題を防ぐために不可欠です。電気自動車が高度化するにつれて、効率的で信頼性の高いバッテリー管理システムへの需要が高まり、バッテリーと他の車両システムとのスムーズな相互作用を保証する接触器のニーズがさらに高まっています。

北米の電気自動車用接触器2024年の市場規模は4,090万米ドルとなりました。北米は、EV産業において支配的な地位を維持しており、多くの主要自動車メーカーが車両システムやEV充電インフラにおいて高電圧コンタクタに大きく依存しています。電気自動車の需要が拡大し続ける中、安全で信頼性の高い電源管理ソリューションを提供する請負業者の役割はさらに重要になり、EVエコシステムにおける重要な地位が強化されています。

世界の電気自動車用接触器市場の主要企業は、Mitsubishi Electric Corporation、Siemens, ABB、Panasonic Corporation、Rockwell Automation、Schaltbau、Schneider Electric、TE Connectivity、GEYA Electrical Equipment Supply、Eaton、Carlo Gavazzi、Fuji Electric FA Components & Systems Co., Ltd.、LS ELECTRIC、K.A. Schmersal GmbH & Co. KG、Toshiba International Corporation、Sensata Technologies, Inc.、L&T、LOVATO Electric S.p.Aが含まれています。市場ポジションを強化するため、電気自動車用接触器セクターの企業は製品イノベーションに注力しており、EV業界の高まる需要に対応するエネルギー効率、耐久性、コンパクトなコンタクタの開発に重点を置いています。また、新興市場に対応するため、世界な生産・流通ネットワークの拡大に投資しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 貿易への影響

- 展望と今後の検討事項

- 業界への影響要因

- 成長促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業の市場シェア

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- ACコンタクタ

- DCコンタクタ

第6章 市場規模・予測:電圧別、2021年~2034年

- 主要動向

- 高電圧(60V未満)

- 低電圧(60V以上)

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- バッテリー管理システム

- インバーター

- 暖房、換気、空調(HVAC)

- 充電システム

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- ABB

- Carlo Gavazzi

- Eaton

- Fuji Electric FA Components &Systems Co.、Ltd.

- GEYA Electrical Equipment Supply

- K.A. Schmersal GmbH &Co. KG

- L&T

- LOVATO Electric S.p.A.

- LS ELECTRIC

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Rockwell Automation

- Schaltbau

- Schneider Electric

- Sensata Technologies、Inc.

- Siemens

- TE Connectivity

- Toshiba International Corporation

目次

The Global Electric Vehicle Contactor Market was valued at USD 237.4 million in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 469.9 million by 2034, driven by the growing demand for electric vehicles, the need for high-voltage contactors, which are critical in managing the power safely. The increasing adoption of electric vehicles, spurred by government incentives and emission regulations, has intensified the demand for these components. EV manufacturers are installing robust contactors to ensure that high-voltage circuits are safely managed, allowing their vehicles to comply with stricter environmental standards.

Contactors are crucial in regulating the power flow between the battery and other essential systems within electric vehicles (EVs), including charging stations, inverters, and battery management systems. Their role ensures safe and efficient power management, enabling the vehicle's various components to function optimally. As global efforts to reduce carbon emissions intensify, there is a noticeable shift towards electric drivetrains, further driving the demand for reliable contactors in EV applications. These components ensure seamless operation, from energy storage to distribution, contributing to the growing adoption of electric vehicles worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $237.4 Million |

| Forecast Value | $469.9 Million |

| CAGR | 7.3% |

The DC contactor segment was valued at USD 119.2 million in 2024. These contactors are engineered to handle high-voltage currents, ensuring smooth power flow between the battery and power electronics. Their design focuses on maintaining high performance, even under extreme operating conditions. The ability to endure rapid switching cycles, high durability, and minimal voltage loss makes DC contactors ideal for EVs, where consistent performance is essential. This reliability enhances the efficiency of electric vehicles, making DC contactors indispensable in the industry.

Battery management systems (BMS) are another major application in the electric vehicle contactor market, accounting for a 35% share in 2024. These systems monitor and manage the battery's state of charge, temperature, and overall health, which is vital for ensuring optimal performance, extending battery life, and preventing safety issues like overcharging and overheating. As electric vehicles become more advanced, the demand for efficient and reliable battery management systems is rising, further increasing the need for contactors that ensure smooth interaction between the battery and other vehicle systems.

North America Electric Vehicle Contactor Market generated USD 40.9 million in 2024. North America remains a dominant player in the EV industry, with many key automakers relying heavily on high-voltage contactors in vehicle systems and EV charging infrastructure. As the demand for electric vehicles continues to expand, the role of contractors in providing safe and reliable power management solutions becomes even more critical, reinforcing their essential position in the EV ecosystem.

Key players in the Global Electric Vehicle Contactor Market include: Mitsubishi Electric Corporation, Siemens, ABB, Panasonic Corporation, Rockwell Automation, Schaltbau, Schneider Electric, TE Connectivity, GEYA Electrical Equipment Supply, Eaton, Carlo Gavazzi, Fuji Electric FA Components & Systems Co., Ltd., LS ELECTRIC, K.A. Schmersal GmbH & Co. KG, Toshiba International Corporation, Sensata Technologies, Inc., L&T, and LOVATO Electric S.p.A. To strengthen their market position, companies in the electric vehicle contactor sector are focusing on product innovation, emphasizing the development of energy-efficient, durable, and compact contactors that meet the growing demands of the EV industry. They are also investing in expanding their global production and distribution networks to cater to emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data source

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.1 Impact on trade

- 3.3 Outlook and future considerations

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiative

- 4.4 Company market share

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 AC contactor

- 5.3 DC contactor

Chapter 6 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 High voltage (>60V)

- 6.3 Low voltage (≤60V)

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Battery management systems

- 7.3 Inverters

- 7.4 Heating, Ventilation, and Air Conditioning (HVAC)

- 7.5 Charging systems

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Carlo Gavazzi

- 9.3 Eaton

- 9.4 Fuji Electric FA Components & Systems Co., Ltd.

- 9.5 GEYA Electrical Equipment Supply

- 9.6 K.A. Schmersal GmbH & Co. KG

- 9.7 L&T

- 9.8 LOVATO Electric S.p.A.

- 9.9 LS ELECTRIC

- 9.10 Mitsubishi Electric Corporation

- 9.11 Panasonic Corporation

- 9.12 Rockwell Automation

- 9.13 Schaltbau

- 9.14 Schneider Electric

- 9.15 Sensata Technologies, Inc.

- 9.16 Siemens

- 9.17 TE Connectivity

- 9.18 Toshiba International Corporation

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 138 Pages

- 納期

- 2~3営業日