コーヒーポッドの市場機会と促進要因、業界動向分析、2025年~2034年予測

Coffee Pods Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750421

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

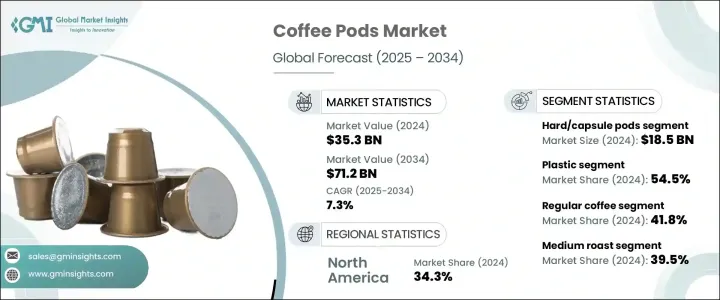

世界のコーヒーポッド市場は、2024年には353億米ドルと評価され、2034年にはCAGR 7.3%で成長して712億米ドルに達すると推定されています。

多忙な日常生活やハイブリッドな職場環境に適応する人が増える中、シングルサーブ形式のコーヒーが台所や職場の定番になりつつあります。密封されたポッドコーヒーの利便性は、後片付けが最小限で済むため、家庭でカフェスタイルのコーヒー体験を求める現代の消費者を魅了し続けています。都市部の家庭では、味の安定性を保ちながら時間を節約できるコンパクトな抽出ソリューションにシフトしています。

もう一つの重要な成長要因は、現在ポッド形式で入手可能な多種多様なフレーバー、オーガニックブレンド、スペシャルティオプションにあり、多様なコーヒー愛飲者グループを惹きつけています。コーヒーメーカーが郊外や半都市部でも利用しやすくなるにつれて、非伝統的市場で需要が高まる。北米と欧州は早くからポッド式コーヒーを採用してきたが、現在ではアジア太平洋とラテンアメリカ地域がプレミアムポッド式コーヒーに強い関心を示しています。持続可能性に対する意識の高まりは、リサイクル可能なポッド素材や生分解性ポッド素材の技術革新に勢いを与え、この競争領域における製品開発とブランド戦略を再構築しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 353億米ドル |

| 予測金額 | 712億米ドル |

| CAGR | 7.3% |

2024年の製品タイプ別世界市場は、ハードタイプまたはカプセルタイプのコーヒーポッドが52.6%のシェアを占め、185億米ドルの売上を計上しました。このカテゴリーは、安定した強さと風味を持つ大胆なエスプレッソ・スタイルのビールを好む消費者にアピールします。家庭でのグルメ体験志向の高まりと、コンパクトなキッチンやオフィススペースに合わせたシングルサーブコーヒーマシーンの台頭が相まって、需要が大きく伸びています。品質を犠牲にすることなく利便性を求める消費者が増えるにつれ、カプセル・ポッド分野は繁栄を続けています。フレーバープロファイル、焙煎度合い、スペシャルティブレンドの革新の急増がこのカテゴリーを拡大し、カジュアルな飲み手からコーヒー通まで幅広い層に魅力的な存在であり続けています。

コーヒーポッド製造における素材の選択は、製品の魅力と持続可能性に大きく影響します。プラスチックベースのポッドセグメントは2024年に54.5%のシェアを占め、2034年までCAGR 7%で成長すると予想されています。その人気は、耐久性、費用対効果、鮮度を閉じ込める能力といった利点に起因します。しかし、環境に対する監視の目はますます厳しくなっており、メーカーは非生分解性包装のエコロジカル・フットプリントへの対応を迫られています。これに対し、企業は消費者の期待と規制上の要求の両方を満たすため、堆肥化可能で完全にリサイクル可能な代替ポッドなど、環境に優しい素材の開発を強化しています。

