|

市場調査レポート

商品コード

1750490

金属製クロージャーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Metal Closures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 金属製クロージャーの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月12日

発行: Global Market Insights Inc.

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

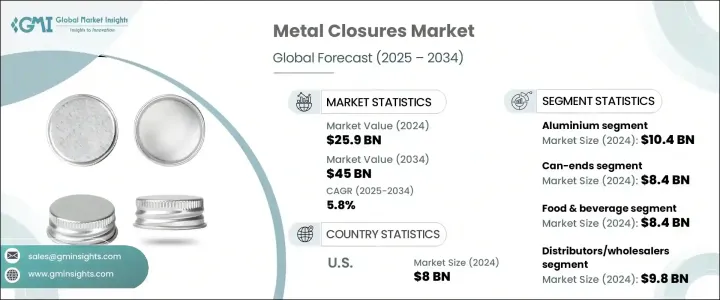

金属製クロージャーの世界市場規模は、2024年に259億米ドルとなり、CAGR5.8%で成長し、2034年までには450億米ドルに達すると推定されます。

この成長の主な原動力は、先進経済諸国と新興経済諸国の両方でアルコール飲料の消費が増加していることに加え、食品・飲料に対する需要が増加していることです。消費者のライフスタイルがより速いペースで都市化するにつれて、便利で耐久性があり、改ざんできないパッケージングソリューションに対するニーズが大幅に高まり、金属製クロージャーの採用に拍車をかけています。これらのクロージャーは、製品の完全性を保ち、賞味期限を延ばし、持続可能な包装の取り組みを支援する能力を持っているため、支持されています。近年、市場関係者は、環境に優しい機能を取り入れ、リサイクル可能な材料を優先することで、進化する規制と消費者の期待に応えています。

トランプ政権下で輸入アルミニウムと鉄鋼に関税が課されたことは、業界に大きな影響を与えました。この措置は原材料費の高騰を招き、最大で25%に達し、輸入に頼っていたメーカーに広範な混乱を引き起こしました。国内メーカーは利幅の縮小に直面し、コスト上昇分を顧客に転嫁する必要がありました。一部の地場金属メーカーは一時的な価格優位性の恩恵を受けましたが、業界全体ではボラティリティの高まりと操業費用の上昇に対処しました。こうした課題もまた、企業に調達戦略の再評価を促し、多くの企業が自動化へとシフトし、生産コストを安定させるために代替材料を模索しました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 259億米ドル |

| 予測金額 | 450億米ドル |

| CAGR | 5.8% |

材料別では、アルミニウム、スチール、スズ、その他に区分されます。2024年にはアルミセグメントが優位を占め、104億米ドル以上を生み出しました。アルミ製クロージャーは、物流経費を削減する軽量性と、信頼性の高い密封ソリューションを提供する耐久性で広く選ばれています。この材料は、耐腐食性と酸性製品への適合性で特に好まれています。循環型経済への取り組みとの整合性や、持続可能性に向けた企業のコミットメントの高まりが、さまざまな産業での採用を後押ししています。

製品タイプ別では、クラウン、缶エンド、スクリュー、ツイスト、その他のクロージャーがあります。缶エンドカテゴリーは主要セグメントとして浮上し、2024年には84億米ドルを突破しました。食品・飲料の包装に使用されることが増え、需要が大幅に加速しています。これらのクロージャーは優れた密封性能を発揮するため、鮮度維持と汚染防止に理想的です。便利なパッケージングソリューションの人気も、このセグメントの急成長に寄与しており、特に長寿命と使い勝手の良さが不可欠なセクターで顕著です。

金属製クロージャー市場は最終用途に基づき、パーソナルケア・化粧品、食品・飲料、消費財、医薬品、その他に分けられます。食品・飲料分野は2024年に84億米ドルの評価額で市場をリードしました。消費習慣の変化、すぐに食べられる食事への選好の高まり、加工食品における密閉容器の普及などが、需要を促進する上で重要な役割を果たしています。金属製クロージャーは、内容物を湿気や酸素から保護するバリア特性を提供し、特に炭酸飲料や発酵飲料の保存期間の延長と品質維持に貢献しています。

