|

市場調査レポート

商品コード

1750431

ビスケットとクラッカーの市場機会と促進要因、産業動向分析、2025年~2034年予測Biscuits and Crackers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ビスケットとクラッカーの市場機会と促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月13日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

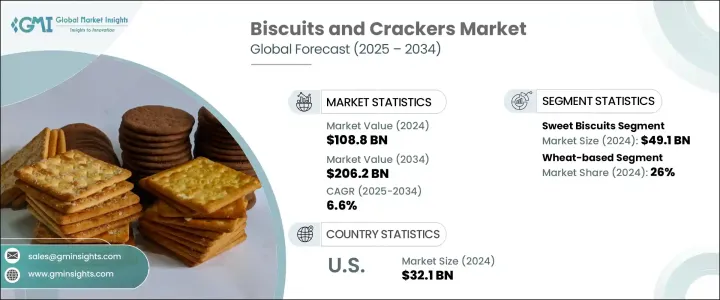

ビスケットとクラッカーの世界市場は、2024年には1,088億米ドルとなり、消費者のペースの速いライフスタイルに合わせた便利で持ち運び可能なスナックオプションへの嗜好の高まりに後押しされ、CAGR 6.6%で成長し、2034年には2,062億米ドルに達すると推定されます。

都市化とパッケージ食品へのアクセスの向上が、特に新興国市場の需要をさらに押し上げます。欧米の食習慣に接する機会が増え、都市部の人口が増加していることが消費動向を加速させています。健康志向の高まりと機能的で体によいスナック菓子へのシフトも、製品開発の形を変えています。

消費者は、低糖質、高タンパク質、グルテンフリー、植物性など、特定の食事ニーズに合致した選択肢を求めており、各ブランドはよりクリーンな表示や栄養豊富な原材料を使ったイノベーションを推進しています。この健康志向の動向は、従来のスナック菓子にスーパーフード、プロバイオティクス、天然甘味料などを取り入れることを促し、スナック菓子の魅力を高めています。さらに、デジタル商取引の急増により、これらの製品は世界中の幅広い消費者層にとってより身近なものとなっています。オンライン・プラットフォームは製品へのリーチを広げるだけでなく、パーソナライズされた推奨や定期購入モデルを提供することで、メーカーが消費者と直接関わり、多様な層のブランド・ロイヤルティを構築することを可能にしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,088億米ドル |

| 予測金額 | 2,062億米ドル |

| CAGR | 6.6% |

製品の多様化が引き続き市場を形成しており、スイート・ビスケット・セグメントは2024年に491億米ドルを創出します。このセグメントは、砂糖摂取に関する意識の高まりにもかかわらず、その幅広い魅力と、風味と食感における絶え間ない革新により、依然として優位を保っています。一方、香ばしいクラッカーは、健康志向の消費者が代替品を求めているため、特にグルテンフリーやタンパク質強化のオプションで注目度が高まっています。これらの品種は、味を犠牲にすることなく栄養を優先する消費者に対応しており、新たな発売の機会を生み出しています。

小麦ベースのビスケットとクラッカーは、2024年に285億米ドルの市場価値を確保し、26%のシェアを占めています。その優位性は、小麦の費用対効果、信頼性の高い世界的供給、シームレスな風味適合を可能にする配合の柔軟性に起因します。メーカーは、小麦のニュートラルな味わいと安定した焼成特性を支持し、甘味と風味のアプリケーションをサポートしています。グルテンフリーやマルチグレイン製品の需要が高まる一方で、小麦は、特に手頃な価格が重要な、価格に敏感な地域では、依然として主食ベースとなっています。

米国ビスケットとクラッカー2024年の市場規模は321億米ドルで、2034年までCAGR 6.9%で成長する見込みです。同国は、可処分所得の高さ、スナッキング文化の定着、小売店の普及を背景に、依然として世界最大かつ最も成熟したスナック市場の1つです。植物由来、アレルゲン不使用、低炭水化物のビスケット・オプションに対する需要も、消費者の健康志向に合致して牽引力を増しています。食料品チェーンにおけるプライベート・ブランドは、手頃な価格を犠牲にすることなくプレミアム・ブランドを補完する高品質の商品を提供し、市場価値にさらに貢献しています。