北米コーヒーポッド 2024年のシェアは34.3%。経済的要因が消費者行動に変化をもたらし、特に価格に敏感な購買層がコスト削減の選択肢として再利用可能なポッドを選ぶようになっています。このような変化にもかかわらず、この地域は全体として堅調な販売量を維持しています。これとは対照的に、欧州市場はより安定しており、根強いコーヒーの伝統と抽出品質に対する洗練された評価が、プレミアムポッドの堅調な販売を牽引しています。一人当たり消費量の増加とエスプレッソベースの飲料の人気が、この地域の成長を支えています。

主要企業は、Nestle SA、Tim Hortons、JAB、Keurig Dr Pepper Inc.、Starbucks Corporationなどです。市場セグメンテーションを強化するため、市場セグメンテーション分野の企業はさまざまな戦略を駆使しています。主なアプローチには、植物由来や持続可能なポッド形式による製品ポートフォリオの拡大、マシンの互換性の強化、地域の味覚に合わせたフレーバーの多様化などがあります。家電メーカーとの戦略的提携は流通網の強化に役立ち、消費者直販チャネルやサブスクリプション・モデルはブランドの粘着性を高めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 製造業者

- 販売代理店

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 便利で高品質な自家醸造に対する消費者の需要の高まり

- 倫理的で高級なコーヒーへの関心の高まり

- 技術的進歩

- 業界の潜在的リスク&課題

- サプライチェーンの混乱

- 経済の不確実性

- 市場機会

- 促進要因

- 製品概要

- コーヒーポッドの製造工程

- コーヒーの加工・包装技術

- 賞味期限保存技術

- フレーバーカプセル化方法

- 規制の枠組みと基準

- 食品安全規制

- 包装およびラベルの要件

- オーガニック&フェアトレード認証

- 使い捨て製品に関する環境規制

- リサイクル基準とコンプライアンス

- 製造プロセス分析

- コーヒーの焙煎と粉砕

- ポッドの組み立てと充填

- シーリングおよび包装技術

- 品質管理プロセス

- 原材料分析と調達戦略

- 価格分析

- 持続可能性と環境影響評価

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 市場シェア分析

- 戦略枠組み

- 合併と買収

- ジョイントベンチャーとコラボレーション

- 新製品開発

- 拡大戦略

- 競合ベンチマーキング

- ベンダー情勢

- 競合ポジショニングマトリックス

- 戦略的ダッシュボード

- ブランドポジショニングと消費者認識分析

- 新規参入者の市場参入戦略

- プライベートラベル分析と戦略

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- ソフトポッド

- 紙フィルターポッド

- メッシュフィルターポッド

- その他のソフトポッド

- ハード/カプセルポッド

- プラスチックカプセル

- アルミニウムカプセル

- 堆肥化可能なカプセル

- その他のハードポッド

第6章 市場推計・予測:材質別、2021-2034

- 主要動向

- プラスチック

- 従来のプラスチック

- リサイクル可能なプラスチック

- バイオプラスチック

- アルミニウム

- 紙と繊維

- 生分解性/堆肥化可能な素材

- その他

第7章 市場推計・予測:コーヒーの種類別、2021-2034

- 主要動向

- レギュラーコーヒー

- アラビカ

- ロブスタ

- ブレンド

- オーガニックコーヒー

- フレーバーコーヒー

- バニラ

- キャラメル

- ヘーゼルナッツ

- チョコレート

- その他のフレーバー

- カフェイン抜きコーヒー

- スペシャルティコーヒー

- シングルオリジン

- マイクロロット

- その他のスペシャルティコーヒー

- フェアトレードコーヒー

- その他のコーヒーの種類

第8章 市場推計・予測:焙煎タイプ別、2021-2034

- 主要動向

- ミディアムロースト

- 中深煎り

- ダークロースト

- エクストラダークロースト

第9章 市場推計・予測:流通チャネル別、2021 –2034

- 主要動向

- スーパーマーケットとハイパーマーケット

- 専門店

- コンビニエンスストア

- オンライン小売

- 企業のウェブサイト

- eコマースプラットフォーム

- サブスクリプションサービス

- フードサービス

- 消費者直販

- その他

第10章 市場推計・予測:機種互換性別、2021-2034

- 主要動向

- ネスプレッソ

- キューリグ

- タッシモ

- センセオ

- ドルチェグスト

- ラバッツァ

- イリー

- マルチ互換ポッド

- その他

第11章 市場推計・予測:価格帯別、2021-2034

- 主要動向

- 経済

- ミッドレンジ

- プレミアム

- スーパープレミアム

第12章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第13章 企業プロファイル

- Nestle S.A.(Nespresso、Nescafe Dolce Gusto)

- Keurig Dr Pepper Inc.

