電気自動車用サウンドジェネレーター市場の市場機会、成長促進要因、産業動向分析、2025~2034年予測

Electric Vehicle Sound Generator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750474

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

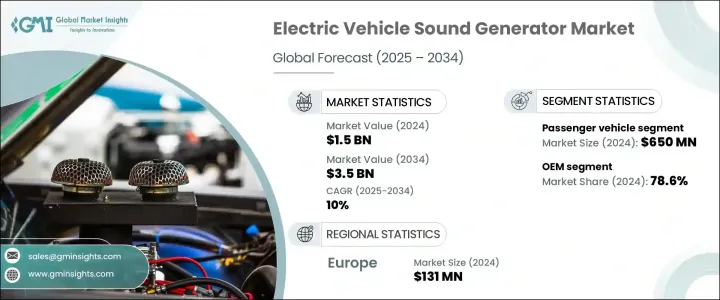

世界の電気自動車用サウンドジェネレーター市場は、2024年に15億米ドルと評価され、CAGR 10%で成長し、2034年には35億米ドルに達すると推定されています。

電気自動車(EV)の普及に伴い、音響発生器の需要は増加の一途をたどっています。EVは低速ではほとんど無音であるため、都市部や歩行者の多い地域では安全上のリスクがあります。世界中の規制機関は、EVに合成音を発生させて歩行者、特に視覚障害者に注意を喚起するよう求めています。このような規制圧力の高まりは、自動車メーカーにEVSGを標準装備として採用するよう促しています。EVの生産台数の増加と安全性への懸念の高まりが、特に人口密度の高い都市での需要を促進しています。

個々の乗用車から商用車や公共交通機関まで、電動モビリティがさまざまなセグメントで拡大を続ける中、電気自動車用サウンドジェネレーター(EVSG)は、オプション機能から必須安全部品へと進化しています。都市がますます混雑し、歩行者天国が増える中、低速でほぼ無音に近いEVの運転は、公共の安全にとって現実的なリスクとなります。サウンドジェネレーターは、歩行者、サイクリスト、その他の道路利用者に車両の接近を警告する音声による合図を生成することで、このギャップを埋めるのに役立ちます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 15億米ドル |

| 予測金額 | 35億米ドル |

| CAGR | 10% |

電気自動車用サウンドジェネレーター市場の乗用車セグメントは40%のシェアを占め、2024年の評価額は6億5,000万米ドルに達しました。ドライバーの移動距離が長くなるにつれて、法規制の遵守と安全性向上の必要性から、自動車メーカーはこれらの車両にサウンドジェネレーターを組み込むようになっています。メーカーはまた、法的義務を満たすためだけでなく、独自のブランドアイデンティティを構築するためにも、カスタムデザインのEVサウンドに注目しています。安全性とブランド・マーケティングの融合が、乗用電気自動車への先進的なEVSGシステムの採用を加速させています。

2024年の市場シェアは、相手先商標製品メーカー(OEM)が78.6%で最大。車両生産時にEVサウンドシステムを搭載することで、パワートレインやインフォテインメント・ユニットを含む車載電子機器やシステムとのシームレスな統合が可能になります。このアプローチにより、当初から法的コンプライアンスが確保されるため、保証の維持や認証プロセスの合理化に役立ちます。OEMは、大規模な購入と組み立てによってコストを削減し、製造効率を維持しながら、ビルトインで規制対応のサウンド・ソリューションを消費者に提供することで利益を得ます。規制機関は、車両が路上を走行する前に適合が保証されるため、OEMによる取り付けを支持しています。

ドイツ電気自動車用サウンドジェネレーター2024年の市場規模は1億3,100万米ドル。同国の優位性は、強力な自動車製造基盤と電動化への積極的な取り組みに起因します。ドイツのメーカーはEVSGシステムをいち早く採用し、競合情勢で優位に立つために規制要件と技術革新を活用しています。彼らのアプローチは、EUの音響規制の厳格な遵守と音響ブランディングの重視を融合させたもので、自動車メーカーはブランドのアイデンティティに沿った特徴的なサウンドプロファイルを作成することができます。大規模な生産設備と高度な研究開発能力に支えられた電気自動車の高生産性は、シームレスに統合されたEVSGソリューションへの需要をさらに高めています。

