|

市場調査レポート

商品コード

1750412

予測遺伝子検査と消費者ゲノムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測Predictive Genetic Testing and Consumer Genomics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 予測遺伝子検査と消費者ゲノムの市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年05月07日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

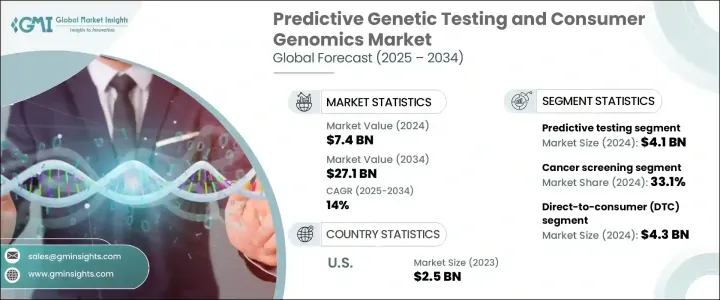

世界の予測遺伝子検査と消費者ゲノム市場は、2024年には74億米ドルと評価され、個別化ヘルスケアに対する消費者の関心の高まり、遺伝子検査技術の進歩、予防的な健康戦略へのシフトが要因となって、CAGR 14%で成長し、2034年には271億米ドルに達すると推定されています。

消費者直接(DTC)遺伝子検査は遺伝子情報へのアクセスを民主化し、個人が医療従事者の関与なしに自分の家系、ライフスタイルの特徴、潜在的な健康リスクを調べることを可能にしました。

特に次世代シークエンシング(NGS)とAIを活用したゲノム解釈における技術的飛躍的進歩は、検査の精度を劇的に向上させ、コストを下げ、消費者のアクセスを広げました。こうした進歩は、遺伝子検査会社とヘルスケアプロバイダーとのパートナーシップによってさらに補完され、ゲノムデータの臨床ケアへの統合を促進しています。慢性疾患の有病率が上昇し、ヘルスケアが予測医療や精密医療をますます採用するようになる中、北米はこの進化する情勢における世界的リーダーであり続ける立場にあります。消費者直販型(DTC)遺伝子検査の利用拡大が市場の勢いに大きな影響を与えており、健康リスクに関する洞察、先祖の内訳、ライフスタイルに関連する遺伝形質への即時アクセスを個人に提供しています。テクノロジーに精通し、健康志向の高い人々の需要が急増する中、こうしたサービスは主流になりつつあります。加えて、NIHのような機関によるイニシアチブと研究資金を通じた政府の強力なバックアップが、ゲノムツールの開発と応用のための強固な基盤を作り上げています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 74億米ドル |

| 予測金額 | 271億米ドル |

| CAGR | 14% |

2024年の市場規模は41億米ドルで、予測検査分野が市場をリードしました。これらの検査は、遺伝的体質に基づいて個人が特定の疾患や病態を開発する可能性を評価し、早期介入と個別化ヘルスケア戦略を可能にします。がんスクリーニングアプリケーションは大きな市場シェアを占め、遺伝子解析を利用してさまざまながんに関連する変異を検出し、早期診断と的を絞った予防対策を促進します。

DTC分野は2024年に世界の予測遺伝子検査と消費者ゲノム市場をリードして43億米ドルを稼ぎ出し、2034年には145億米ドルに達すると予測されています。パーソナライズされた健康とウェルネスソリューションに対する需要の高まりが、DTC検査サービスの採用に拍車をかけています。これらの検査は、個人が自宅にいながらにして、自分の先祖、ライフスタイルの特徴、潜在的な健康リスクを調べることができるようにするものです。ユーザーフレンドリーなプラットフォームと費用対効果の高いキットを提供するDTC企業は、先進国市場と新興国市場の両方で、消費者の主流への参入を推進しています。