- JAB Holding Company(Jacobs Douwe Egberts)

- Luigi Lavazza S.p.A.

- The J.M. Smucker Company

- Starbucks Corporation

- Kraft Heinz Company

- Dunkin'Brands Group、Inc.

- Illycaffe S.p.A.

- Melitta Group

- Dualit Ltd.

- Gourmesso

- Ethical Coffee Company

- Caffe Vergnano S.p.A.

- Peet's Coffee &Tea、Inc.

- Caribou Coffee Company

- Tchibo GmbH

- UCC Ueshima Coffee Co.、Ltd.

- Strauss Group Ltd.

- Cameron's Coffee

- San Francisco Bay Coffee

- Cafe Bustelo(J.M. Smucker)

- Cafe Royal

- Luckin Coffee Inc.

- Trung Nguyen Group

- Tim Hortons Inc.(Restaurant Brands International)

- Segafredo Zanetti(Massimo Zanetti Beverage Group)

- Reily Foods Company(Community Coffee)

- Rogers Family Company

- Puroast Coffee Company

目次

The Global Coffee Pods Market was valued at USD 35.3 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 71.2 billion by 2034, driven by the increasing appeal of convenience-driven products, especially among busy consumers seeking fast, premium coffee without the effort. With more people adapting to hectic routines and hybrid work environments, single-serve coffee formats are becoming a staple in kitchens and workplaces. The convenience of sealed, pre-portioned pods with minimal cleanup continues to attract modern consumers looking for a cafe-style coffee experience at home. Urban households shift towards compact brewing solutions that save time while maintaining taste consistency.

Another important growth factor lies in the broad variety of flavors, organic blends, and specialty options now available in pod format, attracting a diverse group of coffee drinkers. Demand rises in non-traditional markets as coffee machines become more accessible across suburban and semi-urban areas. While North America and Europe have been early adopters, the Asia Pacific and Latin American regions are now showing robust interest in premium pod-based coffee formats. The growing consciousness around sustainability has added momentum to innovations in recyclable and biodegradable pod materials, reshaping product development and branding strategies in this competitive space.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $35.3 Billion |

| Forecast Value | $71.2 Billion |

| CAGR | 7.3% |

In 2024, hard or capsule coffee pods dominated the global market by product type, accounting for a 52.6% share and generating USD 18.5 billion in sales. This category appeals to consumers who prefer bold, espresso-style brews with consistent strength and flavor. The growing inclination toward gourmet experiences at home, combined with the rise in single-serve coffee machines tailored for compact kitchens and office spaces, has driven demand significantly. As more consumers seek convenience without sacrificing quality, the capsule pod segment continues flourishing. A surge in innovation across flavor profiles, roast intensities, and specialty blends expands this category, keeping it attractive to a broad audience ranging from casual drinkers to coffee connoisseurs.

The choice of material in coffee pod production significantly affects product appeal and sustainability performance. Plastic-based pods segment held a 54.5% share in 2024 and is expected to grow at a CAGR of 7% through 2034. Their popularity stems from benefits such as durability, cost-effectiveness, and the ability to lock in freshness. Yet, increasing environmental scrutiny has pressurized manufacturers to address the ecological footprint of non-biodegradable packaging. In response, companies are stepping up development of eco-friendly materials, including compostable and fully recyclable pod alternatives, to meet both consumer expectations and regulatory demands.

