|

市場調査レポート

商品コード

1750469

複合缶の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Composite Cans Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 複合缶の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月08日

発行: Global Market Insights Inc.

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

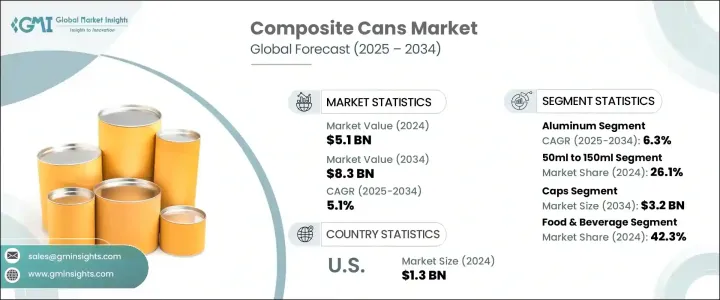

世界の複合缶市場は、2024年には51億米ドルと評価され、スナック食品、調理済み食品、栄養補助食品分野の急速な拡大に後押しされ、CAGR 5.1%で成長し、2034年には83億米ドルに達すると予測されています。

都市化の進展、可処分所得の増加、消費者のライフスタイルの変化が、耐久性、利便性、賞味期限の延長を兼ね備えた包装に対する需要の主な促進要因となっています。多層構造の複合缶は、優れた湿気と酸素のバリアを提供し、デリケートな製品の鮮度と品質を保つのに理想的です。

輸入アルミニウムや鉄鋼に適用された関税のような貿易関連政策は、米国の複合缶メーカーにとって価格設定や調達の状況を破壊してきました。このようなシフトは、コスト上昇や材料調達の課題をもたらし、生産者にサプライチェーンの見直しを促しています。これを受けて、多くの企業は収益性を維持し、将来のリスクを軽減するために、国内原材料と現地生産戦略にシフトしています。こうした再調達の動きは、貿易の混乱を乗り切るだけでなく、より広範な持続可能性と回復力の目標にも合致しています。生産拠点に近い場所で原材料を調達することで、企業はリードタイムを短縮し、ロジスティクスコストを削減し、品質管理と現地規制への準拠を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 51億米ドル |

| 予測金額 | 83億米ドル |

| CAGR | 5.1% |

素材の中では、アルミニウムベースの複合缶が、軽量、耐食性、リサイクル性などの有利な特性によって、2034年までCAGR 6.3%の成長が見込まれています。これらの特性は、飲食品分野で持続可能なパッケージングに対する嗜好が高まっていることとよく一致しています。アルミニウムの湿気、空気、光から保護する能力は、保存期間の延長を必要とする製品にとって理想的な選択肢となります。さらに、環境に優しい慣行と循環型経済に対する政府の支援はこのセグメントを強化し、メーカーが従来のプラスチックからより持続可能な金属ベースのパッケージング・ソリューションに切り替えることを促しています。

容量に基づくと、50ml~150mlセグメントの複合缶は2024年に26.1%のシェアを占めました。このサイズは、健康サプリメント、化粧品、トライアルサイズなど、コンパクトなパッケージングニーズで支持を集めています。都市人口の増加、外出の多いライフスタイル、プレミアムな1回分製品への消費者の関心が、引き続きこのセグメントの成長を支えています。これらの缶は携帯性と利便性を提供し、旅行に適した商品や衝動買いに理想的です。ブランドは革新的なパッケージデザインで視覚的な魅力を高め、パーソナライゼーションと美的アピールを求める消費者の需要を取り込んでいます。

米国複合缶2024年の市場規模は13億米ドル。持続可能でリサイクル可能なプラスチックの代替品を求める動きは、同国の消費者とメーカーの行動に大きな影響を与えています。飲料、スナック、サプリメントにおける環境に優しいパッケージへの需要の高まりが、特に環境意識の高い消費者の間で米国市場のダイナミクスを形成しています。企業は、堆肥化可能な成分、容易なリサイクル性、二酸化炭素排出量の削減を強調した製品ラインで対応しています。

世界の複合缶業界の主要企業は、Smurfit Kappa Group、Irwin Packaging、Sonoco Products、Corex Group、Mondi Groupなどです。市場でのポジショニングを高めるため、主要企業は持続可能な材料統合と高度な製造技術による製品イノベーションに注力しています。飲食品ブランドとの戦略的パートナーシップ、環境に優しい設計への投資、需要の高い地域での生産能力拡大は、メーカーが競争力を維持しながら進化する顧客ニーズを満たすのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 包装食品およびスナック産業の拡大

