軍用ロボット犬の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Military Robot Dogs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750452

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

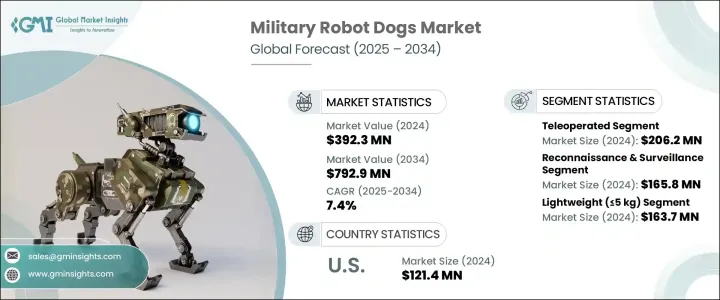

軍用ロボット犬の世界市場規模は、2024年に3億9,230万米ドルとなり、世界の国防予算の増加や兵士の安全性と兵力保護を強化する技術への需要の高まりにより、CAGR 7.4%で成長し、2034年には7億9,290万米ドルに達すると予測されています。

偵察、監視、爆発物処理(EOD)などの重要な任務をこなすロボットとして、軍用ロボット犬の開発は大きな注目を集めています。都市廃墟や化学・生物・放射線・核(CBRN)地帯など、危険な環境でも活動できるロボットは、軍人に大きなメリットをもたらします。

市場はまた、貿易摩擦のような地政学的要因の影響を受けており、海外から調達した特定の部品の生産コストの上昇につながっています。こうした混乱は、メーカーに生産の再調達や調達戦略の調整を検討するよう促しています。防衛請負業者が技術力の強化を迫られる中、軍用ロボット犬開発者は、進化する現代戦の要求に応えるため、自律型ソリューションや任務に特化した設計に注力しています。ネットワーク中心戦争への関心の高まりは、より大規模な軍事システムに統合され、戦場でのリアルタイムの通信と調整を可能にするロボット犬の採用をさらに推進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 3億9,230万米ドル |

| 予測金額 | 7億9,290万米ドル |

| CAGR | 7.4% |

遠隔操作制御システムが軍用ロボット犬市場を独占しており、2024年の市場規模は2億620万米ドルです。これらのシステムは手動制御を提供し、オペレータが爆弾探知、人質救出、その他の危険な任務のようなリスクの高い状況でロボット犬を遠隔管理することを可能にします。この機能により、人的被害の可能性が減少し、重要な任務中の兵士の安全が確保されます。さらに、遠隔操作ロボット犬は、完全自律型のロボット犬と比べて開発が迅速かつ低コストであるため、費用対効果が高く信頼性の高い選択肢を求める防衛軍にとって実用的なソリューションとなります。特に迅速な対応が不可欠な環境では、リアルタイム作戦に迅速に配備され使用できることが、軍事用途に好んで選ばれ続けている主な理由のひとつです。

機能面では、軍用ロボット犬の偵察・監視分野が2024年に1億6,580万米ドルを生み出しました。これらのロボットは、LiDAR、ナイトビジョン、AI搭載光学系などの最先端技術を搭載しており、潜在的な脅威をリアルタイムで検知・分析する能力を高めています。軍用ロボット犬は、敵の動き、簡易爆弾、スナイパーを発見することができ、戦術的な作戦において非常に貴重な存在となります。低ノイズと視覚的シグネチャによるステルス性は、発見されないことが最も重要な隠密作戦に最適です。

ドイツ軍用ロボット犬2024年の市場規模は2,220万米ドル。ドイツの防衛近代化戦略は、NATOの目標や欧州の防衛協力に沿ったものであり、ロボットシステムの採用を大きく後押ししています。軍用ロボット犬は、困難な地形での機動性と汎用性が強化されているため、国境監視、国境を越えた作戦、迅速な対応任務にますます使用されるようになっています。ドイツはPESCOや欧州防衛基金(EDF)などのプログラムの下で技術革新と防衛協力に取り組んでおり、防衛活動におけるロボットソリューションの統合に有利な環境を作り出しています。

世界の軍用ロボット犬業界の主要企業には、Boston Dynamics、Unitree Robotics、Addverb Technologies、Ghost Robotics、Deep Roboticsなどがあります。これらの企業は、ロボット機能の強化、最先端のセンサーの統合、過酷な環境下での信頼性と耐久性の向上に注力しています。さらに、多くのメーカーが、戦力増強、EOD作戦の改善、兵站業務の支援を可能にする自律型任務特化型システムを重視しています。研究開発に投資し、防衛機関と協力することで、AeroArcやXian Supersonic Aviation Technologyのような企業は市場での地位を強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 世界の軍事費の増加

- AIとマシンビジョンの統合

- 兵士の安全と部隊の保護に対する需要の高まり

- 市街戦シナリオの拡大

- 戦術機動性の向上

- 業界の潜在的リスク&課題

- サイバーセキュリティとハッキングのリスク

- バッテリー寿命と耐久性の制限

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:制御モード別、2021 –2034

- 主要動向

- 遠隔操作

- 完全自律型

- 半自律型

第6章 市場推計・予測:積載量別、2021 –2034

- 主要動向

- 軽量(5kg未満)

- 中型(5~10 kg)

- ヘビーデューティー(>10 kg)

