|

市場調査レポート

商品コード

1750419

胸骨閉鎖システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Sternal Closure Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 胸骨閉鎖システムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月13日

発行: Global Market Insights Inc.

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

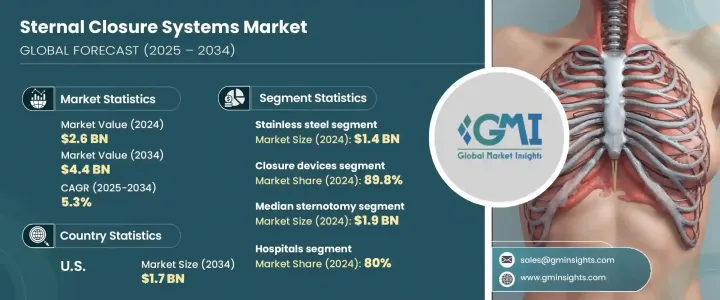

世界の胸骨閉鎖システム市場は、2024年には26億米ドルと評価され、2034年にはCAGR5.3%で成長して44億米ドルに達すると推定されています。

冠動脈疾患などの心血管疾患の有病率の増加により、開心術、特に胸骨正中切開術が一般的になっています。心臓手術の増加に伴い、効果的な胸骨閉鎖装置の需要が急増しています。先進的な胸骨閉鎖システムは、感染リスクを低減し、治癒を改善し、入院期間を最短にすることで、患者の転帰を向上させました。これらのシステムの成功は、術後の合併症の減少につながり、その使用と市場全体の成長を後押ししています。

胸骨閉鎖システムは、心臓手術などの術後に胸骨を安定させ閉鎖するために設計された医療機器です。これらの器具は、胸骨の2つの半分を一緒に固定することで、創傷の剥離や感染などの合併症を予防します。これらのシステムで使用される一般的な装置には、ワイヤー、プレート、スクリュー、クリップ、骨セメントなどがあり、これらは手術後の適切な治癒を確保し、機械的な問題を防ぐために不可欠なものです。抗菌コーティングや再吸収性技術を使用したものなど、より効率的な新しい胸骨閉鎖器具の開発は、市場を前進させ続けています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025年~2034年 |

| 開始金額 | 26億米ドル |

| 予測金額 | 44億米ドル |

| CAGR | 5.3% |

2024年の市場シェアは、デバイス分野が89.8%で最大でした。開心術、特に冠動脈バイパス移植術や心臓弁置換術の増加により、胸骨閉鎖装置の需要が引き続き高まっています。心血管系疾患が依然として世界の主要死因であることから、術後に胸骨を固定するための信頼性が高く効率的なシステムの必要性が高まっています。さらに、特にリスクの高い症例や複雑な症例に対する高度な技術や固定方法が普及しつつあり、市場の成長をさらに後押ししています。

2024年には、ステンレス鋼の胸骨閉鎖システムセグメントが最大の収益を生み出し、14億米ドルと評価されました。ステンレス鋼は、その費用対効果と耐久性から支持されており、厳しい予算制約の下で運営されている病院にとって理想的です。機械的完全性を維持しながら滅菌に耐えるその能力は、特に公立病院や低・中所得地域における大量手術環境において極めて重要です。手頃な価格と信頼性の組み合わせが、ステンレス鋼を人気の高い選択肢にしています。

米国の胸骨閉鎖システム市場規模は2024年に11億米ドルとなり、2034年までには17億米ドルに達すると予測されています。米国では高齢化が進んでおり、心臓疾患の罹患率が高いことが成長の主な要因となっています。さらに、創傷感染などの合併症を減らし、回復の成果を向上させるために、ヘルスケア機関が先進的な胸骨閉鎖システムを採用するケースが増えています。これらのシステムは、病院がCenters for Medicare &Medicaid Servicesなどの組織の費用対効果や質の高い医療基準を満たすのに役立っています。

胸骨閉鎖システムの世界市場における主要企業には、Jeil Medical、Zimmer Biomet、Acumed、Stryker、KLS Martin、Orthofix、Johnson &Johnson、Praesidiaなどがあります。胸骨閉鎖システム市場の主な戦略には、抗菌コーティングや再吸収性技術などの革新的な機能を備えた製品の提供を強化するための研究開発への投資が含まれます。また、戦略的パートナーシップ、買収、提携を通じて市場での存在感を高めています。各社は、さまざまな患者のニーズに対してより多用途で効果的なソリューションを提供するため、製品ポートフォリオをますます拡大しています。さらに、特に新興市場における販売網や流通網を強化することで、これらの企業は足場を固め、より幅広い顧客層にリーチすることができます。製品の機能と性能を継続的に改善することで、これらの企業は競争市場において長期的な成長を確実なものにしています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム分析

- 業界への影響要因

- 成長促進要因

- 胸骨切開術における技術的進歩

- 心臓胸部外科手術の増加

- 主要市場における医療費償還の利用可能性の拡大

- 低侵襲手術とより迅速な回復ソリューションへの関心の高まり

- 業界の潜在的リスク・課題

- 胸骨閉鎖に伴う合併症

- 高度な閉鎖システムの高コスト

- 成長促進要因

- 成長可能性分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項トランプ政権の関税

- 貿易への影響

- テクノロジーの情勢

- 将来の市場動向

- 規制情勢

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 競争市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 閉鎖装置