EVSG市場の主要企業には、Hyundai、ECCO、STMicroelectronics、Continental、Harman International、Aptiv、Denso、Forvia Hella、Brigade Electronics、Ansysなどがあります。競争力を維持するため、これらの企業はデジタルサウンドアーキテクチャの進歩、OEMとのパートナーシップの拡大、AIベースのサウンド生成への投資といった重要な戦略を採用しています。多くの企業は、車載統合とユーザーエクスペリエンスの向上を図りながら、さまざまなタイプのEVに対応するスケーラブルなソリューションに注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 原材料サプライヤー

- 部品メーカー

- ソフトウェア開発者と音響エンジニア

- システムインテグレーター

- 最終用途

- 利益率分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーとイノベーションの情勢

- 特許分析

- 価格動向

- 地域

- 製品

- コスト内訳分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 歩行者の安全に関する規制義務

- EVの普及拡大

- サウンドデザインとテクノロジーの進歩

- OEM統合とブランド差別化

- 業界の潜在的リスク&課題

- 高度なシステムの高コスト

- 技術的および標準化の障壁

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 外部サウンドジェネレータ

- 内部サウンドジェネレーター

- カスタマイズ可能なサウンドシステム

第6章 市場推計・予測:推進力別、2021-2034

- 主要動向

- バッテリー電気自動車(BEV)

- ハイブリッド電気自動車(HEV)

- プラグインハイブリッド電気自動車(PHEV)

- 燃料電池電気自動車(FCEV)

第7章 市場推計・予測:車両別、2021-2034

- 主要動向

- 乗用車

- セダン

- SUV

- ハッチバック

- 商用車

- 小型商用車

- MCV

- HCV

- 二輪車と三輪車

- オフロード車両

第8章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第9章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ハードウェア

- スピーカー

- アンプ

- コントローラー

- アクチュエータ

- 配線ハーネス

- ソフトウェア

- サウンドデザインアプリケーション

- 制御システム

- ユーザーインターフェースシステム

第10章 市場推計・予測:速度域別、2021-2034

- 主要動向

- 低速音響発生器(0~30 km/h)

- 全速度域音響発生装置(時速30km以上)

第11章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第12章 企業プロファイル

- Ansys

- Aptiv

- Brigade Electronics

- Continental

- Denso

- ECCO

- ESI Group(Keysights)

- Forvia Hella

- General Motors

- Harman International

- Hyundai

- Mercedes-Benz

- Softeq

- Soundracer

- STMicroelectronics

- Thor

- TVS

- Volkswagen

- Volvo

目次

The Global Electric Vehicle Sound Generator Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 10% to reach USD 3.5 billion by 2034, as electric vehicles (EVs) become more widespread, the demand for sound generators continues to rise. EVs are almost silent at low speeds, which poses safety risks in urban and pedestrian-heavy areas. Regulatory bodies worldwide have responded by requiring EVs to produce synthetic sounds to alert pedestrians, especially those who are visually impaired. This growing regulatory pressure pushes automakers to adopt EVSGs as a standard feature. The convergence of rising EV production and increasing safety concerns fuels this demand, particularly in densely populated cities.

As electric mobility continues to expand across multiple segments-from individual passenger cars to commercial fleets and public transit-electric vehicle sound generators (EVSGs) are evolving from optional features to mandatory safety components. With cities growing more congested and pedestrian zones increasing, the near-silent operation of EVs at low speeds poses a real risk to public safety. Sound generators help bridge this gap by producing audible cues that alert pedestrians, cyclists, and other road users to an approaching vehicle.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $3.5 Billion |

| CAGR | 10% |

The passenger vehicles segment in the electric vehicle sound generator market held a 40% share, reaching a valuation of USD 650 million in 2024, as these vehicles are most often used in urban areas where pedestrian interaction is frequent. As drivers travel longer distances, the need to ensure regulatory compliance and enhance safety prompts automakers to integrate sound generators in these vehicles. Manufacturers are also turning to custom-designed EV sounds not only to meet legal mandates but also to build distinctive brand identities. The fusion of safety and brand marketing is accelerating the adoption of advanced EVSG systems in passenger electric vehicles.

