敗血症治療薬市場の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Sepsis Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 131 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750480

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

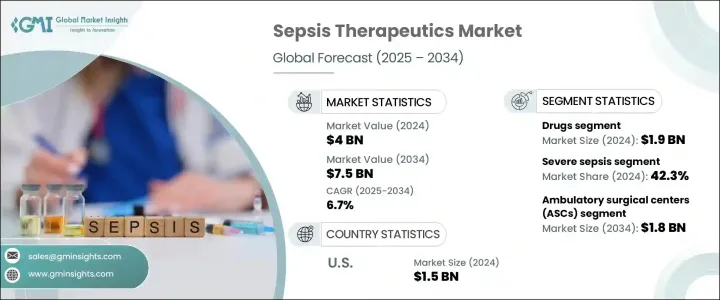

世界の敗血症治療薬市場は、2024年には40億米ドルと評価され、CAGR 6.7%で成長し、2034年には75億米ドルに達すると推定されています。

この市場は、感染に対する制御不能な免疫反応によって引き起こされる生命を脅かす状態によって牽引され、即座に的を絞った医療措置が必要となります。身体の防御システムが制御不能に陥ると、健康な組織に損傷を与え、深刻な臓器不全につながる可能性があります。院内感染による世界の負担の増大と高齢化により、次世代の治療薬が急務となっています。

世界中のヘルスケアシステムは、タイムリーで的確な敗血症治療を提供する必要性によってますます緊張しており、次世代治療オプションの必要性が高まっています。敗血症の発症率が上昇を続ける中、製薬会社やバイオテクノロジー企業は画期的な治療法を発見するために研究開発への投資を強化しています。この技術革新の急増は、身体の免疫反応を調節して患者の生存率を向上させることを目的とした生物学的製剤や免疫療法のパイプラインの増加に特に顕著に表れています。抗菌薬耐性により従来の抗生物質が限界に直面する中、新規薬剤クラス別や精密ベースの治療に対する需要はかつてないほど高まっています。臨床的理解の進展は、規制面での支援環境と相まって、敗血症治療戦略の進化をさらに加速させています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 40億米ドル |

| 予測金額 | 75億米ドル |

| CAGR | 6.7% |

2024年、薬剤セグメントは19億米ドルを生み出しました。抗生物質、抗ウイルス薬、抗真菌薬、血管収縮薬、免疫調節薬は、敗血症管理の基礎であり続けています。治療初期に病原体と闘うためには、広域抗生物質の迅速な投与が不可欠です。副腎皮質ステロイドや血管圧迫薬などの支持療法は、患者を安定させ、全身の炎症を抑えます。薬剤耐性により敗血症の症例が複雑化する中、医薬品開発者はより大きな臨床転帰をもたらす標的療法に注力しています。

2024年には、重症敗血症セグメントのシェアは42.3%に達します。この重症敗血症は、多くの症例が急速に進行し、広範な炎症と臓器不全を特徴とします。特に薬剤耐性感染の脅威が高まる中、このような臨床症状がますます複雑化していることから、より強力なマルチターゲット治療ソリューションの必要性が浮き彫りになっています。ヘルスケアプロバイダーは、早期診断と個別化医療を重視し、感染の拡大防止と患者の予後改善に努めています。

米国敗血症治療薬2024年の市場規模は15億米ドル。この堅調な業績には、高齢者人口の増加、院内感染率の高さ、医療提供の継続的改善など、いくつかの要因が寄与しています。AIと機械学習を敗血症診断に統合することで、リスクのある患者をより迅速かつ正確に特定できるようになり、支持を集めています。さらに、積極的な研究開発プログラムと製品パイプラインの拡大に重点を置くことで、この分野における日本のリーダーシップが強化されています。このような開発により、精密な技術を駆使した治療が敗血症管理の中心的役割を果たす未来が形作られつつあります。

敗血症治療薬の世界市場において、各社はイノベーション、臨床提携、パイプラインの拡充に重点を置いた戦略を採用し、その地位を確固たるものにしています。北米と欧州の企業は、先進的な生物製剤、次世代抗生物質、免疫療法を開発するための研究提携を重視しています。ファイザー、F.ホフマン・ラ・ロシュ、シプラなどの企業は、敗血症の検出と介入を迅速化するために、新規ドラッグデリバリーシステムとAI統合診断プラットフォームに投資しています。多くの企業が、特にアジア太平洋市場において、新たな需要を開拓するため、第II相および第III相臨床試験を進めています。敗血症治療の格差が依然として大きいラテンアメリカや中東・アフリカのような市場では、ライセンシング契約、合併、地域的な製造能力も支持を集めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 敗血症の発生率の増加

