|

市場調査レポート

商品コード

1750515

経カテーテル塞栓・閉塞装置の市場機会と成長促進要因、産業動向分析、2025年~2034年予測Transcatheter Embolization And Occlusion Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 経カテーテル塞栓・閉塞装置の市場機会と成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月02日

発行: Global Market Insights Inc.

ページ情報: 英文 155 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

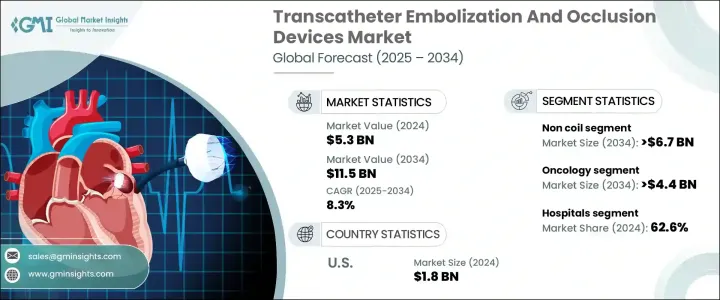

世界の経カテーテル塞栓・閉塞装置市場は、2024年には53億米ドルと評価され、2034年には115億米ドルに達するまでCAGR 8.3%で成長すると予測されています。

これは、がんなどの慢性疾患、合併症妊娠、血管奇形、血友病のような出血性疾患などの有病率の増加を含むいくつかの要因によるもので、これらはすべて専門的な医療処置を必要とします。さらに、世界の高齢化により、手術の侵襲を減らし、入院期間を短縮するQOL(生活の質)の高い手術に対する需要が高まっており、TEO装置は医師と患者の双方にとって好ましいものとなっています。

特にアジア太平洋地域では、肝臓がんや肝細胞がんの症例が増加しており、経動脈的化学塞栓療法(TACE)のような塞栓療法の使用が増加しています。カテーテル技術、医療用画像処理、生体適合性材料の進歩により、これらの手技の安全性と精度が向上し、より広範な導入が促されています。さらに、低侵襲治療の選択肢に対する意識の高まりにより、子宮筋腫塞栓術(UFE)は、従来の外科手術に代わる治療法を求める女性の間で人気の高い選択肢となっています。子宮摘出術とは異なり、UFEは子宮を温存し、回復時間を短縮し、入院期間を最小限にするため、より魅力的で患者に優しい解決策となっています。このような患者の嗜好の変化は、より多くの婦人科医やインターベンショナル・ラジオロジストに塞栓術を勧めることを促し、ひいては経カテーテル塞栓装置の採用を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 53億米ドル |

| 予測金額 | 115億米ドル |

| CAGR | 8.3% |

市場は、デバイスのタイプ別にノンコイルとコイルのカテゴリーに区分されます。非コイル・セグメントはCAGR 8.6%で成長し、2034年には67億米ドルに達すると予測されます。これは、マイクロスフィアや液体塞栓剤のような新しい塞栓剤の採用や、従来のコイルベースのデバイスと比較して閉塞時に優れた制御を提供するプラグの採用によるものです。非コイルソリューションは、肝臓がん、動静脈奇形、消化管出血、子宮筋腫の治療に用いられる標的塞栓術で特に好まれています。複雑な血管の解剖学的構造を安定した結果でナビゲートする能力により、インターベンショナル・ラジオロジストからますます支持されています。

用途別では、がん分野が事業の成長を牽引し、CAGR 8.8%で拡大し、2034年には44億米ドルに達すると予想されています。これは、がん、特に肝臓がん、腎臓がん、肺がんの世界の負担増に後押しされたもので、より局所的で侵襲性の低い治療オプションが必要とされることが多いです。肝動脈化学塞栓療法(TACE)と放射性塞栓療法は、重要なインターベンショナル・オンコロジー治療法として採用され、大きな伸びを示しています。アジア太平洋やラテンアメリカを中心に肝細胞がんの症例数が増加しており、塞栓療法の利用が拡大しています。