流通チャネルに関しては、市場は直販、流通業者・卸売業者、小売業者、eコマースに区分されます。流通業者・卸売業者は2024年に最も高い市場シェアを占め、98億米ドルに達しました。このセグメントの成長は、さまざまな業界のメーカーによる大量購入が、信頼できるサプライチェーンの継続性を確保していることに起因しています。これらの販売業者は、柔軟な注文サイズとカスタムオプションで中堅企業に対応することが多く、ニッチ市場や特殊包装の要件に対応することができます。

米国は2024年に80億米ドルで最大の地域シェアを占めました。同国の強固な医薬品生産インフラと厳格な安全・包装基準が、先進クロージャーシステムの採用を後押ししています。タンパーエビデントや小児用耐性を備えた金属製クロージャーは、コンプライアンスと消費者の安全のためにますます重要になってきています。また、高級パッケージ商品の人気上昇やアルコール飲料の消費量増加も需要を後押ししており、いずれも安全で効率的な密封技術を必要としています。

金属製クロージャー業界の競合は激しく、世界メーカーも地域メーカーも存在します。上位3社、Silgan Holdings Inc.、Crown Holdings Inc.、Guala Closures Groupは、2024年には合わせて12.8%以上の市場シェアを占めました。大手企業は研究開発に投資を続け、軽量材料、リサイクル性の向上、革新的な密封機構に焦点を当てた次世代製品を発表しています。QRコードやNFCチップを搭載したスマートクロージャーなどの機能は、企業が消費者の関与、トレーサビリティ、製品の安全性を高めようとしていることから、勢いを増しています。さらに、健康志向とトレーサビリティを重視するパッケージングの重要性が高まっているため、メーカーはBPA-NIライニングやハイバリア技術などの機能を備えたクロージャーの開発を促しています。また、オンライン小売、消費者直販ブランド、工芸品製造の人気が各業界で高まっていることも、機能性と美的魅力を兼ね備えたカスタマイズ可能な小ロット対応のクロージャーの必要性を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 成長促進要因

- 包装食品・飲料の需要増加

- 活況を呈する製薬業界

- アルコール飲料の消費量の増加

- 長い保存期間と密閉性

- 持続可能性とリサイクル性の魅力

- 業界の潜在的リスク・課題

- 原材料価格の変動

- 軽量フレキシブル包装への代替

- 成長促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- アルミニウム

- 鋼鉄

- 錫

- その他

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- クラウン

- 缶の端

- スクリュー

- ねじ込み

- その他

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 食品・飲料

- 医薬品

- 消費財

- パーソナルケア・化粧品

- その他

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接販売

- 販売業者/卸売業者

- 小売業者

- eコマース

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Amcor

- AptarGroup

- Berry Global

- CL Smith

- Closure Systems International

- Crown Holdings

- Finn-Korkki

- Guala Closures

- MJS Packaging

- Metal Closures

- Nippon Closures

- O. Berk

- Pelliconi

- Silgan Holdings

- Sonoco Products

- Tecnocap

The Global Metal Closures Market was valued at USD 25.9 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 45 billion by 2034. This growth is primarily driven by the increasing demand for packaged food and beverages, along with rising consumption of alcoholic drinks across both developed and emerging economies. As consumer lifestyles become more fast-paced and urbanized, the need for convenient, durable, and tamper-proof packaging solutions has grown substantially, fueling the adoption of metal closures. These closures are favored due to their ability to preserve product integrity, offer extended shelf life, and support sustainable packaging efforts. In recent years, market players have responded to evolving regulations and consumer expectations by incorporating environmentally friendly features and prioritizing recyclable materials.

The imposition of tariffs on imported aluminum and steel under the Trump administration significantly impacted the industry. These measures led to raw material cost surges-up to 25%-causing widespread disruptions for manufacturers reliant on imports. Domestic players faced tightened margins and had to pass on higher costs to customers. While some local metal producers benefited from the temporary pricing advantage, the broader industry dealt with heightened volatility and rising operational expenses. These challenges also encouraged firms to re-evaluate sourcing strategies, with many shifting towards automation and exploring alternative materials to stabilize production costs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25.9 Billion |

| Forecast Value | $45 Billion |

| CAGR | 5.8% |

By material, the market is segmented into aluminum, steel, tin, and others. The aluminum segment dominated in 2024, generating over USD 10.4 billion. Aluminum closures are widely chosen for their lightweight nature, which reduces logistics expenses, and their durability, which provides reliable sealing solutions. This material is especially favored for its resistance to corrosion and compatibility with acidic products. Its alignment with circular economy initiatives and rising corporate commitments toward sustainability are boosting its adoption across various industries.