North America Coffee Pods Market held a 34.3% share in 2024. The economic factors influence a shift in consumer behavior, particularly among price-sensitive buyers now opting for reusable pods as a cost-saving alternative. Despite this shift, the region continues to maintain strong overall sales volumes. In contrast, European markets have remained more consistent, with robust sales of premium pods driven by deep-rooted coffee traditions and a refined appreciation for brewing quality. Higher per-capita consumption and the popularity of espresso-based drinks help sustain growth in this region.

Top market players include Nestle SA, Tim Hortons, JAB, Keurig Dr Pepper Inc., and Starbucks Corporation. To enhance their market footprint, companies in the coffee pods segment are leveraging a mix of strategies. Key approaches include expanding product portfolios with plant-based and sustainable pod formats, enhancing machine compatibility, and diversifying flavor offerings to cater to regional palates. Strategic collaborations with appliance manufacturers help strengthen distribution networks, while direct-to-consumer channels and subscription models increase brand stickiness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Methodology and Scope

- 1.2 Research methodology

- 1.3 Research scope & assumptions

- 1.4 List of data sources

- 1.5 Market estimation technique

- 1.6 Research limitations

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Manufacturers

- 3.1.4 Distributors

- 3.1.5 Impact on trade

- 3.1.6 Trade volume disruptions

- 3.2 Retaliatory Measures

- 3.3 Impact on the Industry

- 3.3.1 Supply-Side impact (Raw Materials)

- 3.3.1.1 Price volatility in key materials

- 3.3.1.2 Supply chain restructuring

- 3.3.1.3 Production cost implications

- 3.3.1 Supply-Side impact (Raw Materials)

- 3.4 Demand-Side Impact (Selling Price)

- 3.4.1 Price transmission to end markets

- 3.4.2 Market share dynamics

- 3.4.3 Consumer response patterns

- 3.5 Key companies impacted

- 3.6 Strategic industry responses

- 3.6.1 Supply chain reconfiguration

- 3.6.2 Pricing and product strategies

- 3.6.3 Policy engagement

- 3.7 Outlook and future considerations

- 3.8 Supplier landscape

- 3.9 Profit margin analysis

- 3.10 Key news & initiatives

- 3.11 Regulatory landscape

- 3.12 Impact forces

- 3.12.1 Growth drivers

- 3.12.1.1 Rising consumer demand for convenient and high-quality home brewing

- 3.12.1.2 Growing interest in ethical and premium coffee options

- 3.12.1.3 Technological advancements

- 3.12.2 Industry pitfalls & challenges

- 3.12.2.1 Supply chain disruptions

- 3.12.2.2 Economic uncertainty

- 3.12.3 Market Opportunities

- 3.12.1 Growth drivers

- 3.13 Product Overview

- 3.13.1 Coffee pod manufacturing process

- 3.13.2 Coffee processing & packaging technologies

- 3.13.3 Shelf-life preservation techniques

- 3.13.4 Flavor encapsulation methods

- 3.14 Regulatory framework & standards

- 3.14.1 Food safety regulations

- 3.14.2 Packaging & labeling requirements

- 3.14.3 Organic & fair trade certifications

- 3.14.4 Environmental regulations for single-use products

- 3.14.5 Recyclability standards & compliance

- 3.15 Manufacturing process analysis

- 3.15.1 Coffee roasting & grinding

- 3.15.2 Pod assembly & filling

- 3.15.3 Sealing & packaging technologies

- 3.15.4 Quality control processes

- 3.16 Raw material analysis & procurement strategies

- 3.17 Pricing Analysis

- 3.18 Sustainability & environmental impact assessment

- 3.19 Growth potential analysis

- 3.20 Porter's analysis

- 3.21 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Market share analysis