米国の経カテーテル塞栓・閉塞装置市場は2024年に18億米ドルを占め、2025年から2034年にかけてCAGR 7.4%で成長すると予測されています。塞栓治療デバイスの需要は、がん、消化管出血、動脈瘤、子宮筋腫などの広範な健康問題に大きく影響され、これらは低侵襲塞栓療法を用いて最適に治療されます。同国の圧倒的なヘルスケア支出は、その洗練されたヘルスケア・インフラとともに、新しいTEO手技の採用を促進しています。さらに、市場をリードするメーカーの利用可能性が高まっていること、新しく効率的な塞栓剤と送達システムに対するFDAの承認が急増していることも、市場の成長を後押ししています。

世界の経カテーテル塞栓・閉塞装置業界で事業を展開している有力企業には、Abbott、Acandis、Balt、Boston Scientific、COOK MEDICAL、Edwards Lifesciences、Johnson &Johnson、LEPU MEDICAL、Medtronic、Merit Medical、MicroVention、Penumbra、Shape Memory Medical、SIRTEX、Stryker、TERUMOなどがあります。市場ポジションを強化するため、経カテーテル塞栓・閉塞装置市場の企業はいくつかの主要戦略に注力しています。これには、医療従事者や患者の進化するニーズに応える革新的な製品を生み出すための研究開発への投資が含まれます。病院やヘルスケア機関との戦略的パートナーシップやコラボレーションは、製品の採用を促進し、市場へのリーチを拡大するために進められています。さらに各社は、より幅広い病状や用途に対応できるよう、製品ポートフォリオの拡充にも注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 低侵襲手術への移行

- インターベンショナルラジオロジーの能力向上

- 慢性疾患の有病率の上昇

- 塞栓材料の技術的進歩

- 外傷の発生率の増加

- 業界の潜在的リスク&課題

- 機器や手順の高コスト

- 非標的塞栓のリスク

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 国別の対応

- 業界への影響

- 供給側の影響(製造コスト)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(消費者のコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(製造コスト)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーの情勢

- ギャップ分析

- ポーター分析

- PESTEL分析

- バリューチェーン分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:デバイスタイプ別、2021-2034

- 主要動向

- コイルなし

- 流れ転換装置

- 塞栓粒子

- 液体塞栓

- その他の非コイルデバイスの種類

- コイル

- 押し込み可能なコイル

- 取り外し可能なコイル

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 腫瘍学

- 末梢血管疾患

- 神経学

- 泌尿器科

- その他の用途

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott

- acandis

- balt

- Boston Scientific

- COOK MEDICAL

- Edwards Lifesciences

- Johnson &Johnson

- LEPU MEDICAL

- Medtronic

- Merit Medical

- MicroVention

- Penumbra

- shape memory medical

- SIRTEX

- stryker

- TERUMO

The Global Transcatheter Embolization And Occlusion Devices Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 11.5 billion by 2034, driven by several factors, including the increasing prevalence of chronic diseases such as cancer, complicated pregnancies, vascular malformations, and hemorrhagic disorders like hemophilia, all of which require specialized medical attention. Additionally, the aging global population is leading to a higher demand for quality-of-life procedures that reduce the invasiveness of surgery and shorten hospital stays, making TEO devices favorable to both physicians and patients.

The rise in cases of liver cancer and hepatocellular carcinoma, particularly in the Asia Pacific region, has led to an increased use of embolization therapies like transarterial chemoembolization (TACE). Advancements in catheter technology, medical imaging, and biocompatible materials have improved the safety and accuracy of these procedures, encouraging more widespread adoption. Additionally, the rising awareness about minimally invasive treatment options has made uterine fibroid embolization (UFE) a popular choice among women seeking alternatives to traditional surgical procedures. Unlike hysterectomy, UFE preserves the uterus, reduces recovery time, and minimizes hospital stays, making it a more attractive and patient-friendly solution. This shift in patient preference is encouraging more gynecologists and interventional radiologists to recommend embolization techniques, which is, in turn, boosting the adoption of transcatheter embolization devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 8.3% |