- ワイヤー

- プレート・ネジ

- クリップ・ストラップ

- 骨セメント

第6章 市場推計・予測:材料別、2021年~2034年

- 主要動向

- ステンレス鋼

- チタン

- ポリエーテルエーテルケトン(PEEK)

第7章 市場推計・予測:手順別、2021年~2034年

- 主要動向

- 正中胸骨切開術

- 半側骨切り術

- 両胸開胸術

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Able Medical

- Abyrx

- Acumed

- B. Braun

- IDEAR

- Jace Medical

- Jeil Medical

- Johnson &Johnson

- Kinamed

- KLS Martin

- Orthofix

- Praesidia

- Stryker

- Waston Medical

- Zimmer Biomet

The Global Sternal Closure Systems Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 4.4 billion by 2034, driven by the increasing prevalence of cardiovascular diseases, such as coronary artery disease, which has made open-heart surgeries, especially median sternotomies, more common. As the number of cardiac surgeries rises, the demand for effective sternal closure devices has surged. Advanced sternal closure systems have enhanced patient outcomes by reducing infection risks, improving healing, and minimizing hospital stay times. The success of these systems has led to lower post-surgical complications, boosting their use and the overall market growth.

Sternal closure systems are medical devices designed to stabilize and close the sternum after surgeries like heart surgery. These devices prevent complications such as wound dehiscence and infection by holding the two halves of the sternum together. Common devices used in these systems include wires, plates, screws, clips, and bone cement, which are essential for ensuring proper healing and preventing mechanical issues after surgery. The development of new, more efficient sternal closure devices, such as those using antimicrobial coatings or resorbable technology, continues to push the market forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $4.4 Billion |

| CAGR | 5.3% |

The devices segment held the largest market share of 89.8% in 2024. The increasing number of open-heart surgeries, particularly coronary artery bypass grafting and heart valve replacement, continues to drive the demand for sternal closure devices. As cardiovascular diseases remain a leading cause of death worldwide, the need for reliable and efficient systems to fixate the sternum post-surgery is growing. Furthermore, advanced techniques and fixation methods, especially for high-risk or complicated cases, are becoming more prevalent, further propelling market growth.

In 2024, the stainless steel sternal closure systems segment generated the largest revenue, valued at USD 1.4 billion. Stainless steel is favored due to its cost-effectiveness and durability, making it ideal for hospitals operating under tight budget constraints. Its ability to withstand sterilization while maintaining mechanical integrity is crucial in high-volume surgical environments, particularly in public hospitals and low-to-middle-income regions. This combination of affordability and reliability makes stainless steel a popular choice.

U.S. Sternal Closure Systems Market was valued at USD 1.1 billion in 2024 and is anticipated to reach USD 1.7 billion by 2034. The aging population and the high incidence of heart conditions in the U.S. are the main drivers behind this growth. Furthermore, healthcare institutions are increasingly adopting advanced sternal closure systems to reduce complications like wound infections and improve recovery outcomes. These systems help hospitals meet the cost-effectiveness and quality care standards of organizations like the Centers for Medicare & Medicaid Services.

Some key players in the Global Sternal Closure Systems Market include Jeil Medical, Zimmer Biomet, Acumed, Stryker, KLS Martin, Orthofix, Johnson & Johnson, and Praesidia. Key strategies in the sternal closure systems market include investing in research and development to enhance product offerings with innovative features, such as antimicrobial coatings and resorbable technologies. They also strengthen their market presence through strategic partnerships, acquisitions, and collaborations. Companies are increasingly expanding their product portfolios to offer more versatile and effective solutions for various patient needs. Additionally, enhancing their sales and distribution networks, particularly in emerging markets, helps these companies strengthen their foothold and reach a broader customer base. By continuously improving the functionality and performance of their products, these players ensure long-term growth in the competitive market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advancements in sternotomy techniques

- 3.2.1.2 Increasing number of cardiothoracic surgical procedures

- 3.2.1.3 Growing availability of medical reimbursement across major markets

- 3.2.1.4 Rising preference for minimally invasive procedures and faster recovery solutions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complications associated with sternal closure

- 3.2.2.2 High cost of advanced closure systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerationsTrump administration tariffs

- 3.4.1 Impact on trade

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.8 Patent analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Closure devices

- 5.2.1 Wires

- 5.2.2 Plates and screws

- 5.2.3 Clips and straps

- 5.3 Bone cement

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Stainless steel

- 6.3 Titanium

- 6.4 Polyether ether ketone (PEEK)

Chapter 7 Market Estimates and Forecast, By Procedure, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Median sternotomy

- 7.3 Hemistemotomy

- 7.4 Bilateral thoracotomy

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Specialty clinics

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 Japan

- 9.4.2 China

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Mexico

- 9.5.2 Brazil

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Able Medical

- 10.2 Abyrx

- 10.3 Acumed

- 10.4 B. Braun

- 10.5 IDEAR

- 10.6 Jace Medical

- 10.7 Jeil Medical

- 10.8 Johnson & Johnson

- 10.9 Kinamed

- 10.10 KLS Martin

- 10.11 Orthofix

- 10.12 Praesidia

- 10.13 Stryker

- 10.14 Waston Medical

- 10.15 Zimmer Biomet