In terms of product type, the market includes crown, can-ends, screw, twist, and other closures. The can-ends category emerged as the leading segment, surpassing USD 8.4 billion in 2024. Their increasing use in the packaging of food and beverages has significantly accelerated demand. These closures provide excellent sealing performance, making them ideal for maintaining freshness and preventing contamination. The popularity of convenient packaging solutions has also contributed to the rapid growth of this segment, especially in sectors where longevity and user-friendliness are essential.

Based on end-use, the metal closures market is divided into personal care and cosmetics, food and beverage, consumer goods, pharmaceuticals, and others. The food and beverage sector led the market in 2024 with a valuation of USD 8.4 billion. Changing consumption habits, increased preference for ready-to-eat meals, and the widespread use of airtight containers in processed food have all played a vital role in driving demand. Metal closures offer barrier properties that protect contents from moisture and oxygen, helping extend shelf life and maintain quality, especially for carbonated and fermented beverages.

Regarding distribution channels, the market is segmented into direct sales, distributors/wholesalers, retailers, and e-commerce. Distributors and wholesalers accounted for the highest market share in 2024, reaching USD 9.8 billion. The growth of this segment is attributed to bulk purchasing by manufacturers across various industries, ensuring reliable supply chain continuity. These distributors often cater to mid-sized firms with flexible order sizes and custom options, enabling them to meet the needs of niche markets and specialty packaging requirements.

The United States held the largest regional share in 2024, valued at USD 8 billion. The country's robust pharmaceutical production infrastructure, combined with stringent safety and packaging standards, has driven the adoption of advanced closure systems. Metal closures designed with tamper-evident and child-resistant features have become increasingly important for compliance and consumer safety. Demand is also being fueled by the rising popularity of premium packaged goods, along with increased consumption of alcohol-based beverages, all of which require secure and efficient sealing technologies.

Competition in the metal closures industry is intense, with the presence of both global and regional manufacturers. The top three companies- Silgan Holdings Inc., Crown Holdings Inc., and Guala Closures Group-together held a market share of over 12.8% in 2024. Leading firms continue to invest in research and development to introduce next-generation products focusing on lightweight materials, enhanced recyclability, and innovative sealing mechanisms. Features such as smart closures equipped with QR codes and NFC chips are gaining momentum as companies look to boost consumer engagement, traceability, and product safety. Additionally, the rising importance of health-conscious and traceable packaging is prompting manufacturers to develop closures with features like BPA-NI linings and high-barrier technologies. The growing popularity of online retail, direct-to-consumer brands, and craft production across industries is also amplifying the need for customizable, short-run closures that combine functionality with aesthetic appeal.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising demand for packaged food & beverages

- 3.3.1.2 Booming pharmaceutical industry

- 3.3.1.3 Increasing alcoholic beverage consumption

- 3.3.1.4 Long shelf life and hermetic sealing

- 3.3.1.5 Sustainability & recyclability appeal

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Volatility in raw material prices

- 3.3.2.2 Substitution by lightweight flexible packaging

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Million and Billion Units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Steel

- 5.4 Tin

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million and Billion Units)

- 6.1 Key trends

- 6.2 Crown

- 6.3 Can-ends

- 6.4 Screw

- 6.5 Twist

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million and Billion Units)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Pharmaceuticals

- 7.4 Consumer goods

- 7.5 Personal care & cosmetics

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million and Billion Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Distributors / wholesalers

- 8.4 Retailer

- 8.5 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million and Billion Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Amcor

- 10.2 AptarGroup

- 10.3 Berry Global

- 10.4 CL Smith

- 10.5 Closure Systems International

- 10.6 Crown Holdings

- 10.7 Finn-Korkki

- 10.8 Guala Closures

- 10.9 MJS Packaging

- 10.10 Metal Closures

- 10.11 Nippon Closures

- 10.12 O. Berk

- 10.13 Pelliconi

- 10.14 Silgan Holdings

- 10.15 Sonoco Products

- 10.16 Tecnocap