Original equipment manufacturers (OEMs) held the largest market share of 78.6% in 2024. Installing EV sound systems during vehicle production allows for seamless integration with onboard electronics and systems, including powertrains and infotainment units. This approach ensures legal compliance from the outset, which helps preserve warranties and streamline certification processes. OEMs benefit by reducing costs through large-scale purchasing and assembly, offering consumers built-in, regulation-ready sound solutions while maintaining manufacturing efficiency. Regulatory bodies favor OEM installation since it guarantees adherence before the vehicle hits the road.

Germany Electric Vehicle Sound Generator Market generated USD 131 million in 2024. The country's dominance is attributed to its strong automotive manufacturing base and aggressive push toward electrification. German manufacturers are among the earliest adopters of EVSG systems, leveraging regulatory requirements and innovation to stay ahead in the competitive landscape. Their approach blends strict adherence to EU sound regulations with a focus on acoustic branding, allowing automakers to create signature sound profiles that align with brand identity. The high output of electric vehicles, supported by large-scale production facilities and advanced R&D capabilities, further fuels demand for seamlessly integrated EVSG solutions.

Leading players in the EVSG market include Hyundai, ECCO, STMicroelectronics, Continental, Harman International, Aptiv, Denso, Forvia Hella, Brigade Electronics, and Ansys. To stay competitive, these companies are adopting key strategies such as advancing digital sound architecture, expanding partnerships with OEMs, and investing in AI-based sound generation. Many focus on scalable solutions for different EV types while enhancing in-vehicle integration and user experience.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material supplier

- 3.2.2 Component manufacturers

- 3.2.3 Software developers and acoustic engineers

- 3.2.4 System integrators

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Impact of Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook & future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Price trend

- 3.7.1 Region

- 3.7.2 Product

- 3.8 Cost breakdown analysis

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Regulatory mandates for pedestrian safety

- 3.11.1.2 Increasing adoption of EVs

- 3.11.1.3 Advancements in sound design and technology

- 3.11.1.4 OEM integration and brand differentiation

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High cost of advanced systems

- 3.11.2.2 Technical and standardization barriers

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 External sound generators

- 5.3 Internal sound generators

- 5.4 Customizable sound systems

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Battery electric vehicles (BEV)

- 6.3 Hybrid electric vehicles (HEV)

- 6.4 Plug-in hybrid electric vehicles (PHEV)

- 6.5 Fuel cell electric vehicles (FCEV)

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicle

- 7.2.1 Sedan

- 7.2.2 SUV

- 7.2.3 Hatchback

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

- 7.4 Two and three wheelers

- 7.5 Off-highway vehicles

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Hardware

- 9.2.1 Speakers

- 9.2.2 Amplifiers

- 9.2.3 Controllers

- 9.2.4 Actuators

- 9.2.5 Wiring harnesses

- 9.3 Software

- 9.3.1 Sound design applications

- 9.3.2 Control systems

- 9.3.3 User interface systems

Chapter 10 Market Estimates & Forecast, By Speed Range, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Low-speed sound generators (0-30 km/h)

- 10.3 Full-speed range sound generators (more than 30 km/h)

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Ansys

- 12.2 Aptiv

- 12.3 Brigade Electronics

- 12.4 Continental

- 12.5 Denso

- 12.6 ECCO

- 12.7 ESI Group (Keysights)

- 12.8 Forvia Hella

- 12.9 General Motors

- 12.10 Harman International

- 12.11 Hyundai

- 12.12 Mercedes-Benz

- 12.13 Softeq

- 12.14 Soundracer

- 12.15 STMicroelectronics

- 12.16 Thor

- 12.17 TVS

- 12.18 Volkswagen

- 12.19 Volvo

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日