第7章 市場推計・予測:用途別、2021 –2034

- 主要動向

- 偵察と監視

- 夜間パトロール

- 前方観測

- 敵地でのステルス監視

- 戦闘支援

- 捜索救助

- 爆発物処理(EOD)

- 地雷探知

- CBRN環境評価

- その他

第8章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- Addverb Technologies

- AeroArc

- Boston Dynamics

- Deep Robotics

- Edith Defense Systems

- Ghost Robotics

- Svaya Robotics

- Unitree Robotics

- Xian Supersonic Aviation Technology

目次

The Global Military Robot Dogs Market was valued at USD 392.3 million in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 792.9 million by 2034, driven by the increasing defense budgets worldwide and the growing demand for technologies that enhance soldier safety and force protection. The development of military robot dogs has gained significant attention, as these robots can perform critical tasks such as reconnaissance, surveillance, and explosive ordnance disposal (EOD) operations. Their ability to operate in hazardous environments, including urban ruins or chemical-biological-radiological-nuclear (CBRN) zones, offers substantial benefits to military personnel.

The market is also influenced by geopolitical factors such as trade tensions, which have led to higher production costs for certain components sourced from overseas. These disruptions have prompted manufacturers to consider reshoring production and adjusting procurement strategies. As defense contractors are under pressure to enhance their technological capabilities, military robot dog developers are focusing on autonomous solutions and mission-specific designs to meet the evolving demands of modern warfare. The growing interest in network-centric warfare has further propelled the adoption of robot dogs that can be integrated into larger military systems, allowing for real-time communication and coordination on the battlefield.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $392.3 Million |

| Forecast Value | $792.9 Million |

| CAGR | 7.4% |

Teleoperated control systems dominate the military robot dogs market, valued at USD 206.2 million in 2024. These systems provide manual control, enabling operators to remotely manage robot dogs in high-risk situations like bomb detection, hostage rescue, and other hazardous missions. This capability reduces the potential for human casualties, ensuring soldiers' safety during critical tasks. Additionally, teleoperated robot dogs are quicker and more affordable to develop compared to their fully autonomous counterparts, making them a practical solution for defense forces looking for cost-effective and reliable options. Their ability to be swiftly deployed and used in real-time operations is one of the main reasons they remain the preferred choice for military applications, particularly in environments where rapid response is essential.

In terms of functionality, the reconnaissance and surveillance segment in military robot dogs generated USD 165.8 million in 2024. These robots are equipped with cutting-edge technologies, including LiDAR, night vision, and AI-powered optics, that enhance their ability to detect and analyze potential threats in real time. Military robot dogs can spot enemy movements, IEDs, or snipers, making them invaluable in tactical operations. Their stealthy nature, due to their low noise and visual signature, makes them perfect for covert operations, where avoiding detection is paramount.

Germany Military Robot Dogs Market generated USD 22.2 million in 2024. Germany's defense modernization strategy, in line with NATO's objectives and European defense collaborations, is significantly driving the adoption of robotic systems. Military robot dogs are increasingly being used for border surveillance, cross-border operations, and rapid-response missions, as they offer enhanced mobility and versatility in challenging terrains. Germany's commitment to technological innovation and defense cooperation under programs like PESCO and the European Defence Fund (EDF) has created a favorable environment for the integration of robotic solutions in its defense operations.

Key players in the Global Military Robot Dogs Industry include Boston Dynamics, Unitree Robotics, Addverb Technologies, Ghost Robotics, and Deep Robotics. These companies are focusing on enhancing robot capabilities, integrating cutting-edge sensors, and improving reliability and durability in harsh environments. Additionally, many manufacturers are emphasizing autonomous mission-specific systems that can provide force multiplication, improve EOD operations, and support logistics tasks. By investing in R&D and collaborating with defense organizations, companies like AeroArc and Xian Supersonic Aviation Technology are strengthening their positions in the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising military expenditures globally

- 3.3.1.2 Integration of AI and machine vision

- 3.3.1.3 Growing demand for soldier safety and force protection

- 3.3.1.4 Growth in urban warfare scenarios

- 3.3.1.5 Enhanced tactical mobility

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Cybersecurity and hacking risks

- 3.3.2.2 Battery life and endurance limitations

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Control Mode, 2021 – 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Teleoperated

- 5.3 Fully autonomous

- 5.4 Semi-autonomous

Chapter 6 Market Estimates and Forecast, By Payload Capacity, 2021 – 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Lightweight (≤5 kg)

- 6.3 Medium weight (5–10 kg)

- 6.4 Heavy duty (>10 kg)

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Reconnaissance and surveillance

- 7.2.1 Night-time patrols

- 7.2.2 Forward observation

- 7.2.3 Stealth surveillance in hostile terrain

- 7.3 Combat Support

- 7.4 Search and rescue

- 7.5 Explosive ordnance disposal (EOD)

- 7.5.1 Mine detection

- 7.5.2 CBRN environment assessment

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Addverb Technologies

- 9.2 AeroArc

- 9.3 Boston Dynamics

- 9.4 Deep Robotics

- 9.5 Edith Defense Systems

- 9.6 Ghost Robotics

- 9.7 Svaya Robotics

- 9.8 Unitree Robotics

- 9.9 Xian Supersonic Aviation Technology

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 180 Pages

- 納期

- 2~3営業日