The market is segmented by device type into non-coil and coil categories. The non-coil segment is expected to grow at a CAGR of 8.6%, reaching USD 6.7 billion by 2034, attributed to the adoption of new embolic agents like microspheres and liquid embolics, along with plugs that offer superior control during occlusion compared to traditional coil-based devices. Non-coil solutions are particularly preferred in targeted embolization procedures used in treating liver cancer, arteriovenous malformations, gastrointestinal bleeding, and uterine fibroids. Their ability to navigate complex vascular anatomies with consistent results has made them increasingly favored by interventional radiologists.

In terms of application, the oncology segment is expected to drive business growth, expanding at a CAGR of 8.8%, reaching USD 4.4 billion by 2034, fueled by the increasing global burden of cancer, especially liver, kidney, and lung cancers, which often require more localized and less invasive treatment options. There has been significant growth in the adoption of transarterial chemoembolization (TACE) and radioembolization as vital interventional oncology procedures. The growing caseload of hepatocellular carcinoma, predominantly in the Asia Pacific and Latin America regions, is witnessing greater use of embolization therapies.

U.S. Transcatheter Embolization And Occlusion Devices Market accounted for USD 1.8 billion in 2024 and is anticipated to grow at a CAGR of 7.4% between 2025 to 2034. Demand for embolization therapeutic devices is greatly influenced by widespread health issues such as cancer, gastrointestinal bleeding, aneurysms, and uterine fibroids, which are optimally treated using minimally invasive embolization therapies. The country's dominant healthcare spending, along with its sophisticated healthcare infrastructure, facilitates the adoption of new TEO procedures. Furthermore, the increasing availability of leading market manufacturers and a surge in FDA approvals for new and efficient embolic agents and delivery systems fuel market growth.

Prominent players operating in the Global Transcatheter Embolization And Occlusion Devices Industry include Abbott, Acandis, Balt, Boston Scientific, COOK MEDICAL, Edwards Lifesciences, Johnson & Johnson, LEPU MEDICAL, Medtronic, Merit Medical, MicroVention, Penumbra, Shape Memory Medical, SIRTEX, Stryker, and TERUMO. To strengthen their market position, companies in the transcatheter embolization and occlusion devices market are focusing on several key strategies. These include investing in research and development to create innovative products that meet the evolving needs of healthcare providers and patients. Strategic partnerships and collaborations with hospitals and healthcare institutions are being pursued to enhance product adoption and expand market reach. Additionally, companies are focusing on expanding their product portfolios to cater to a wider range of medical conditions and applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward minimally invasive procedures

- 3.2.1.2 Increasing interventional radiology capabilities

- 3.2.1.3 Rising prevalence of chronic diseases

- 3.2.1.4 Technological advancements in embolic materials

- 3.2.1.5 Increased incidence of traumatic injuries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices and procedures

- 3.2.2.2 Risk of non-target embolization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise Response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Device Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Non coil

- 5.2.1 Flow diverting devices

- 5.2.2 Embolization particles

- 5.2.3 Liquid embolics

- 5.2.4 Other non-coil device types

- 5.3 Coils

- 5.3.1 Pushable coils

- 5.3.2 Detachable coils

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oncology

- 6.3 Peripheral vascular disease

- 6.4 Neurology

- 6.5 Urology

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 acandis

- 9.3 balt

- 9.4 Boston Scientific

- 9.5 COOK MEDICAL

- 9.6 Edwards Lifesciences

- 9.7 Johnson & Johnson

- 9.8 LEPU MEDICAL

- 9.9 Medtronic

- 9.10 Merit Medical

- 9.11 MicroVention

- 9.12 Penumbra

- 9.13 shape memory medical

- 9.14 SIRTEX

- 9.15 stryker

- 9.16 TERUMO