業界の主要プレーヤーには、グルポ・ビンボ、ネスレS.A.、モンデリーズ・インターナショナル、ブリタニア・インダストリーズ・リミテッド、ケロッグ・カンパニーなどがいます。これらの企業は、ポートフォリオの多様化、より健康的な製品ラインへの投資、地域拡大、デジタル小売業者との提携といった重点戦略を通じて、市場での地位を強化しています。新たなウェルネス動向を取り入れ、地域の嗜好に合わせて製品をカスタマイズすることで、世界の消費者のダイナミックなニーズに応えながら、ブランド・ロイヤルティを高めることを目指しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 市場イントロダクション

- 業界バリューチェーン分析

- 製品概要

- ビスケットとクラッカーの製造工程

- 成分の機能性

- 保存期間技術

- フレーバー開発技術

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国、2021-2024

- 主要輸入国、2021-2024

注:上記の貿易統計は主要国についてのみ提供されます

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 食品安全規制

- ラベル要件

- オーガニック&ナチュラル製品認証

- 栄養強調表示規制

- アレルギー表示要件

- 影響要因

- 促進要因

- 都市部の小売チャネルでは、小分けされた持ち運び用のビスケットパックの需要が高まっています

- グルテンフリー、高繊維、高タンパク質ビスケット製品に対する消費者の関心が高まっています

- 新興経済諸国における組織化された小売およびeコマースプラットフォームの拡大

- 成人消費者をターゲットにした高級で贅沢なビスケットの各種製品イノベーション

- 業界の潜在的リスク&課題

- 原材料価格、特に小麦、砂糖、食用油の価格の変動

- 焼き菓子製品に含まれる糖分とトランス脂肪酸に関する規制圧力

- 促進要因

- 製造プロセス分析

- 生地の準備方法

- 成形および切断技術

- ベーキング技術

- 冷却および包装プロセス

- 原材料分析と調達戦略

- 価格分析

- 持続可能性と環境影響評価

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 市場シェア分析

- 戦略的枠組み

- 合併と買収

- ジョイントベンチャーとコラボレーション

- 新製品開発

- 拡大戦略

- 競合ベンチマーキング

- ベンダー情勢

- 競合ポジショニングマトリックス

- 戦略的ダッシュボード

- ブランドポジショニングと消費者認識分析

- 新規参入者のための市場参入戦略

- プライベートラベル分析と戦略

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 甘いビスケット

- クッキー

- クリーム入りビスケット

- チョコレートコーティングビスケット

- ショートブレッド

- ウエハース

- その他の甘いビスケット

- 風味豊かなビスケットとクラッカー

- プレーンクラッカー

- フレーバークラッカー

- チーズクラッカー

- 塩味クラッカー

- クリスプブレッド

- その他の風味豊かなビスケットとクラッカー

- 消化ビスケット

- プレーンダイジェスティブ

- チョコレートコーティングされたダイジェスティブ

- その他の消化剤

- 健康&ウェルネスビスケット

- 高繊維ビスケット

- 低糖/無糖ビスケット

- 低脂肪ビスケット

- タンパク質強化ビスケット

- 機能性ビスケット

- サンドイッチビスケット

- 朝食用ビスケット

- 職人手作りの特製ビスケット

- その他の製品タイプ

第6章 市場推計・予測:食材別、2021-2034

- 主要動向

- 小麦ベース

- 精製小麦粉

- 全粒小麦粉

- グルテンフリー

- 米粉ベース

- コーンフラワーベース

- アーモンド粉ベース

- その他のグルテンフリー小麦粉

- マルチグレイン

- オート麦ベース

- ライ麦ベース

- オーガニック原料

- 非遺伝子組み換え原料

- その他の成分の種類

第7章 市場推計・予測:包装形態別、2021-2034

- 主要動向

- 硬質包装

- 段ボール箱

- プラスチック容器

- 金属缶

- その他の硬質包装

- フレキシブル包装

- プラスチックポーチ

- フローラップ

- 紙袋

- その他のフレキシブル包装

- トレイとクラムシェル

- マルチパック形式

- シングルサーブ包装

- 持続可能な包装ソリューション

- 生分解性包装

- リサイクル可能な包装

- 堆肥化可能な包装

第8章 市場推計・予測:価格帯別、2021-2034

- 主要動向

- 経済

- ミッドレンジ

- プレミアム

- 超高級&職人技

第9章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- スーパーマーケットとハイパーマーケット

- コンビニエンスストア

- 専門店

- オンライン小売

- フードサービス

- カフェ&レストラン

- ホテル&ケータリング

- 施設内ケータリング

- 自動販売機

- 消費者直販

- その他の流通チャネル

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ地域

第11章 企業プロファイル

- Arnott's Biscuits Limited

- Bahlsen GmbH &Co. KG

- Barilla G. e R. Fratelli S.p.A.

- Britannia Industries Ltd.

- Burton's Biscuit Company

- Campbell Soup Company(Pepperidge Farm)

- Dare Foods Limited

- Fox's Biscuits(2 Sisters Food Group)

- General Mills、Inc.

- Grupo Bimbo

- ITC Limited

- Kellogg Company

- Keebler(Ferrero)

- Kind LLC

- Kashi Company(Kellogg)

- Lotus Bakeries

- Lotte Confectionery Co.、Ltd.

- Mary's Gone Crackers

- Meiji Holdings Co.、Ltd.

- Mondelez International、Inc.

- Nairn's Oatcakes Limited

- Nestle S.A.

- Orion Corporation

- Parle Products Pvt. Ltd.

- PepsiCo、Inc.(Frito-Lay)

- Ryvita Company Limited(ABF)

- Snyder's-Lance、Inc.(Campbell Soup Company)

- United Biscuits(pladis)

- Walkers Shortbread Ltd.

- Yildiz Holding(Ulker)