- 小売およびeコマースチャネルの拡大

- 棚の魅力とブランド化の機会の向上

- ペットフード包装の需要増加

- 栄養補助食品および健康補助食品市場の成長

- 業界の潜在的リスク&課題

- 生産コストが高め

- 再利用性が限られており、使い捨てである

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:材料別、2021-2034

- 主要動向

- アルミニウム

- 板紙

- プラスチック

- 鋼鉄

第6章 市場推計・予測:閉鎖タイプ別、2021-2034

- 主要動向

- キャップ

- スナップオン

- プラグ

- 蓋

- アルミニウム膜

- プラスチック膜

- 板紙の端

第7章 市場推計・予測:容量別、2021-2034

- 主要動向

- 50ml未満

- 50mlから150ml

- 150ml~250ml

- 250mlから500ml

- 500mlから1000ml

- 1000ml以上

第8章 市場推計・予測:業種別、2021-2034

- 主要動向

- 食品と飲料

- 医薬品

- パーソナルケア

- 工業および化学製品

- その他

第9章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Ace Paper Tube

- Bharath Paper Conversions

- Canfab Packaging

- Corex Group

- Heartland Products Group

- Irwin Packaging

- Hangzhou Qunle Packaging

- Mondi Group

- PTS Manufacturing

- Quality Container Company

- Shetron Group

- Smurfit Kappa Group

- Sonoco Products Company

The Global Composite Cans Market was valued at USD 5.1 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 8.3 billion by 2034, fueled by the rapid expansion of the snack food, ready-to-eat meals, and nutraceutical sectors. Rising urbanization, growing disposable incomes, and a shift in consumer lifestyles are key drivers of demand for packaging that combines durability, convenience, and extended shelf life. Composite cans, with their multi-layer construction, offer excellent moisture and oxygen barriers, making them ideal for preserving the freshness and quality of sensitive products.

Trade-related policies, such as the tariffs applied to imported aluminum and steel, have disrupted the pricing and sourcing landscape for composite can manufacturers in the U.S. These shifts have resulted in cost increases and material sourcing challenges, prompting producers to reevaluate their supply chains. In response, many companies are shifting towards domestic raw materials and localized production strategies to maintain profitability and mitigate future risks. This movement toward reshoring is not only helping manufacturers navigate trade disruptions aligns with broader sustainability and resilience goals. By sourcing materials closer to production hubs, firms are reducing lead times, lowering logistics costs, and enhancing their control over quality and compliance with local regulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $8.3 Billion |

| CAGR | 5.1% |

Among materials, aluminum-based composite cans are expected to grow at a CAGR of 6.3% through 2034, driven by favorable properties such as light weight, corrosion resistance, and recyclability. These characteristics align well with the rising preference for sustainable packaging in food and beverage segments. Aluminum's ability to protect against moisture, air, and light makes it an ideal choice for products requiring extended shelf life. Additionally, government support for environmentally friendly practices and circular economies strengthens this segment, encouraging manufacturers to switch from conventional plastics to more sustainable metal-based packaging solutions.

Based on capacity, composite cans in the 50ml to 150ml segment held a 26.1% share in 2024. This size is gaining traction in compact packaging needs across health supplements, cosmetic products, and trial-size offerings. Growing urban populations, on-the-go lifestyles, and consumer interest in premium, single-serve products continue to support segment growth. These cans offer portability and convenience, making them ideal for travel-friendly goods and impulse buys. Brands enhance their visual appeal with innovative packaging designs, tapping into consumer demand for personalization and aesthetic appeal.

U.S. Composite Cans Market was valued at USD 1.3 billion in 2024. The push for sustainable and recyclable alternatives to plastic has significantly influenced consumer and manufacturer behavior in the country. Growing demand for eco-friendly packaging in beverages, snacks, and supplements shapes U.S. market dynamics, especially among environmentally conscious consumers. Companies are responding with product lines that highlight compostable components, easy recyclability, and reduced carbon footprints.

Key players in the Global Composite Cans Industry include Smurfit Kappa Group, Irwin Packaging, Sonoco Products, Corex Group, and Mondi Group. To enhance market positioning, leading companies focus on product innovation through sustainable material integration and advanced manufacturing technologies. Strategic partnerships with food and beverage brands, investments in eco-friendly design, and capacity expansions in high-demand regions are helping manufacturers meet evolving customer needs while staying competitive.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-Side Impact (raw Materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-Side Impact (raw Materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Expansion of the packaged food and snack industry

- 3.3.1.2 Expansion of retail and e-commerce channels

- 3.3.1.3 Improved shelf appeal and branding opportunities

- 3.3.1.4 Increasing demand in pet food packaging

- 3.3.1.5 Growth in the nutraceuticals and health supplements market

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost of production

- 3.3.2.2 Limited reusability and single-use nature

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 Pestel analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Million & units)

- 5.1 Key trends

- 5.2 Aluminum

- 5.3 Paperboard

- 5.4 Plastic

- 5.5 Steel

Chapter 6 Market Estimates & Forecast, By Closure Type, 2021-2034 (USD Million & units)

- 6.1 Key trends

- 6.2 Caps

- 6.2.1 Snap on

- 6.2.2 Plug

- 6.3 Lids

- 6.3.1 Aluminum membrane

- 6.3.2 Plastic membrane

- 6.3.3 Paperboard ends

Chapter 7 Market Estimates & Forecast, By Capacity, 2021-2034 (USD Million & units)

- 7.1 Key trends

- 7.2 Less than 50ml

- 7.3 50ml to 150ml

- 7.4 150ml to 250ml

- 7.5 250ml to 500ml

- 7.6 500ml to 1000ml

- 7.7 Greater than 1000ml

Chapter 8 Market Estimates & Forecast, By Industry Vertical, 2021-2034 (USD Million & units)

- 8.1 Key trends

- 8.2 Food and beverage

- 8.3 Pharmaceutical

- 8.4 Personal care

- 8.5 Industrial & chemicals

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ace Paper Tube

- 10.2 Bharath Paper Conversions

- 10.3 Canfab Packaging

- 10.4 Corex Group

- 10.5 Heartland Products Group

- 10.6 Irwin Packaging

- 10.7 Hangzhou Qunle Packaging

- 10.8 Mondi Group

- 10.9 PTS Manufacturing

- 10.10 Quality Container Company

- 10.11 Shetron Group

- 10.12 Smurfit Kappa Group

- 10.13 Sonoco Products Company