- 4.3 Strategic framework

- 4.3.1 Mergers & acquisitions

- 4.3.2 Joint ventures & collaborations

- 4.3.3 New product developments

- 4.3.4 Expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Vendor landscape

- 4.6 Competitive positioning matrix

- 4.7 Strategic dashboard

- 4.8 Brand positioning & consumer perception analysis

- 4.9 Market entry strategies for new players

- 4.10 Private label analysis & strategies

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Soft pods

- 5.2.1 Paper filter pods

- 5.2.2 Mesh filter pods

- 5.2.3 Other soft pods

- 5.3 Hard/Capsule pods

- 5.3.1 Plastic capsules

- 5.3.2 Aluminum capsules

- 5.3.3 Compostable capsules

- 5.3.4 Other hard pods

Chapter 6 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Plastic

- 6.2.1 Conventional plastic

- 6.2.2 Recyclable plastic

- 6.2.3 Bioplastic

- 6.3 Aluminum

- 6.4 Paper & fiber

- 6.5 Biodegradable/Compostable materials

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Coffee Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Regular coffee

- 7.2.1 Arabica

- 7.2.2 Robusta

- 7.2.3 Blends

- 7.3 Organic coffee

- 7.4 Flavored coffee

- 7.4.1 Vanilla

- 7.4.2 Caramel

- 7.4.3 Hazelnut

- 7.4.4 Chocolate

- 7.4.5 Other Flavors

- 7.5 Decaffeinated coffee

- 7.6 Specialty coffee

- 7.6.1 Single Origin

- 7.6.2 Micro-Lot

- 7.6.3 Other specialty coffee

- 7.7 Fair trade coffee

- 7.8 Other coffee types

Chapter 8 Market Estimates and Forecast, By Roast Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Medium roast

- 8.3 Medium-dark roast

- 8.4 Dark roast

- 8.5 Extra dark roast

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Supermarkets & Hypermarkets

- 9.3 Specialty stores

- 9.4 Convenience stores

- 9.5 Online retail

- 9.5.1 Company websites

- 9.5.2 E-commerce platforms

- 9.5.3 Subscription services

- 9.6 Foodservice

- 9.7 Direct-to-consumer

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Machine Compatibility, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Nespresso

- 10.3 Keurig

- 10.4 Tassimo

- 10.5 Senseo

- 10.6 Dolce Gusto

- 10.7 Lavazza

- 10.8 Illy

- 10.9 Multi-compatible pods

- 10.10 Others

Chapter 11 Market Estimates and Forecast, By Price Range, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 Economy

- 11.3 Mid-Range

- 11.4 Premium

- 11.5 Super-Premium

Chapter 12 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 Saudi Arabia

- 12.6.2 South Africa

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Nestle S.A. (Nespresso, Nescafe Dolce Gusto)

- 13.2 Keurig Dr Pepper Inc.

- 13.3 JAB Holding Company (Jacobs Douwe Egberts)

- 13.4 Luigi Lavazza S.p.A.

- 13.5 The J.M. Smucker Company

- 13.6 Starbucks Corporation

- 13.7 Kraft Heinz Company

- 13.8 Dunkin' Brands Group, Inc.

- 13.9 Illycaffe S.p.A.

- 13.10 Melitta Group

- 13.11 Dualit Ltd.

- 13.12 Gourmesso

- 13.13 Ethical Coffee Company

- 13.14 Caffe Vergnano S.p.A.

- 13.15 Peet's Coffee & Tea, Inc.

- 13.16 Caribou Coffee Company

- 13.17 Tchibo GmbH

- 13.18 UCC Ueshima Coffee Co., Ltd.

- 13.19 Strauss Group Ltd.

- 13.20 Cameron's Coffee

- 13.21 San Francisco Bay Coffee

- 13.22 Cafe Bustelo (J.M. Smucker)

- 13.23 Cafe Royal

- 13.24 Luckin Coffee Inc.

- 13.25 Trung Nguyen Group

- 13.26 Tim Hortons Inc. (Restaurant Brands International)

- 13.27 Segafredo Zanetti (Massimo Zanetti Beverage Group)

- 13.28 Reily Foods Company (Community Coffee)

- 13.29 Rogers Family Company

- 13.30 Puroast Coffee Company

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日