The Global Biscuits and Crackers Market was valued at USD 108.8 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 206.2 billion by 2034, fueled by consumers' rising preference for convenient and portable snack options that align with fast-paced lifestyles. Urbanization and evolving access to packaged food further push market demand, especially in developing regions. Increased exposure to Western eating habits and a rising urban population are accelerating consumption trends. A growing emphasis on health and wellness, paired with a shift toward functional and better-for-you snacks, is also reshaping product development.

Consumers seek options that align with specific dietary needs, such as low-sugar, high-protein, gluten-free, and plant-based formulations, pushing brands to innovate with cleaner labels and nutrient-rich ingredients. This health-conscious trend is also encouraging the incorporation of superfoods, probiotics, and natural sweeteners into traditional snack profiles to enhance their appeal. Additionally, the surge in digital commerce is making these products more accessible to a broader consumer base globally. Online platforms are not only expanding product reach but also offering personalized recommendations and subscription models, allowing manufacturers to engage directly with consumers and build brand loyalty across diverse demographics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $108.8 Billion |

| Forecast Value | $206.2 Billion |

| CAGR | 6.6% |

Product diversification continues to shape the market, with the sweet biscuits segment generating USD 49.1 billion in 2024. This segment remains dominant due to its widespread appeal and continuous innovation in flavor and texture, despite growing awareness around sugar intake. Meanwhile, savory crackers are witnessing increased attention, particularly gluten-free and protein-enriched options, as health-conscious consumers seek alternatives. These varieties cater to those prioritizing nutrition without sacrificing taste, creating opportunities for new launches.

Wheat-based biscuits and crackers secured USD 28.5 billion market value in 2024, holding a 26% share. Their dominance stems from wheat's cost-effectiveness, reliable global supply, and flexibility in formulation, which allows for seamless flavor adaptation. Manufacturers favor wheat for its neutral taste and consistent baking properties, which support sweet and savory applications. While demand for gluten-free and multi-grain offerings rises, wheat remains the staple base, especially in price-sensitive regions where affordability is critical.

U.S. Biscuits and Crackers Market generated USD 32.1 billion in 2024 and is set to grow at a 6.9% CAGR through 2034. The country remains one of the largest and most mature snack markets in the world, driven by high disposable income, an ingrained snacking culture, and widespread retail availability. Demand for plant-based, allergen-free, and low-carb biscuit options is also gaining traction, aligning with consumer focus on wellness. Private labels in grocery chains have further contributed to market value, providing quality offerings that complement premium brands without sacrificing affordability.