北米の予測遺伝子検査と消費者ゲノムの市場(2024年)シェアは、高度なヘルスケアインフラ、遺伝子技術の早期導入、個別化医療と予防医療への強い文化的シフトが牽引して42%に達しました。同地域の消費者は、認知度の向上、教育水準の向上、デジタルヘルスへの取り組みに後押しされ、日常的な健康とウェルネスプラクティスの一環としてゲノム検査をますます受け入れるようになっています。

世界の予測遺伝子検査と消費者ゲノム業界の主要企業には、Abbott Laboratories、Agilent Technologies、ARUP Laboratories、BGI Genomics、Bio-Rad Laboratories、Danaher、EasyDNA、F. Hoffmann-La Roche、Illumina、Myriad Genetics、QIAGEN、Quest Diagnostics、Thermo Fisher Scientific、Variantyxなどがあります。予測遺伝子検査と消費者ゲノム市場の企業は、市場での存在感を高めるために様々な戦略を採用しています。これには、検査精度の向上とサービス提供の拡大のための研究開発への投資、遺伝子検査を臨床診療に組み込むためのヘルスケアプロバイダーとの戦略的パートナーシップの形成、アクセシビリティを高めるための消費者への直接サービスの拡大などが含まれます。さらに、企業は消費者の信頼を獲得し、検査の信頼性を確保するために、規制遵守に注力しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 個別化医療への意識の高まり

- 遺伝子配列解析における技術的進歩

- 祖先と健康に対する消費者の関心の高まり

- 業界の潜在的リスク&課題

- 遺伝子データに関する倫理とプライバシーの懸念

- テスト技術の高コスト

- 促進要因

- 成長可能性分析

- 規制情勢

- トランプ政権による関税への影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 需要側の影響(販売価格)

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:テストタイプ別、2021-2034

- 主要動向

- 予測テスト

- 遺伝的感受性検査

- 予測診断

- 人口スクリーニング

- 消費者ゲノミクス

- ウェルネスゲノミクス

- ヌートリアの遺伝学

- 皮膚と代謝の遺伝学

- その他のウェルネスゲノミクス

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- がん検診

- 心血管スクリーニング

- 筋骨格スクリーニング

- 糖尿病のスクリーニングとモニタリング

- パーキンソン病/アルツハイマー病のスクリーニング

- その他の用途

第7章 市場推計・予測:設定別、2021-2034

- 主要動向

- 消費者直販(DTC)

- 病院と診療所

- 診断検査室

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- Agilent Technologies

- ARUP Laboratories

- BGI Genomics

- Bio-Rad Laboratories

- Danaher

- EasyDNA

- F. Hoffmann-La Roche

- Illumina

- Myriad Genetics

- QIAGEN

- Quest Diagnostics

- Thermo Fisher Scientific

- Variantyx

The Global Predictive Genetic Testing and Consumer Genomics Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 14% to reach USD 27.1 billion by 2034, attributed to heightened consumer interest in personalized healthcare, advancements in genetic testing technologies, and a shift towards proactive, preventative health strategies. Direct-to-consumer (DTC) genetic testing has democratized access to genetic information, allowing individuals to explore their ancestry, lifestyle traits, and potential health risks without healthcare provider involvement.

Technological breakthroughs, particularly in next-generation sequencing (NGS) and AI-powered genomic interpretation, have dramatically improved test precision and lowered costs, broadening consumer access. These advancements are further complemented by partnerships between genetic testing firms and healthcare providers, facilitating the integration of genomic data into clinical care. As the prevalence of chronic illnesses rises, and healthcare increasingly adopts predictive and precision medicine, North America is positioned to remain the global leader in this evolving landscape. The expanding use of direct-to-consumer (DTC) genetic tests has significantly influenced market momentum, offering individuals immediate access to health risk insights, ancestry breakdowns, and lifestyle-related genetic traits. With a surge in demand from a tech-savvy and health-conscious population, these offerings are becoming more mainstream. Additionally, strong governmental backing through initiatives and research funding from institutions like the NIH has created a robust foundation for the development and application of genomic tools.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $27.1 Billion |

| CAGR | 14% |

The predictive testing segment led the market in 2024, valued at USD 4.1 billion. These tests assess the likelihood of individuals developing specific diseases or conditions based on their genetic makeup, enabling early intervention and personalized healthcare strategies. The cancer screening application accounted for a significant market share, utilizing genetic analysis to detect mutations associated with various cancers, facilitating early diagnosis and targeted prevention measures.