- 院内感染症(HAI)の蔓延

- 診断と治療の選択肢における技術の進歩

- 業界の潜在的リスク&課題

- 治療費が高め

- 厳格な規制承認

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:治療の種類別、2021-2034

- 主要動向

- 薬物

- 抗生物質

- 抗ウイルス/抗真菌

- その他の薬物

- 点滴液

- 酸素療法

- 手術

- その他の治療の種類

第6章 市場推計・予測:病気の種類別、2021-2034

- 主要動向

- 軽度の敗血症

- 重度の敗血症

- 敗血症性ショック

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- クリニック

- 外来手術センター

- その他の用途

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- Adrenomed

- Astellas Pharma

- Aurobindo Pharmaceuticals

- Aurora St. Luke’s Medical Center

- Azurity Pharmaceuticals

- Bosch Pharmaceuticals

- Christiana hospitals

- Cipla

- Drive DeVilbiss Healthcare

- F. Hoffmann La Roche

- Medical Services Company

- Pfizer

- Torrent Pharmaceuticals

- West Virginia University Hospital

目次

The Global Sepsis Therapeutics Market was valued at USD 4 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 7.5 billion by 2034, driven by a life-threatening condition triggered by an unregulated immune reaction to infection, which requires immediate and targeted medical attention. When the body's defense system spirals out of control, it can damage healthy tissues and lead to severe organ failure. With the rising global burden of hospital-acquired infections and an aging population, there is an urgent need for next-generation therapies.

Healthcare systems worldwide are increasingly strained by the need to deliver timely and precise sepsis care, intensifying the push for next-generation treatment options. As the incidence of sepsis continues to rise, pharmaceutical and biotech companies are stepping up investments in research and development to discover breakthrough therapies. This surge in innovation is especially apparent in the growing pipeline of biologics and immunotherapies that aim to modulate the body's immune response and improve patient survival rates. With traditional antibiotics facing limitations due to antimicrobial resistance, the demand for novel drug classes and precision-based therapies has never been higher. Advancements in clinical understanding, combined with supportive regulatory environments, are further accelerating the evolution of sepsis treatment strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 6.7% |

In 2024, the drug segment generated USD 1.9 billion. Antibiotics, antivirals, antifungals, vasoconstrictors, and immunomodulators continue to be the foundation of sepsis management. Prompt administration of broad-spectrum antibiotics is essential to combat pathogens early in treatment. Supportive therapies, including corticosteroids and vasopressors, stabilize patients and reduce systemic inflammation. With sepsis cases becoming more complex due to drug resistance, pharmaceutical developers are focusing on more targeted therapies that can offer greater clinical outcomes.

In 2024, the severe sepsis segment held a 42.3% share. Many cases progress rapidly to this critical stage, characterized by extensive inflammation and organ failure. The increasing complexity of these clinical presentations, especially amid the growing threat of drug-resistant infections, underscores the need for more potent, multi-targeted therapeutic solutions. Healthcare providers emphasize early-stage diagnostics and personalized medicine to prevent escalation and improve patient outcomes.

United States Sepsis Therapeutics Market generated USD 1.5 billion in 2024. Several factors contribute to this robust performance, including a rising elderly population, a high rate of hospital-acquired infections, and continuous improvements in healthcare delivery. Integrating AI and machine learning in sepsis diagnostics is gaining traction, allowing for faster, more accurate identification of at-risk patients. Additionally, active R&D programs and a strong focus on expanding product pipelines reinforce the country's leadership in the field. These developments are shaping a future where precision-driven, technology-enabled care plays a central role in sepsis management.

In the Global Sepsis Therapeutics Market companies are adopting strategies focused on innovation, clinical partnerships, and pipeline expansion to solidify their position. Players in North America and Europe emphasize research alliances to develop advanced biologics, next-gen antibiotics, and immunotherapies. Firms such as Pfizer, F. Hoffmann-La Roche, and Cipla are investing in novel drug delivery systems and AI-integrated diagnostic platforms to speed up sepsis detection and intervention. Many companies are progressing through Phase II and III clinical trials, especially in the Asia Pacific market, to tap into emerging demand. Licensing agreements, mergers, and regional manufacturing capabilities are also gaining traction in markets like Latin America and the Middle East & Africa, where the sepsis treatment gap remains wide.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidences of sepsis

- 3.2.1.2 Growing prevalence of hospital-acquired infections (HAIs)

- 3.2.1.3 Technological advancement in diagnostics and treatment options

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Stringent regulatory approvals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Drugs

- 5.2.1 Antibiotics

- 5.2.2 Anti-viral/ Anti-fungal

- 5.2.3 Other drugs

- 5.3 I.V fluids

- 5.4 Oxygen therapy

- 5.5 Surgery

- 5.6 Other treatment types

Chapter 6 Market Estimates and Forecast, By Disease Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Mild sepsis

- 6.3 Severe sepsis

- 6.4 Septic shock

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Clinics

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Adrenomed

- 9.3 Astellas Pharma

- 9.4 Aurobindo Pharmaceuticals

- 9.5 Aurora St. Luke’s Medical Center

- 9.6 Azurity Pharmaceuticals

- 9.7 Bosch Pharmaceuticals

- 9.8 Christiana hospitals

- 9.9 Cipla

- 9.10 Drive DeVilbiss Healthcare

- 9.11 F. Hoffmann La Roche

- 9.12 Medical Services Company

- 9.13 Pfizer

- 9.14 Torrent Pharmaceuticals

- 9.15 West Virginia University Hospital

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 131 Pages

- 納期

- 2~3営業日