Key players in the industry include Grupo Bimbo, Nestle S.A., Mondelez International Inc., Britannia Industries Limited, and Kellogg Company. These companies are strengthening their market position through focused strategies such as portfolio diversification, investment in healthier product lines, regional expansion, and partnerships with digital retailers. By tapping into emerging wellness trends and customizing offerings for local tastes, they aim to boost brand loyalty while meeting the dynamic needs of global consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research methodology

- 1.3 Research scope & assumptions

- 1.4 List of data sources

- 1.5 Market estimation technique

- 1.6 Market segmentation & breakdown

- 1.7 Research limitations

Chapter 2 Executive Summary

- 2.1 Segment highlights

- 2.2 Competitive landscape snapshot

- 2.3 Regional market outlook

- 2.4 Key market trends

- 2.5 Future market outlook

Chapter 3 Industry Insights

- 3.1 Market introduction

- 3.2 Industry value chain analysis

- 3.3 Product overview

- 3.3.1 Biscuit & cracker manufacturing process

- 3.3.2 Ingredient functionality

- 3.3.3 Shelf-life technologies

- 3.3.4 Flavor development techniques

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Demand-side impact (selling price)

- 3.4.3.1 Price transmission to end markets

- 3.4.3.2 Market share dynamics

- 3.4.3.3 Consumer response patterns

- 3.4.4 Key companies impacted

- 3.4.5 Strategic industry responses

- 3.4.5.1 Supply chain reconfiguration

- 3.4.5.2 Pricing and product strategies

- 3.4.5.3 Policy engagement

- 3.4.6 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Trade statistics (HS code)

- 3.5.1 Major exporting countries, 2021-2024 (kilo tons)

- 3.5.2 Major importing countries, 2021-2024 (kilo tons)

Note: the above trade statistics will be provided for key countries only.

- 3.6 Supplier landscape

- 3.7 Profit margin analysis

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.9.1 Food safety regulations

- 3.9.2 Labeling requirements

- 3.9.3 Organic & natural product certifications

- 3.9.4 Nutritional claim regulations

- 3.9.5 Allergen labeling requirements

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising demand for portion-controlled and on-the-go biscuit packs in urban retail channels.

- 3.10.1.2 Increased consumer interest in gluten-free, high-fiber, and protein-enriched biscuit formulations.

- 3.10.1.3 Expansion of organized retail and e-commerce platforms in developing economies.

- 3.10.1.4 Product innovation in premium and indulgent biscuit varieties targeting adult consumers.

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Volatility in raw material prices, especially wheat, sugar, and edible oils.

- 3.10.2.2 Regulatory pressures around sugar content and trans fats in baked snack products.

- 3.10.1 Growth drivers

- 3.11 Manufacturing process analysis

- 3.11.1 Dough preparation methods

- 3.11.2 Forming & cutting techniques

- 3.11.3 Baking technologies

- 3.11.4 Cooling & packaging processes

- 3.12 Raw material analysis & procurement strategies

- 3.13 Pricing analysis

- 3.14 Sustainability & environmental impact assessment

- 3.15 Growth potential analysis

- 3.16 Porter's analysis

- 3.17 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Market Share Analysis