The DTC segment led the global predictive genetic testing and consumer genomics market in 2024, generating USD 4.3 billion and is projected to reach USD 14.5 billion by 2034, driven by offering consumers convenient access to genetic insights without the involvement of healthcare professionals. The growing demand for personalized health and wellness solutions is fueling the adoption of DTC testing services. These tests empower individuals to explore their ancestry, lifestyle traits, and potential health risks from the comfort of their homes. With user-friendly platforms and cost-effective kits, DTC companies are driving mainstream consumer engagement across both developed and emerging markets.

North America Predictive Genetic Testing and Consumer Genomics Market held 42% share in 2024 driven by a sophisticated healthcare infrastructure, early adoption of genetic technologies, and a strong cultural shift toward personalized and preventative medicine. Consumers in the region are increasingly embracing genomic testing as part of routine health and wellness practices, spurred by growing awareness, higher education levels, and digital health engagement.

Key players in the Global Predictive Genetic Testing and Consumer Genomics Industry include Abbott Laboratories, Agilent Technologies, ARUP Laboratories, BGI Genomics, Bio-Rad Laboratories, Danaher, EasyDNA, F. Hoffmann-La Roche, Illumina, Myriad Genetics, QIAGEN, Quest Diagnostics, Thermo Fisher Scientific, and Variantyx. Companies in the predictive genetic testing and consumer genomics market employ various strategies to strengthen their market presence. These include investing in research and development to enhance test accuracy and expand service offerings, forming strategic partnerships with healthcare providers to integrate genetic testing into clinical practices, and expanding direct-to-consumer services to increase accessibility. Additionally, companies are focusing on regulatory compliance to gain consumer trust and ensure the reliability of their tests.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising awareness about personalized medicine

- 3.2.1.2 Technological advancements in genetic sequencing

- 3.2.1.3 Growing consumer interest in ancestry and wellness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Ethical and privacy concerns about genetic data

- 3.2.2.2 High cost of testing technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Demand-side impact (selling price)

- 3.5.1.1 Price transmission to end markets

- 3.5.2 Key companies impacted

- 3.5.3 Strategic industry responses

- 3.5.3.1 Supply chain reconfiguration

- 3.5.3.2 Pricing and product strategies

- 3.5.3.3 Policy engagement

- 3.5.4 Outlook and future considerations

- 3.5.1 Demand-side impact (selling price)

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Test Type, 2021-2034 ($ Mn)

- 5.1 Key trends

- 5.2 Predictive testing

- 5.2.1 Genetic susceptibility test

- 5.2.2 Predictive diagnostics

- 5.2.3 Population screening

- 5.3 Consumer genomics

- 5.4 Wellness genomics

- 5.4.1 Nutria genetics

- 5.4.2 Skin and metabolism genetics

- 5.4.3 Other wellness genomics

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cancer screening

- 6.3 Cardiovascular screening

- 6.4 Musculoskeletal screening

- 6.5 Diabetic screening and monitoring

- 6.6 Parkinsons/Alzheimer disease screening

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By Setting, 2021-2034 ($ Mn)

- 7.1 Key trends

- 7.2 Direct-to-consumer (DTC)

- 7.3 Hospitals and clinics

- 7.4 Diagnostic laboratories

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Agilent Technologies

- 9.3 ARUP Laboratories

- 9.4 BGI Genomics

- 9.5 Bio-Rad Laboratories

- 9.6 Danaher

- 9.7 EasyDNA

- 9.8 F. Hoffmann-La Roche

- 9.9 Illumina

- 9.10 Myriad Genetics

- 9.11 QIAGEN

- 9.12 Quest Diagnostics

- 9.13 Thermo Fisher Scientific

- 9.14 Variantyx