- 4.6 Strategic Framework

- 4.6.1 Mergers & Acquisitions

- 4.6.2 Joint Ventures & Collaborations

- 4.6.3 New Product Developments

- 4.6.4 Expansion Strategies

- 4.7 Competitive Benchmarking

- 4.8 Vendor Landscape

- 4.9 Competitive Positioning Matrix

- 4.10 Strategic Dashboard

- 4.11 Brand Positioning & Consumer Perception Analysis

- 4.12 Market Entry Strategies for New Players

- 4.13 Private Label Analysis & Strategies

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Sweet biscuits

- 5.2.1 Cookies

- 5.2.2 Cream-filled biscuits

- 5.2.3 Chocolate-coated biscuits

- 5.2.4 Shortbread

- 5.2.5 Wafers

- 5.2.6 Other sweet biscuits

- 5.3 Savory biscuits & crackers

- 5.3.1 Plain crackers

- 5.3.2 Flavored crackers

- 5.3.3 Cheese crackers

- 5.3.4 Saltines

- 5.3.5 Crispbreads

- 5.3.6 Other savory biscuits & crackers

- 5.4 Digestive biscuits

- 5.4.1 Plain digestives

- 5.4.2 Chocolate-coated digestives

- 5.4.3 Other digestives

- 5.5 Health & wellness biscuits

- 5.5.1 High-fiber biscuits

- 5.5.2 Low-sugar/sugar-free biscuits

- 5.5.3 Low-fat biscuits

- 5.5.4 Protein-enriched biscuits

- 5.5.5 Functional biscuits

- 5.6 Sandwich biscuits

- 5.7 Breakfast biscuits

- 5.8 Artisanal & specialty biscuits

- 5.9 Other product types

Chapter 6 Market Estimates & Forecast, By Ingredient Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Wheat-based

- 6.2.1 Refined wheat flour

- 6.2.2 Whole wheat flour

- 6.3 Gluten-free

- 6.3.1 Rice flour-based

- 6.3.2 Corn flour-based

- 6.3.3 Almond flour-based

- 6.3.4 Other gluten-free flours

- 6.4 Multi-grain

- 6.5 Oat-based

- 6.6 Rye-based

- 6.7 Organic ingredients

- 6.8 Non-GMO ingredients

- 6.9 Other ingredient types

Chapter 7 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Rigid packaging

- 7.2.1 Paperboard boxes

- 7.2.2 Plastic containers

- 7.2.3 Metal tins

- 7.2.4 Other rigid packaging

- 7.3 Flexible packaging

- 7.3.1 Plastic pouches

- 7.3.2 Flow wraps

- 7.3.3 Paper bags

- 7.3.4 Other flexible packaging

- 7.4 Trays & clamshells

- 7.5 Multi-pack formats

- 7.6 Single-serve packaging

- 7.7 Sustainable packaging solutions

- 7.7.1 Biodegradable packaging

- 7.7.2 Recyclable packaging

- 7.7.3 Compostable packaging

Chapter 8 Market Estimates & Forecast, By Price Segment, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Economy

- 8.3 Mid-range

- 8.4 Premium

- 8.5 Super-premium & artisanal

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Supermarkets & hypermarkets

- 9.3 Convenience stores

- 9.4 Specialty stores

- 9.5 Online retail

- 9.6 Foodservice

- 9.6.1 Cafes & restaurants

- 9.6.2 Hotels & catering

- 9.6.3 Institutional catering

- 9.7 Vending machines

- 9.8 Direct-to-consumer

- 9.9 Other distribution channels

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Arnott's Biscuits Limited

- 11.2 Bahlsen GmbH & Co. KG

- 11.3 Barilla G. e R. Fratelli S.p.A.

- 11.4 Britannia Industries Ltd.

- 11.5 Burton's Biscuit Company

- 11.6 Campbell Soup Company (Pepperidge Farm)

- 11.7 Dare Foods Limited

- 11.8 Fox's Biscuits (2 Sisters Food Group)

- 11.9 General Mills, Inc.

- 11.10 Grupo Bimbo

- 11.11 ITC Limited

- 11.12 Kellogg Company

- 11.13 Keebler (Ferrero)

- 11.14 Kind LLC

- 11.15 Kashi Company (Kellogg)

- 11.16 Lotus Bakeries

- 11.17 Lotte Confectionery Co., Ltd.

- 11.18 Mary's Gone Crackers

- 11.19 Meiji Holdings Co., Ltd.

- 11.20 Mondelez International, Inc.

- 11.21 Nairn's Oatcakes Limited

- 11.22 Nestle S.A.

- 11.23 Orion Corporation

- 11.24 Parle Products Pvt. Ltd.

- 11.25 PepsiCo, Inc. (Frito-Lay)

- 11.26 Ryvita Company Limited (ABF)

- 11.27 Snyder's-Lance, Inc. (Campbell Soup Company)

- 11.28 United Biscuits (pladis)

- 11.29 Walkers Shortbread Ltd.

- 11.30 Yildiz Holding (Ulker)